The Issues | What We Know | September 2017

Issue Brief

●●●●

● Summary

Job loss is one of the top two sources of unexpected income loss for households. Unpredictable schedules—the other top cause—and job losses result in different patterns of income volatility. Scheduling-related volatility is regularly occurring and shocks have relatively smaller magnitudes. Job loss leads to large, sudden, very large dips in income that are generally followed by slow, sometimes incomplete, recoveries. Yet many efforts to understand and address income volatility do not differentiate between volatility caused by irregular work schedules and that caused by job loss.

Newly unemployed workers face not only the short-term financial distress associated with dips in income, but also a long-term reduction in earnings, leaving them with fewer resources to manage income volatility in the future. In recent decades, laid-off workers often do not reach their previous level of earnings for as long as six years. Even once reemployed, these workers face the type of ongoing, shortterm volatility that impacts nearly half of all households— though future income spikes are likely to be smaller in magnitude. To explore these specific challenges, EPIC is focusing two briefs in our series on promising solutions to income volatility caused by job loss: this brief on unemployment insurance and a previous brief on wage insurance. Both briefs focus on public policies that can make these social insurance schemes work well for families, as well as explore private sector opportunities to minimize the financial insecurity caused by job loss.

This brief reviews the current research on how income shocks associated with job displacement impact families’ financial security in the short- and long-term. It discusses the performance of current UI programs and a range of reform proposals. The brief also explores specific reforms that would enable UI programs to serve a broader base of workers and buffer more effectively against employment-related negative income shocks. It also considers the roles of key institutions – governments, employers, and financial services providers including insurers—in supporting UI reforms, and identifies specific opportunities for private-sector leadership.

● Background

The Expanding Prosperity Impact Collaborative (EPIC), an initiative of the Aspen Institute’s Financial Security Program, is a first-of-its-kind, cross-sector effort to shine a light on economic forces that severely impact the financial security of millions of Americans. EPIC deeply investigates one consequential consumer finance issue at a time.

EPIC’s first issue is income volatility, which destabilizes the budgets of nearly half of American households. Over the last year, EPIC has synthesized data, polled consumers, surveyed experts, published reports, and convened leaders, all to build a more accurate understanding of how income volatility impacts low- and moderate-income families and how best to combat the most destabilizing dimensions of the problem.

This brief on unemployment insurance is one of a series that explores highly promising solutions to income volatility. Unemployment insurance addresses one of the leading causes of income volatility: job loss. The United States’ Unemployment Insurance Program (UI), however, fails to serve the vast majority of U.S. workers because it has not adapted to changes in the economy and labor markets. This brief identifies opportunities to reform UI to expand coverage and make the program more flexible and portable, as well as opportunities for private-sector stakeholders to provide more effective support. Our hope is that this brief will support public and private leaders—including employers and financial services providers—as they seek to help workers who struggle in increasingly insecure and precarious labor markets.

● Issue Brief

JOB LOSS IS A LEADING CAUSE OF INCOME VOLATILITY BUT FEW FAMILIES ARE PREPARED TO WEATHER A SPELL OF UNEMPLOYMENT

Income volatility has become both more common and more intense in recent decades. The share of households experiencing an income loss of $20,000 per year or more, for example, rose by 23% from 1991-2004. The Pew Charitable Trusts define a “sudden income shock” as a year-over-year change of more than 25%, and find that 15% of households experience a negative shock each year. Among those who experience income volatility, the second most common reason (following irregular work schedules) is unemployment.

Different sources of volatility impact workers’ financial security in different ways. Volatility caused by irregular work schedules manifests as regularly occurring, but difficult to predict, short-term fluctuations in income. In contrast, job loss causes large, sudden dips in income that are generally followed by a slow, sometimes incomplete, recovery. Solutions to this type of income volatility must help more workers access income supports such as UI during unemployment, expand non-governmental resources available to unemployed and underemployed workers, and provide ongoing support as workers climb back up the income ladder.

Although the labor market is stronger than it has been in a decade, the risk of job loss remains real—for example, 17 million workers experienced an involuntary spell of unemployment in 2015. Most families are inadequately prepared to weather even one month without income. Nearly 70% of Americans report having less than $1,000 in a liquid savings account—likely not enough to cover even one rent or mortgage payment.

Unfortunately, the social safety net does little to protect workers from the financial risks of unemployment. Over the past forty years, the United States labor market has experienced significant shifts, driven by globalization, the decline of pensions and unions, automation, and the rise of the gig economy and other alternative work arrangements. Support for unemployed workers, however, have not kept pace with these changes. UI coverage has eroded to record lows, with less than 30% of jobless workers receiving benefits. Moreover, UI benefits are generally exhausted after 26 weeks, even though the mean duration of unemployment is almost two weeks longer than that.

These outdated policies have contributed to the rising financial burden of unemployment, particularly among lower-income households. Pew’s research indicates families that experience negative income shocks do, in fact, have lower financial wellbeing than others. These families are more likely to miss bill payments or delay medical care, and are less likely to have savings. The lowest-income families in this group report having just $100 in savings.

UNEMPLOYMENT INSURANCE COULD REDUCE UNEMPLOYMENT-RELATED INCOME VOLATILITY FOR MILLIONS BUT REQUIRES MAJOR REFORMS

Insurance is one of the most effective ways to hedge against financial risks. In the private sector, insurance is available to protect consumers against the risks of costly medical care, car accidents, theft, floods and fires, early death, and outliving one’s savings. In the public sector, social insurance programs protect certain groups of individuals, primarily workers (Unemployment Insurance, Workers Compensation), the disabled (Social Security Disability Insurance), poor families (Medicaid), and the elderly (Medicare and Social Security).

Insurance is one of the most effective ways to hedge against financial risks. In the private sector, insurance is available to protect consumers against the risks of costly medical care, car accidents, theft, floods and fires, early death, and outliving one’s savings. In the public sector, social insurance programs protect certain groups of individuals, primarily workers (Unemployment Insurance, Workers Compensation), the disabled (Social Security Disability Insurance), poor families (Medicaid), and the elderly (Medicare and Social Security).

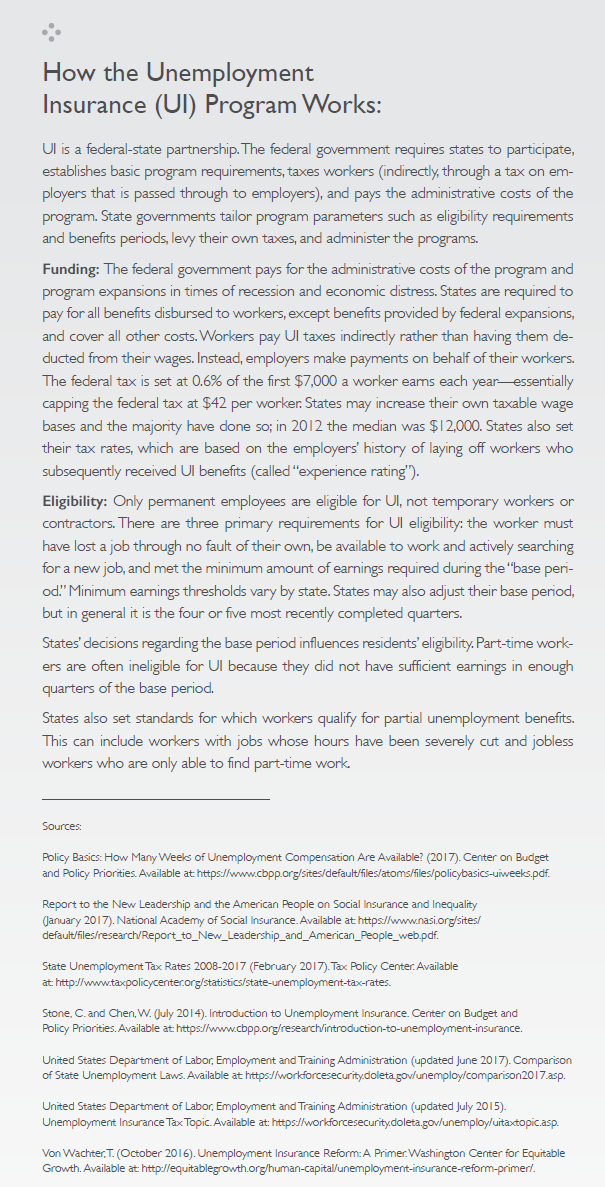

Since the New Deal, the Unemployment Insurance (UI) program, a federal-state partnership, has provided income support for

workers who have lost their jobs and are actively searching for new positions. UI is designed to replace a substantial portion of lost income while encouraging workers to find new jobs quickly. The sidebar to the left summarizes how the program is structured and implemented.

The UI program has proven highly effective at stabilizing individual households and the economy as a whole. In general, each dollar spent on UI generates more than one dollar in economic benefits, and this effect is magnified during recessions. A recent report on the state of the UI system found that during the Great Recession, UI lifted 5 million people out of poverty and prevented more than 2 million job losses. With fewer and fewer workers covered by the program, however, its current and future effectiveness is questionable.

Many of the rules and regulations that restrict eligibility may have made sense in the past, but are no longer appropriate given changes in the labor market. The proportion of workers covered by UI has fallen steadily for decades. At the same time, the length of spells of unemployment has increased, leaving a greater proportion of UI recipients unable to find new jobs before they exhaust their benefits. Specifically:

- In 1990, the proportion of workers covered by UI was 40%. Now it is just 27%.

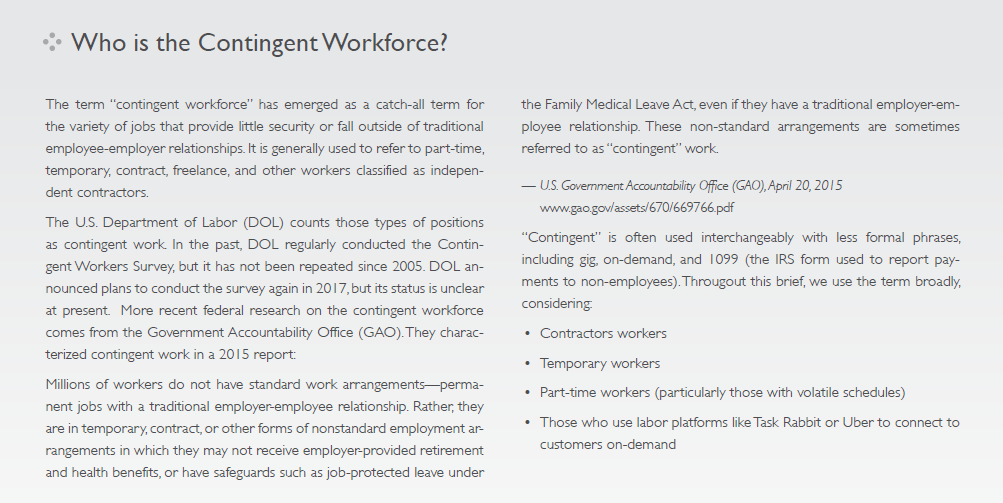

- The contingent workforce, including part-time, temporary, and independent contractors, has grown rapidly since 2000. Already, as many as 16% of U.S. workers have contingent jobs, 17 which are generally ineligible for UI.

- Throughout the 1990s, the mean duration of unemployment was 13 weeks, 18 while in 2015 it reached 28 weeks.

- Even though the unemployment rate has returned to pre-recession levels, 20 one out of every four jobless workers has been unemployed for longer than UI’s standard 26-week eligibility period.

HOW INSTITUTIONS CAN HELP:

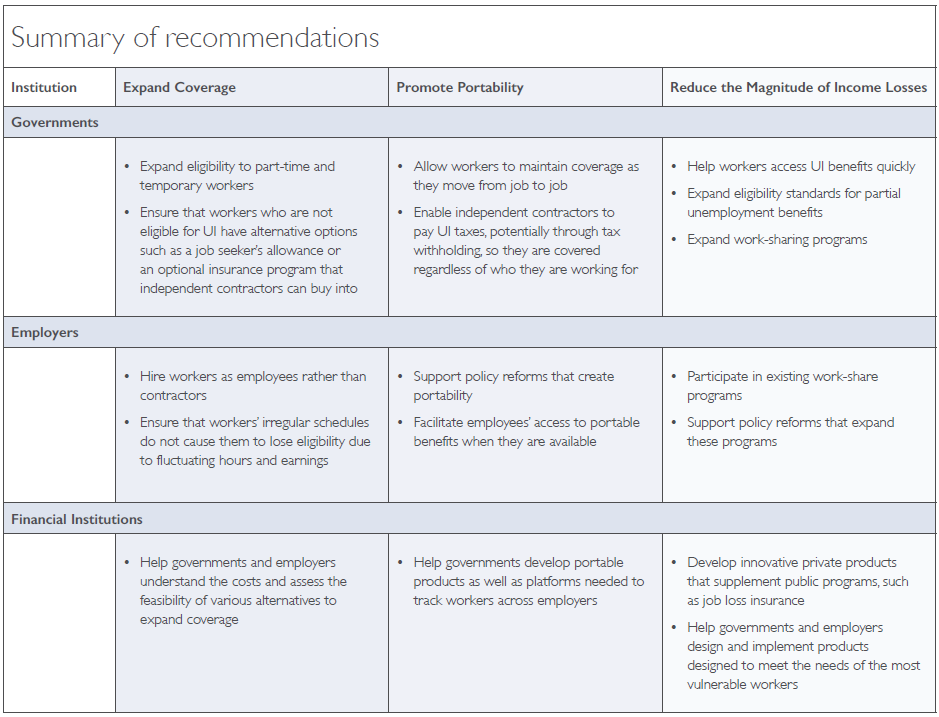

When EPIC surveyed our panel of experts about trends in income volatility, more than 70% expected it to increase in the next decade. They identified social insurance policies as among the most likely to reduce income volatility. Likewise, labor experts anticipate that employment security will continue to decline while “alternative work arrangements” will continue to grow. To better address income volatility and insure workers against negative income shocks, reform efforts should expand coverage, promote portability, and reduce the magnitude of income losses. This section of the brief identifies opportunities for government, employers, and financial institutions to contribute toward these goals. Each of these players have critical roles to play:

Government must take the lead. Employers and financial institutions cannot solve these problems without government partnership. The federal government is the only institution with the capacity to reach all of the nation’s 160 million workers. It has the ultimate authority over UI and has significant influence over how each state implements the program. The states also have considerable discretion to adapt UI to their workers’ and businesses’ needs. They also have the power to develop supplemental programs.

Employers and financial institutions should not be expected to fix workforce- wide problems like coverage erosion by themselves, but they have many opportunities to help cushion the blow. Employers can work to understand the impact of lack of coverage on workers and change hiring, compensation, and scheduling practices that exclude workers from UI. Financial institutions can be essential partners in any effort to reform UI, as they offer the products and infrastructure for delivering benefits. Their role as innovators is equally valuable as governments and employers develop new solutions.

EXPANDING COVERAGE:

Expanding the UI program’s coverage is the greatest priority. UI’s 46% income replacement rate is an admirable achievement, but a safety net that serves only one in four workers in need has too many gaps. Government policy changes, employer labor practices, and financial products and partnerships are all part of the solution to this pressing challenge. Each institution can take significant steps to increase coverage rates.

GOVERNMENT

UI coverage will most likely continue to erode if policymakers do not take action to cover contingent workers. These types of jobs were initially excluded from UI for a variety of reasons, from logistical challenges to preventing cheating to limiting the program to primary breadwinners. But these jobs no longer represent the periphery of the labor market—they account for nearly all net job creation since 2005. Not only are these groups of workers growing rapidly, they are also among the most vulnerable to negative income shocks. The Government Accountability Office found that contingent workers are more likely to experience job instability and less likely to receive benefits or workplace protections. The National Academy of Social Insurance finds that this increases contingent workers’ risk of income volatility, tax penalties, and inability to afford healthcare, among other risks.

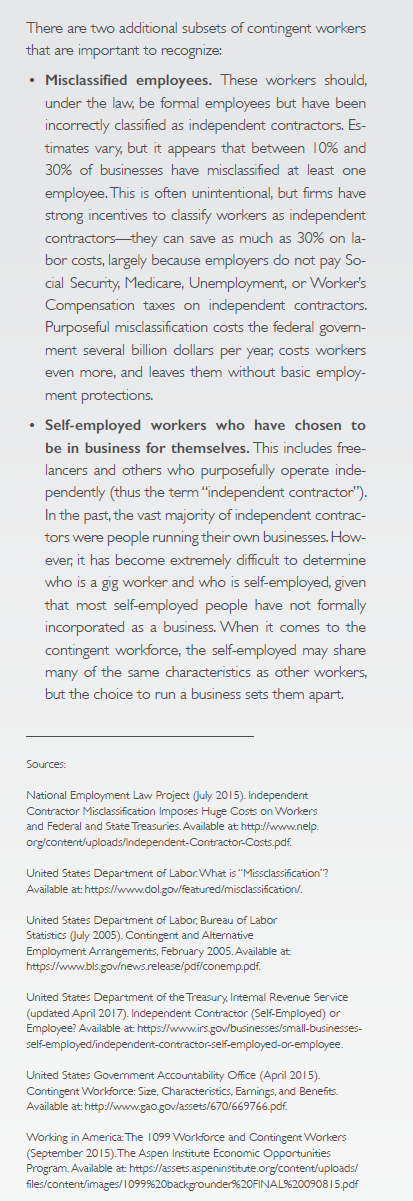

For many contingent workers, simply changing UI eligibility standards and prorating benefits would be enough to ensure their UI coverage. Expanding UI to 1099 workers, however, is much more complicated. That is because it is difficult to verify whether changes in a 1099 worker’s earnings are truly due to a lack of available work rather than lack of effort. Many self-employed business owners, for example, are paid primarily through 1099s – but business owners have much greater control over their hours and workload than the average worker.

Several proposals have identified ways to address this issue. The Center for American Progress (CAP), National Employment Law Project (NELP), and Georgetown University Center on Poverty and Inequality call for a “Job Seeker’s Allowance,” a benefit of about half the duration and half the value of UI, to be available to most job seekers who do not qualify for UI. Economist Jonathan Gruber proposes that the government should fully fund security accounts – funded with a 6% match on earnings – for all workers earning less than $25,000. Government supports could be phased out as earnings rise. Further contributions by workers and employers would be optional, and the accounts would link to government-established retirement accounts. Others suggest allowing firms to pool their independent workers to provide affordable access to private insurance—without losing the right to classify those workers as 1099s.

States also have opportunities to lead. One easy approach would be to treat the federal guidelines on eligibility, benefit amounts and periods, and funding as minimum standards and commit to meeting or improving upon them. States can also amend rules to expand coverage to more part-time workers and ensure that workers who experience high income volatility are not penalized with regard to eligibility or amount of benefits. Furthermore, states can consider strategies to increase funding for their UI programs, such as increasing the taxable wage base and increasing their UI tax rate, in order to increase the income replacement rate, lengthen benefit eligibility periods, and/or increase benefit amounts.

States are also well-positioned to develop innovative alternative policies to expand coverage to 1099 workers. California’s opt-in, short-term disability insurance and paid family leave program for the self-employed may offer a model: self-employed workers can choose to contribute to the state’s disability insurance fund to gain coverage. While disability and paid leave are different from unemployment, all involve challenging cuts in pay. States could replicate the California approach to create an optional program for 1099 workers.

EMPLOYERS

Employer compensation and scheduling practices are at the heart of income volatility, so employers have an essential role to play in any effort to reduce volatility and mitigate its impact. The single most consequential thing employers can do to expand UI coverage is, when possible, hire employees instead of contractors or temporary workers. This would increase labor costs, but could also potentially increase workers’ job satisfaction, reduce their financial stress, and improve turnover rates. Employers could also study the state-level UI rules related to the distribution of earnings and eligibility of part-time employees. With a better understanding of how these rules impact their workers, they could change their practices to maximize worker wellbeing with minimal impact on their bottom line. This could include, for example, providing part-timers with enough hours to be eligible for coverage. For workers with variable schedules, employers can more intentionally distribute their shifts to prevent disqualification for UI based on fluctuations in their hours and earnings patterns.

FINANCIAL INSTITUTIONS

Collaboration with financial institutions is critical for governments and employers to be able to offer insurance coverage to more workers and launch new products to reduce the impact of layoffs. They have the expertise, data, and back-end systems needed to address questions related to the feasibility of covering contingent workers, estimate the costs of various products and proposals, and implement new products and systems effectively.

PROMOTE PORTABILITY:

Workers no longer stay with a single employer for their whole career, but unemployment policies are still built for that relationship. Not only do today’s workers change jobs more often, many seek work across multiple platforms simultaneously. Tying benefits to a relationship with a single employer no longer makes sense. Instead, benefits should be tied to the worker, and portable from job to job. This would make benefits available to contingent workers as well as those who are laid off a short time after starting a new position.

GOVERNMENT

Within the UI system, portability could be achieved by associating unemployment taxes paid by firms with specific workers they employ, and basing individual benefits on their actual, total work rather than their work for a single employer. Making UI portable presents real policy challenges, but the National Academy of Social Insurance points out that we do not need to reinvent the wheel:

Even though most of the American social insurance system was designed well before the rise of nonstandard work, programs like Social Security and Medicare are in many ways ideally suited to the needs of the 21st century workforce. These programs are portable… Policymakers should thus consider ways to build on this successful social insurance model.

—National Academy of Social Insurance, 201728

Etsy, for example, proposes switching to tax withholding to fund unemployment benefits, rather than the current tax paid by employers on behalf of their employees. Under Etsy’s proposal, workers would pay into the system based on the information provided on the tax documents they complete in order to receive payment (W-4s for employees and W-9s for contractors). This would enable all workers to pay into the system, and thus support expanding eligibility. Currently, firms are not responsible for withholding taxes from contractors’ payments, but this would be necessary for such a plan to work.

Others, such as the CAP, NELP and Georgetown proposal discussed above, have suggested creating a portable system parallel to UI as a way to ensure the broadest possible coverage. This is similar to the California model for insuring the self-employed. The benefit of this approach is that it does not require amending the UI program itself. However, it would require a challenging level of coordination and agreement among self-organized groups of employers. A similar model exists in the retirement space in the form of multiple employer plans: participating small employers band together to collectively offer one retirement plan to their employees.

Several proposals envision portable benefits systems at the national level, but it is important to note that states can independently make many of these changes.

EMPLOYERS

The success or failure of portable benefits will depend on workers being aware of these products and employers facilitating access to them. Some firms have publicly declared interest in offering portable benefits to their workers, and others should follow suit. Etsy’s proposal would create a system in which firms could offer supplemental, portable benefit plans to workers who aren’t covered alongside regular benefits to those who are. Under Etsy’s proposal, workers would consolidate their tax-preferred retirement, education, health, and other accounts into a single, portable “MyFlex Account” to which they could make supplemental contributions. Last year, a group of industry and policy leaders—including major platform employers Lyft and Care.com as well as the Aspen Institute Economic Opportunities Program—jointly released a call for portable benefits.

In many cases, such as state short-term disability and paid leave programs, employers can already offer portable benefits. Wherever possible, employers should facilitate employees’ access to these products. In other cases, portable benefits would violate existing labor laws, but, in those situations, supportive employers can still make a powerful case for policy reforms. In fact, leading gig economy firms Lyft and Postmates have supported federal legislation introduced in May 2017 by Senator Mark Warner (D-VA) and Representative Suzan DelBene (D-WA) to study, pilot, and evaluate state-level initiatives to make benefits portable.

FINANCIAL INSTITUTIONS

Making portable benefits a reality requires support from financial institutions. Governments need their help to develop both products and platforms. Implementing proposals such as a job seekers allowance or MyFlex Accounts would be new territory for public policy but deeply familiar to many in the financial industry. Firms that provide Health Savings Accounts to employers, for example, would have valuable insight regarding increasing workers’ optional contributions. Personal financial management firms have deep experience developing platforms that consumers can use to integrate data from their various accounts, while large banks that provide children’s savings accounts know how to manage multiple small-balance accounts receiving small contributions from multiple sources.

REDUCE THE MAGNITUDE OF NEGATIVE INCOME SHOCKS:

Layoffs are an inevitable feature of the labor market, making some level of unemployment-related income volatility inevitable as well. That said, the degree of volatility matters. The larger the shock, the harder it can be for households to manage without financial hardship. There are numerous opportunities to reduce the magnitude of income shocks due to job loss. It is far easier to cope with a 30% reduction in wages than a 50% cut or total loss. UI itself directly reduces the magnitude of shocks, particularly for families—recent research indicates that receiving benefits reduces the loss of 45% of family income to a loss of just 16%. Governments can do more through proactive efforts to help employers avoid layoffs, while employers and financial institutions have opportunities to innovate.

GOVERNMENT

Governments should seek opportunities to reduce the magnitude of negative income shocks. Simple changes in the structure and priorities of the UI program could soften the blow of income loss. For example, shortening the waiting period between filing an initial claim and beginning to receive benefits would help the large majority of households that have less than one month’s expenses saved.

Expanding eligibility standards for partial unemployment benefits would help workers who are experiencing income volatility due to reduced employment by making up for some of their lost wages. This reform would also encourage more jobless workers to accept part-time jobs while they continue looking for full-time work. This would help these workers speed up the process of increasing and stabilizing their income after the initial negative shock. The Century Foundation has proposed that states allow UI-eligible workers who have part-time jobs to claim partial benefits if their weekly earnings are less than 150% of the weekly benefit they would receive if they had been fully laid off and were not working at all.

Expanding work-sharing could also make a difference. Work-sharing programs help employers avoid layoffs by cutting all workers’ hours, while the affected workers receive UI funds to make up most of the difference.36 This enables workers to maintain more of their income and prevents some layoffs among workers who are not covered by UI. CAP, NELP, and Georgetown explore these programs in depth in their report on modernizing UI, and conclude that expanding work-sharing would leave many workers better off.

Once again, this is an area where states have an opportunity to lead. In 2009, only 17 states offered UI work-sharing programs, which served just 0.2% of workers in those states. Research suggests that they were effective in preventing job losses in manufacturing—the sector most likely to participate—but that low overall take-up rates limit their impact on the economy as a whole. Potential reasons for the low-take-up rate include: several states have implemented a participation fee for employers, making it more expensive than the regular UI program; some states also require employers to continue providing full health and pension benefits to participating workers; and some employers choose not to participate because they fear their most productive workers will quit. AARP suggests that states can bolster work-sharing programs by addressing these limitations: removing unnecessary restrictions, helping firms with administrative costs, implementing promotional campaigns with employers, and collecting data on programs’ costs, benefits, and number of jobs saved.

EMPLOYERS

No employer, no matter how supportive of their workers, can totally eliminate job losses. Employers can, however, do more to ensure that laid off workers are able to weather the loss of income. One easy, high-impact option is to support and participate in UI work-sharing programs. Even though just 0.2% of employees in work-sharing states participated during the Great Recession, the program still saved an estimated 160,000 jobs. With stronger employer participation, the program has the potential not only to save significantly more jobs, but also reduce the magnitude of negative income shocks for millions of workers.

Employers can also provide access—and even subsidize access—to private products that are designed to help smooth income and those intended to support laid off workers. The simplest option is to provide some sort of severance pay to workers not covered by UI who lose jobs through no fault of their own. Employers can also work with insurance firms to develop and offer new products designed for individual workers who are not covered.

FINANCIAL INSTITUTIONS

Financial institutions are best-positioned to develop innovative new insurance products. The state-level regulatory structure presents challenges to insurance innovation, but it is not insurmountable. SafetyNet is pioneering an affordable, individual “job loss insurance” product with monthly premiums as low as $5 for a policy that pays out $1,500. Workers can customize the product to fit their needs, and it has been designed with the self-employed and 1099 workers in mind.

Finally, financial institutions have unmatched expertise when it comes to product design, and can put that expertise to use in partnership with employers, governments, and nonprofits. Working with these institutions to create new products designed around the needs of the most vulnerable workers would likely result in more appealing and effective options. Such partnerships are proving critical to government efforts to support retirement savings, such as state Secure Choice programs.

CONCLUSION

Although income volatility caused by job loss is common, many efforts to address income volatility do not consider the specific challenges and needs of laid off workers. Job loss causes large, sudden dips in income that are generally followed by a slow, sometimes incomplete, recovery. Newly unemployed workers face not only the short-term financial distress associated with dips in income, but also a long-term reduction in earnings, leaving them with fewer resources to manage income volatility in the future. Those challenges require different solutions than volatility caused by irregular work schedules.

Unemployment insurance is an effective strategy to reduce and mitigate the consequences of income volatility because it prevents a total disruption in income and significantly reduces the magnitude of wage losses. Unfortunately, the United States’ current UI system fails to serve the majority of U.S. workers because it has not adapted to changes in the economy and labor markets. For the most part, those who are not covered by UI have no other sources of income support.

Major reforms and innovations are necessary to restore the program’s ability to adequately protect laid off workers against income volatility. Reforms should focus on expanding eligibility for contingent workers, enabling portable benefits that follow workers from job to job, and reducing the severity of income losses. We see opportunities not only for the federal and state governments to strengthen their safety nets, but also for private-sector stakeholders to innovate and provide more effective support.

For Endnotes and Works Cited, please download the PDF version of this Issue Brief:

● Acknowledgments

EPIC would like to thank Katherine Lucas McKay for writing this brief; Kiese Hansen, Gracie Lynne, David Mitchell, Ida Rademacher, and Joanna Smith-Ramani for reviewing drafts and making invaluable suggestions; Liz Ben-Ishai, Mark Greene, Adele Hunter, Tim Lucas, and Rachel West for the time and wisdom they shared on a topics ranging from labor markets conditions, unemployment and jobless workers, social insurance, and private market products; thanks also to Laura Starita at Sona Partners for designing the template. EPIC would also like to thank all those who completed the expert surveys or participated in either of the EPIC convenings. While this document draws on insights shared at these EPIC forums and by the aforementioned individuals, the findings, interpretations, and conclusions expressed in this report – as well as any errors – are EPIC’s alone and do not necessarily represent the view of EPIC’s funders or Advisory Group members. Finally, EPIC thanks the Ford Foundation and the W.K. Kellogg Foundation for their generous support.

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved