What's Trending | POV | May 22, 2019

Aspen EPIC Selects Next Consumer Financial Challenge

EPIC Insights

Housing affordability and stability have a profound impact on families’ overall financial security, and we believe now – given market conditions and policy and product opportunities – is the time to dive into this topic.

●●●●

● Point Of View

The Aspen Institute Financial Security Program (Aspen FSP) is excited to announce the next consumer financial challenge we will focus on as part of our Expanding Prosperity Impact Collaborative (EPIC): housing affordability and stability.

Housing affordability and stability affects every household in America. Whether a household owns or rents their home, housing costs represent the largest monthly expense for most. Further, having dependable shelter is one of the most basic forms of financial stability. Together, housing affordability and stability are essential aspects of families’ financial lives and well-being.

EPIC’s mission is to deeply explore a single consequential consumer financial challenge over several years, with the goal of generating widely-informed analyses and forging convergence and broad support to implement solutions that can improve the lives of millions of people. We select issues that -- based on hundreds of conversations with policymakers, families, employers, financial services providers, researchers, and others – are the biggest challenges facing Americans and which have the biggest opportunity, if solved for, to improve Americans’ financial health. The issues we select are newly informed by emerging research and practice, and present meaningful opportunities to advance solutions through public policy, private markets, or nonprofit programming and services.

To guide the selection of our 2019-2021 issue, we reviewed recent news and research on household finances, considered topics that frequently arose during our previous EPIC cycles on income volatility and consumer debt, surveyed hundreds of experts across financial security, and conducted interviews with external researchers and front-line practitioners.

Housing affordability and stability is a perfect fit for EPIC, especially at this moment in time.

Housing affordability and stability have a profound impact on families’ overall financial security, and we believe now – given market conditions and policy and product opportunities – is the time to dive into this topic. Today, households face significant and rapidly growing housing costs, while income growth has not kept up. As one expert survey respondent put it:

“Housing insecurity is coming up in nearly every conversation. It is not typically seen as a financial inclusion or access issue (except homeownership) and yet the proportion of a household balance sheet that is taken up by this expense is growing in ways that simply must be addressed.”

Harvard University’s Joint Center for Housing Studies reports that, over the past 30 years, the median rent has increased 20% more, and the median home price 41% more, than overall inflation. More than 38 million households (1 in 3) in the US are cost-burdened, paying more than 30% of their income for housing. One in 6 are severely cost-burdened, spending more than 50% of their income on housing.

There is conflicting research on the drivers of rapidly rising housing costs, with some work pointing to the role of land use policies and other studies focusing on issues like the increasing geographic concentration of job growth. Stakeholders across sectors are concerned that, since the Great Recession, construction of new houses—whether single family homes or multifamily buildings—has been historically slow, with an over-emphasis on producing luxury housing.

Meanwhile, an emerging body of work on eviction is changing public understanding of the drivers and impacts of housing instability. The Eviction Lab is aggregating data from local court systems across the United States to develop more detailed analyses of the characteristics of households at risk of eviction and the impact of threatened or actual eviction on families’ well-being and financial security. This work is likely to have important lessons for municipal policymakers and agencies concerned with fair housing.

In our preliminary research, two key themes have emerged.

First, a significant proportion of the population lacks sufficient income to afford any unsubsidized, market-rate housing in their area, leaving them vulnerable to instability and damaging their financial security in the short- and long-term. Second, the costs of constructing and operating housing are so high that not enough housing (and not the needed types of housing) is being constructed to meet demand. We will continue to explore these themes over the next several months, with the goal of clearly defining the set of specific problems that contribute to rising levels of housing unaffordability and instability [and the far-reaching impact these issues have on families, communities, and our economy].

Over the next year, we will seek answers to the following key research questions:

- How do individuals and families experience unaffordability and instability?

- What are the primary drivers of plentiful affordable and stable housing?

- What are the barriers that prevent people from accessing affordable and stable housing?

- What are the long-term impacts of housing unaffordability and housing instability on families’ financial security as well as on adults’ and children’s well-being?

- What does evidence from prior policy and program evaluations tell us about the impact of increased access to stable and affordable housing, and which strategies have been most effective?

- What other strategies might effectively contribute to solving these problems?

- Who are key stakeholders with the desire or capacity to contribute to solving these problems? How can we enable them to take action?

We will answer these questions through a variety of activities:

- We have convened an to provide strategic guidance and feedback.

- We’ve begun a multidisciplinary literature review.

- We’ve interviewed 60 experts representing broadly diverse viewpoints, and will survey and continue to consult with experts throughout the summer and fall of 2019.

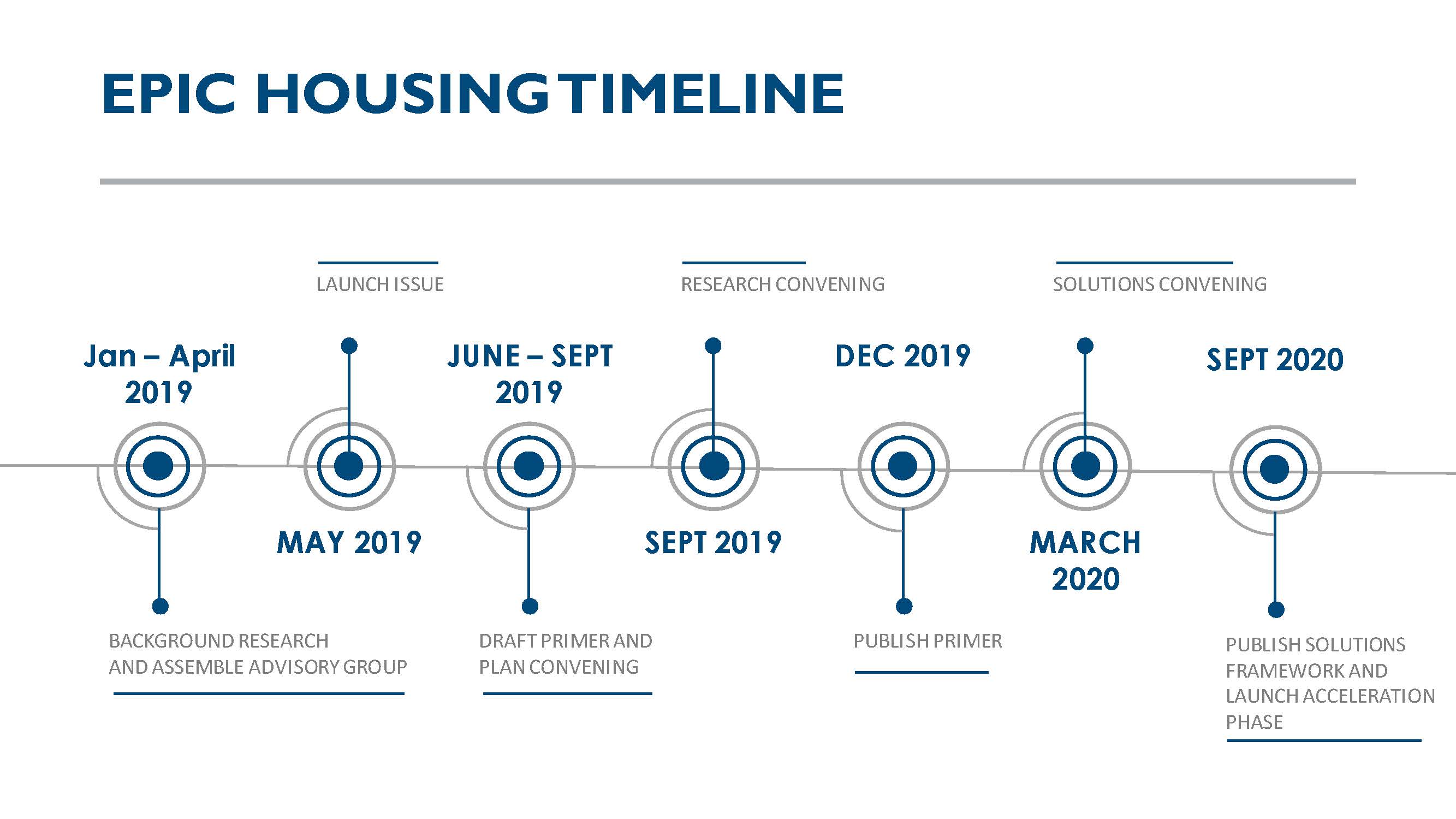

As with previous EPIC issues, we will complete our three-phase process over 2-3 years.

We are currently in the Learning and Discovery phase, which will culminate in the publication of EPIC’s Primer on Housing Affordability and Stability in December 2019. During the Solutions Development phase, we will develop and highlight strategies to solve the problems articulated in the Primer. Finally, beginning in late 2020, we will engage in the Acceleration phase, working with a set of partners to advance public and private sector solutions with the potential to affect millions of households.

Throughout the process, we’ll share occasional updates on our work (such as expert survey results), as well as relevant news and new research, on . If you’re interested in staying on top of updates from EPIC, visit www.aspenepic.org/epic-issues/housing/.

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved