What's Trending | POV | May 4, 2018

Are Plummeting Savings and Rising Debt Red Flags for Household Finances?

●●●●

● Point Of View

By many measures, the American economy is on a roll. Even with the current stock market correction, investors have seen tremendous returns in the years since the Great Recession; unemployment is at a 17-year low; and consumer confidence is at a 17-year high. Despite these bullish figures, consumer debt has also risen to historic levels, while savings have withered. A decade after the Great Recession, millions of households remain financially vulnerable due to factors like precarious employment, lack of savings, and the rapidly rising costs of housing, education, and healthcare. An economic downturn could prove catastrophic for these families.

Plummeting Consumer Savings are Cause for Concern

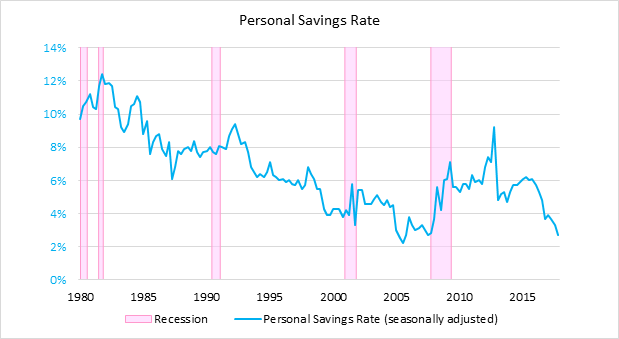

In December 2017, the personal savings rate dropped to 2.4%, the third-lowest rate ever recorded. Notably, the lowest rates on record are from 2005, at the height of the credit boom that fueled the Great Recession. While the rate has rebounded slightly in 2018, the trend is striking. In 2011, the savings rate reached 9% as families built up rainy-day funds, but has since taken a nosedive. As the graph below shows, there has been a dramatic drop in the saving rate over the last two and a half years.

Lower savings are a function of higher consumer confidence in the economy, a relationship economists call the wealth effect. During times of economic hardship, consumers squirrel away funds, and, when people feel more positive about economic conditions such as employment, home values, and earnings they dip into their savings to fund purchases. In recent months this scenario has played out at an accelerated pace as consumption, currently accounting for 70% of economic activity, has risen at a faster rate than wages. The fears that gripped consumers in the fallout of the recession seem to have all but vanished, and they are now spending the money they had been keeping locked away. This seems to be driving the current trend, even though most households have less than $1,000 in their savings accounts. When viewed alongside the growth in consumer debt, this trend seems more risky.

Rising Consumer Debt Also Raises Red Flags*

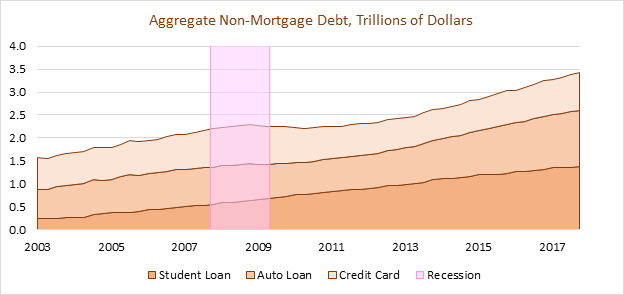

While falling savings rates are on their own cause for concern, the drop has been accompanied by a steady increase in consumer debt, which reached a historic high of $13.2 trillion in the fourth quarter of 2017. While mortgages make up two-thirds of consumer debt, total outstanding mortgage debt remains just below pre-Recession levels. Aggregate auto, student loan, and credit card debts, by contrast, have collectively increased by 51 percent over that time and now top $3 trillion, as the graph below illustrates.

These three largest categories of non-mortgage debt are driving the total increase in consumer debt. Student loan debt has increased by 250% in 10 years, growing from $550 billion in 2007 to $1.4 trillion in 2017. Auto loan debt ($1.22 trillion) and credit card debt ($0.83 trillion) both dipped in the wake of the recession, but have increased at steady paces in the last several years.

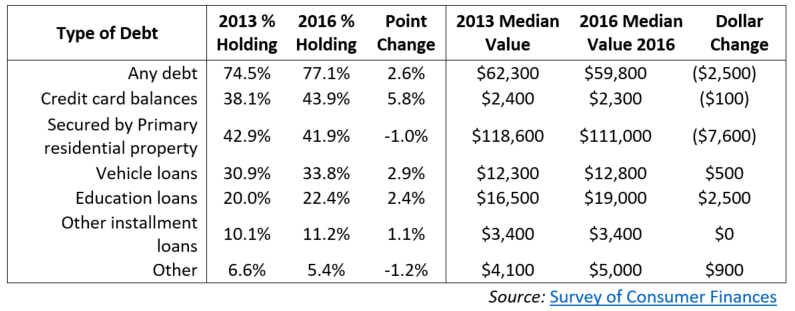

During the recovery from the Great Recession, a greater portion of Americans took on debt, and median debt levels generally rose. While fewer Americans held mortgage debt in 2016 compared to 2013, all other major categories of debt became more common for US households, as indicated in the table below.

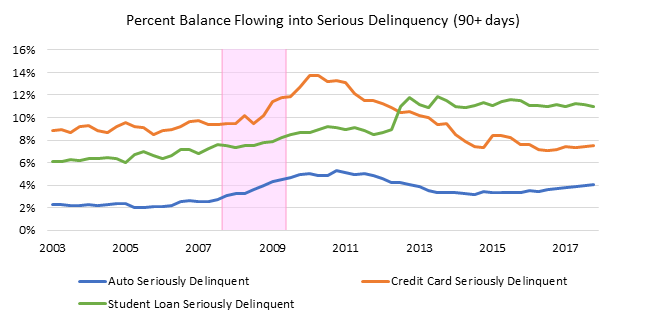

Delinquency and default rates provide warning signs about the sustainability of these record levels of debt. For example, more than 10% of student loans are seriously delinquent, and Federal Reserve officials believe that delinquency levels could actually be twice as high due to the impact of deferment, grace periods, and forbearance on the repayment cycle. Subprime auto delinquency, meanwhile, has doubled since 2011. This is “where the pressure is” according to Fed officials, who believe that increases in prime auto loans are “masking the sharp rise in subprime delinquency.”

Considered Together, Consumer Debt and Savings Trends are Striking

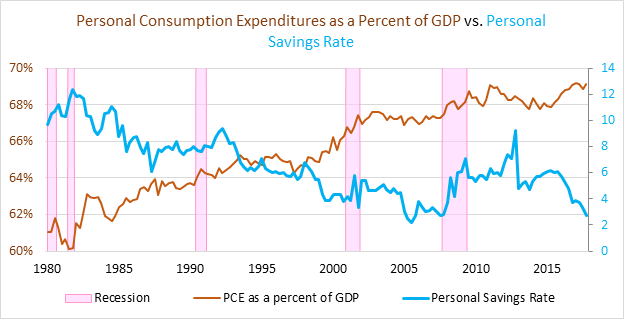

When savings and consumption are compared against each other, as in the graph below, a few trends are immediately apparent. In the below chart, the left axis shows that individuals’ consumption has become an increasingly large component of the economy, while the right axis demonstrates the sharp decline of savings in recent years. The trend in the last couple of years is visually striking, as savings have reached pre-recession levels, while consumption continues to creep ever higher. It is likely that this large gap is largely sustained by consumer borrowing and debt.

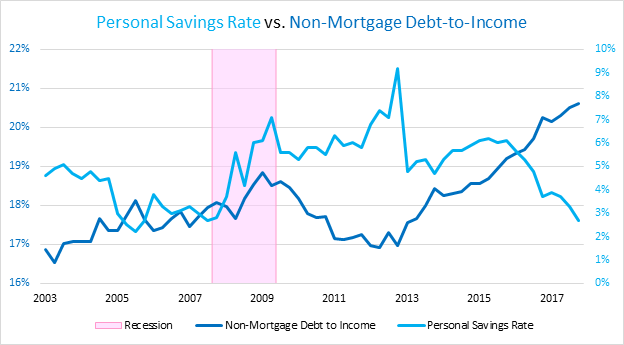

Comparing savings and non-mortgage debt, as in the graph below (in which the DTI ratio includes credit card, auto, and student loan debt), reveals another dramatic illustration of recent trends. It is generally true that non-mortgage debts fall as savings rise, and vice versa. But a wide gap has emerged quite rapidly since 2015. The dovetailing of these two measures shows that it’s essential to consider both sides of the balance sheet to understand how non-mortgage debt may impact household financial dynamics at both macro and individual household levels.

It is too early to tell if these trends are a canary in the economic coal mine. What EPIC’s work on consumer debt does tell us, however, is that debt remains a high-stakes challenge for millions of American families.

To learn more about consumer debt and EPIC’s work on the issue, visit www.aspenepic.org. We suggest checking out our research primer on consumer debt and video of our recent livestream featuring leading experts from academia, the nonprofit sector, fintech, and media.

*Many of the approximately 100 million U.S. households carrying debt are doing well with it. They have been able to access safe and affordable credit and can afford the cost of servicing their debt. Many have been able to benefit from the liquidity provided by revolving debt or the ability to purchase wealth-building assets. But it is also true that millions of indebted households are financially insecure and some populations face elevated risks. EPIC’s work on consumer debt is focused on these households with the goal of developing solutions that enhance their security.

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved