The Issues | What We Know | May 2017

●●●●

● Summary

EPIC has identified when and how workers get paid as an untapped opportunity for building financial resiliency and security in the face of growing volatility. This brief explores the ways in which payroll innovation and technology can help workers better manage volatility, including:

- giving workers quicker access to funds they have already earned;

- rescheduling paydays to better align with lumpy expenses like rent;

- customizing paychecks so that bills, debt payments, and other ex- penses are deducted automatically; and

- linking paychecks to a worker’s other financial accounts so that payroll deductions for savings or other uses can be automatically dialed up or down based on the worker’s current cashflow position.

● Background

The Expanding Prosperity Impact Collaborative (EPIC), an initiative of the Aspen Institute’s Financial Security Program, is a first-of-its-kind, cross-sector effort to shine a light on economic forces that severely impact the financial security of millions of Americans. EPIC deeply investigates one consequential consumer finance issue at a time.

EPIC’s first issue is income volatility, which destabilizes the budgets of nearly half of American house- holds. Over the last year, EPIC has synthesized data, polled consumers, surveyed experts, published re- ports, and convened leaders, all to build a more ac- curate understanding of how income volatility affects low- and moderate-income families and how best to combat the most destabilizing dimensions of the problem.

This brief on payroll innovation is part of a series that explores highly promising solutions to income volatility. Our hope is that this brief will push financial service providers, employers, and governments to consider ways to update and improve how workers get paid, and in the process, give households a new tool for achieving financial stability.

● Issue Brief

THE LINK BETWEEN PAYCHECKS & INCOME AND EXPENSE VOLATILITY

In one sense, periodic paychecks are, by definition, drivers of income volatility. Every payday is an income spike. And, indeed, when focused on intra-year or month-to-month volatility, it turns out that when and how one gets paid is a major driver of the short-term swings we see in the data. For example, a once-a-year bonus paid in lump sum increases intra-year volatility.

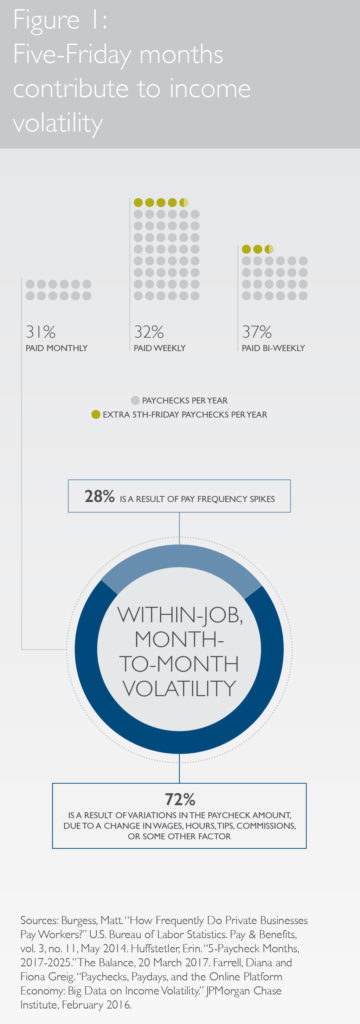

A slightly more superficial example is the case of five-Friday months. If  you’re among the 32% of private sector workers who are paid every week, then any month that includes five Fridays – of which there are four to five every year – will include an extra paycheck.The 37% of private sector workers who are paid every other week will also see an extra paycheck in two or three months every year. According to the JP- Morgan Chase Institute, 28% of within-job month-to-month volatility is a result of these pay frequency spikes, whereas the remaining 72% of with- in-job volatility is explained by variation in the paycheck amount, due to a change in wages, hours, tips, commissions, or some other factor.

you’re among the 32% of private sector workers who are paid every week, then any month that includes five Fridays – of which there are four to five every year – will include an extra paycheck.The 37% of private sector workers who are paid every other week will also see an extra paycheck in two or three months every year. According to the JP- Morgan Chase Institute, 28% of within-job month-to-month volatility is a result of these pay frequency spikes, whereas the remaining 72% of with- in-job volatility is explained by variation in the paycheck amount, due to a change in wages, hours, tips, commissions, or some other factor.

Of course, what matters more to families than when or how often they get paid, is the extent to which they have access to their pay when they need the money. If a bill comes due days, or even hours, before a pay- check lands in a worker’s checking account, the result can be financially disastrous – leading to late fees, overdraft charges, payday loans, pawn shops, or other costly financial bridges. This problem is accentuated when the financial obligations coming due are irregular and unpredictable, which, according to other research from the JPMorgan Chase Institute, is a widespread challenge.The median family in JPMorgan Chase Institute’s analysis, for example, saw a 29% change in total expenses from one month to the next, and almost four in ten families had to make a sizeable medical, tax, or auto repair payment at some point over the course of the year.

INNOVATION #1: QUICKER & MORE FREQUENT PAY

One tempting way to react to the negative outcomes that come from a mistimed paycheck is to simply push for quicker and more frequent pay. After all, the thinking goes, why should workers have to resort to risky credit products while the money they’ve already earned – possibly enough to cover the current bill or emergency – is being held by their employer? Furthermore, given their size and financial sophistication, employers are almost always better positioned than individuals or families to manage cash-flow challenges and navigate the short-term credit markets.

The question of how frequently to pay employees is timeless.The Bible itself offers a passage in favor of daily pay, urging adherents in Deuteronomy 24:15 to “pay [your hired servants] their wages each day before sunset because they are poor and are counting on it.”

Interestingly though, workers themselves seem split on the idea. According to one industry survey, 53% of millennials somewhat or completely agree with the statement,“having access to my pay as I earn it would not be a useful tool for me.” Additionally, a CFED survey of young workers found an equal number of interviewees opposed to an employer-provided payroll advance as there were supportive. Those opposed cited their aversion to feeling indebted to their employer – perhaps a signal that consumers do not fully appreciate that these products are technically not loans – and their fear that they would spend the money on things they didn’t need.

More than one in four millennials prefer real-time pay to a raise. And 97% of one pay advance company’s customers report having lower stress, due in part to reduced overdraft and interest fees.

And, in fact, there is evidence that individuals often prefer the forced saving inherent in large, delayed lump-sum payments to smaller, more regular payments – whether they be tax refunds or wages. This preference for the lump sum may be based on individuals’ desire for commitment devices to thwart short-term temptation. And there is evidence, at least from the developing world, that infrequent lump-sum payments lead to lower levels of stress and more long-term savings and investment, like the purchase of durable goods. This may be because of mental accounting: money that comes infrequently – particularly once a year – feels less like current income and more like an increase in wealth, which, the thinking goes, should be saved instead of spent. (Of course, not all lump sums are characterized as wealth; windfalls like gambling or lottery winnings, for example, often feel like expendable income and are spent as such.)

In keeping with the short-term temptation (called by economists “present bias” or “hyperbolic discounting”) and mental ac- counting hypotheses, many studies have found that consumption tends to spike immediately after the receipt of income, even when that income is expected and regular, like a paycheck, and even among households who are not liquidity-constrained. These spikes in consumption around income receipt have quite literally made paydays in the U.S. a matter of life and death: mortality is more common on, and in the days right after, a payday.This is likely because the new disposable income is used to embark on activities outside the home, some of which can be risky in and of themselves, like playing sports and drinking alcohol, and some of which merely require risky forms of transportation, like driving to the mall.

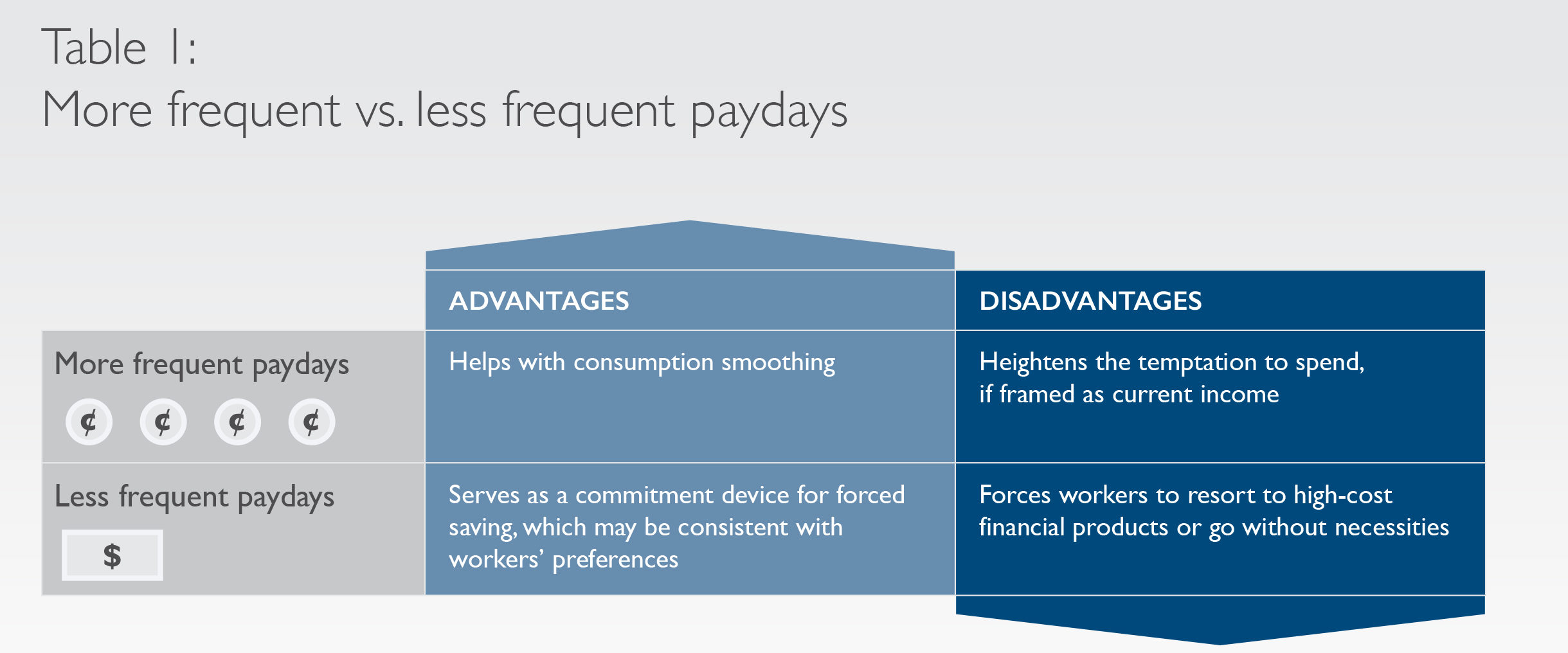

At first blush, these findings may argue for fewer, not more frequent, paydays. But the evidence cuts both ways. More frequent paydays would mean smaller checks and, perhaps, smaller spending spikes. One recent study, for example, found that retired couples who happen to receive both of their monthly Social Security checks on the same day struggle to smooth their consumption and spend more during that week than do couples who have two “paydays” (i.e., receive their checks at two different points in the month). This effect was particularly strong for low-income households. Studies from the developing world have found similar consumption-smoothing benefits, observing that more frequent, rather than lump-sum, pay made it less likely for the recipient to skip meals or otherwise face food insecurity, less likely to receive charity, and more likely to visit the doctor. Additionally, more than one in four millennials prefer real-time pay to a raise, according to the same industry survey referenced above. And a separate survey found that 97% of one pay advance company’s customers report having lower stress, due in part to reduced overdraft and interest fees.

There are, then, advantages and disadvantages to each approach (see Table 1). Much seems to depend on how the new pay is viewed by workers (e.g., as loans from their employer that must be paid back; as an unexpected bonus to be spent; as an expected rebate to be saved; or simply as present income to be treated like any other paycheck). Rising income volatility only complicates the picture, as paycheck amounts become less uniform and their delivery less regular. Despite this uncertainty, several employers and financial firms are speeding ahead with innovations that make pay available more frequently, and government is considering its options as well, as described below.

GOVERNMENTS

One way to accelerate how regularly workers are paid is for the government to simply require it. Little-known laws in many states already dictate how often certain workers must be paid. Connecticut, for example, requires weekly pay, though the state’s labor commissioner can approve a longer interval, up to one month. A similar rule is used in Virginia, where most wage earners must be paid every week, but those making more than 150% of the average wage may be paid monthly if the employee agrees. State governments could update these labor laws, or the federal government could step in and create a national standard. Either way, by creating a legal imperative, such policies would likely spark technological innovation as employers adapt their payroll systems to comply.

The Federal Reserve could also play a constructive role by accelerating automated clearinghouse (ACH) transfers.Today, millions of Americans wait up to three days for their paychecks to clear, far slower than many other countries. Though concerns about the heightened potential for fraud under a system of faster payments are justified, we have the technological wherewithal to make ACH transfers both safe and instantaneous. If the government does not act, financial companies may well take the initiative themselves. Of course, the same technology that allows paychecks to be deposited quicker also allows bills and other charges to be debited quicker. So while quicker payments may help reduce lag time between work and pay – as well as increase certainty about the timing of transfers, which eases planning burdens – it is not a holistic solution.

Of course, the more traditional role for government – regulating bad actors – also remains important. Last year, the Consumer Financial Protection Bureau (CFPB) issued a rule governing prepaid card paychecks, or “paycards,” an increasingly popular way for large corporations to quickly, securely, and cheaply pay their workers. Worker advocates argued that, because some of the cards included large and unavoidable fees, they could be unfair and costly to workers. The CFPB rule limited fees, mandated certain disclosures, and established safeguards against fraud, but it remains to be seen if these requirements will decrease the availability of these financial tools, which, for all their flaws, are likely giving some workers more immediate access to their earnings than they would otherwise have.

By setting clear guidelines on what employers and financial service providers can and cannot do, the government not only protects consumers, but also helps spur innovation. For example, many employers worry that offering their workers a pay advance option could make them a “lender” in the eyes of regulators – despite these products being designed to avoid such a result. State wage and hour laws also include confusing and onerous requirements governing for which purposes employees can direct payroll deductions and whether employee requests for payroll deductions must be in writing. Providing regulatory certainty and clarity in this area could free employers to experiment with new approaches.

By setting clear guidelines on what employers and financial service providers can and cannot do, the government not only protects consumers, but also helps spur innovation. For example, many employers worry that offering their workers a pay advance option could make them a “lender” in the eyes of regulators – despite these products being designed to avoid such a result. State wage and hour laws also include confusing and onerous requirements governing for which purposes employees can direct payroll deductions and whether employee requests for payroll deductions must be in writing. Providing regulatory certainty and clarity in this area could free employers to experiment with new approaches.

EMPLOYERS

The prospect of cutting more frequent paychecks understandably triggers questions from employers about administrative costs (most payroll providers charge employers each time they run payroll). But quicker and more frequent pay could also deliver benefits to the employer in the form of a less financially stressed, and thus more productive, workforce. Eighty-five percent of one pay advance firm’s customers report being more motivated and productive at work, for example. And one large US retailer found that three-fourths of their workers who used a payroll advance product reported fewer unplanned absences. With these outcomes in mind, several employers have instituted new payment systems:

- Lyft—In December 2015, this ride-sharing app unveiled “Express Pay,” allowing drivers (who are technically classified as independent contractors, not employees) to cash out their wages after they reach at least $50 in earnings. Powered by the technology company Stripe, the instant pay feature costs $0.50 per transaction and transfers the money to a debit card within minutes (though some banks require an extra business day).

- Uber quickly followed suit in June 2016, offering “Instant Pay” to all drivers with at least two weeks or 25 rides under their belt. Like Lyft’s “Express Pay,” Uber uses the ATM networks (rather than ACH) to make the transfers, so in most cases it is instantaneous. Uber also provides an option to waive the $0.50 transaction fee if the worker uses an Uber-provided debit card from GoBank.

- Goodwill of Silicon Valley—At the end of 2015, this nonprofit began giving its workers the option of withdrawing up to half of their already accrued wages, up to $500, before payday. Each transaction costs $5, but Goodwill pays half. PayActiv provides the underlying technology and the cash for the pay advances.

FINANCIAL SERVICE AND PAYROLL PROVIDERS

When employers – as well as workers themselves – decide they want to access their pay earlier and faster, they must turn to the technical experts – financial service and payroll providers – to operationalize the new policy. A few companies are specializing in this sort of innovation:

- Instant Financial – This Canadian company is testing a software application that would integrate with payroll systems, like those provided by ADP, PeopleSoft, and Ceridian, to disburse up to 50% of already-earned pay instantly and for free. The only catch: the money must be sent to a prepaid MasterCard, which can be subject to ATM and inactivity fees. Instant plans to make its money by taking a portion of the card fees charged to merchants on each transaction.

- FlexWage Solutions – Founded in 2010, this company offers “WageBank,” on-demand pay that integrates with employers’ payroll and workforce management systems. Employees can transfer their earned wages instantly to their prepaid debit card for a $5 fee. Employers determine the percentage of net wages to make available early, as well as the frequency with which employees can access it. In 2015, FlexWage was added to payroll company ADP’s cloud Marketplace, making it easier for ADP clients to offer the benefit. FlexWage currently has over 250 employers and 20,000 employees on their system.

- Activehours – Founded in 2013, this startup enables workers to access between $100 and $500 of their earnings before payday. Activehours is unique for three main reasons: (1) though it has started to collaborate with certain employers, the service model does not require employer engagement – the app has its own method for verifying employment information and wage levels; (2) there are no fees, though optional tips are encouraged and, according to the company, the resulting revenue stream makes it a sustainable business model; and (3) the app identifies upcoming recurring expenses to ensure you’ll have enough money in your checking account to cover your next bill. Workers at over 12,000 companies, including Starbucks, Target, and Walmart, have used the service.

INNOVATION #2: SMARTER PAYCHECKS

Even if paychecks remain at their current frequency, there are ways that paychecks could be made smarter through dynamic withholdings, automatic bill pay, and customizable paydays. These strategies are consistent with the idea that making pay more readily available is less important than better aligning it with predictable, fixed expenses like rent, utility bills, and food. Smarter paychecks can also help workers build up rainy day savings – which can be used to cope with less predictable financial shocks like car breakdowns, medical bills, and housing repairs – though EPIC explores that potential in a separate brief and so won’t focus on it here.

There is evidence that households are already trying to align income with expenses in various ways. For example, one study found that household spending increases considerably – particularly on durable goods like vehicles – in months directly after five-Friday months. This indicates that consumers are using a heuristic that earmarks the “extra” paycheck for lump sum purchases of large-scale items.

However, there are several additional ways that governments, employers, and financial service and payroll providers can help make paychecks better suited to today’s volatile financial world.

GOVERNMENTS

One particularly interesting idea is frontloaded or delayed payroll tax withholding to artificially increase the size of paychecks right before expenses like rent and utilities are due. For example, a worker who normally receives $423.50 each first Friday of the month ($500 in wages minus 15.3% in federal payroll taxes, assuming for simplicity that no federal or state income tax is withheld) could instead get the full $500, and then have that foregone $76.50 be taken out of the next paycheck two weeks later (if owed another $500 in wages, take home pay that period would be $347, or $500 minus $76.50 x 2). Under current law, most companies (those who paid $50,000 or more in payroll taxes the prior year) must transfer payroll taxes to the IRS within three to seven days after they cut their workers’ checks, or else face a late fee. Easing this requirement, or allowing for early payment – under the condition that any unpaid payroll tax must be used for the employee’s, not employer’s, benefit, and then paid back in the next paycheck – could lead to more liquidity for workers when they need it most.

More directly, the U.S. could follow the example set in Mexico, Indonesia, and Greece, among other countries, that require “extra” paychecks during culturally important – and thus high expenditure – months (Christmas, Ramadan, and Easter, respectively). Though if policymakers are interested in constraining, rather than encouraging, additional spending, creating an artificial windfall such as this may not be effective.

The government can also play a role in easing the path towards automatic payroll deductions for benefits like automatic bill pay or emergency savings accounts. In the retirement space, for example, it wasn’t until Congress shielded employers from state anti-garnishment laws in 2006 that automatic enrollment in employer-based retirement plans took off. A similar “safe harbor” from state wage and hour laws – like those on payroll deduction referenced above – is now needed so that employers can use an opt-out system for other important benefits like emergency savings accounts, automatic bill pay, or frontloaded payroll tax withholdings.

EMPLOYERS

Employers are increasingly aware that minimizing their workers’ financial stress can pay dividends in the form of higher motivation, fewer unplanned absences, and less turnover – all leading to greater labor productivity. In response, employers should consider non-traditional financial wellness benefits, including smarter paychecks.

- Catholic Charities of Fort Worth – This anti-poverty nonprofit is piloting “WageGoal”, a partnership between the on-demand pay company FlexWage (see above) and the nonprofit financial counselor Neighborhood Trust. This new financial service gives workers both early access to accrued pay (for a $5 transaction fee) and personalized financial forecasting to help employees manage their cash flow and avoid debt.

One idea that, at least to our knowledge, has not been tried is simply allowing workers to decide what day of the month they want to be paid. Though potentially complicated to administer, this could help workers better align income with expenses without increasing the frequency of the paychecks.

FINANCIAL SERVICE AND PAYROLL PROVIDERS

Several nonprofit and for-profit players are trying to make paychecks smarter:

-

- DoubleNet Pay –This Atlanta-based company gives workers the chance to save for an emergency, manage their debt, and pay upcoming bills automatically from their paycheck, giving workers a clearer view of what they can spend. A partnership with Empower Retirement has meant thousands of employers already offering retirement benefits can now easily add DoubleNet Pay’s services as an option for their workers.

- Painless 1099 –This financial technology start-up helps the growing number of independent contractors seamlessly meet their quarterly tax obligations, as well as pay for insurance and save for the future. Painless 1099’s customers, who include “contingent” or “gig” workers like Uber drivers, real estate agents, and landscapers, often have highly volatile incomes and don’t benefit from automatic tax withholding on the job.The firm makes real-time calculations based on a sophisticated algorithm that considers money coming in, federal and state tax brackets, and the worker’s projected income at the beginning of the year, and then automatically deposits the necessary funds in a back account specifically earmarked for future tax payments, insurance premiums, or savings.

- EarnUp – Though not directly connected to the paycheck, this fintech star t-up automatically sets aside small sums of money as income comes into a customer’s checking account, and then uses that money to pay down debt in the most efficient way possible. Launched in 2016 with $3 million in seed funding, the company is still in early stages, but it has already secured partnerships with Common Cents Lab and the Financial Solutions Lab.

HARNESSING THE PAYROLL MOMENT: PRINCIPLES FOR FUTURE ACTION

A number of innovators recognize the promise of the payroll “moment” to help workers cope with income and expense volatility and, ultimately, improve their financial security. But not all promising innovations bear fruit. To maximize effectiveness, reformers in all sectors should keep the following lessons in mind:

Interventions must be dynamic, automatic, and customizable. Spikes in income don’t always match up with spikes in expenses. The size and direction of fluctuations are hard to predict – and sometimes even hard to fully perceive while they’re happening. The financial choices consumers face are complicated and cognitively taxing. In such a dynamic environment, financial tools that are static, inflexible, and require heavy user management are no help. For example, an app that prompts a user to send the same amount from each paycheck into an emergency savings account, no matter the household’s financial situation that month, is of limited benefit. Instead, interventions must be automatically dialed to users’ unique circumstances.

Employers are critical partners. Though some innovators are trying to create workarounds, the payroll “moment” is, by definition, an employer-based opportunity. Employers are the ones doing the paying, and they have the sole power to change payment practices at scale. Innovators should keep this in mind and must continue making the case to firms that a more financially secure workforce is good for their bottom line. One tension here is that, while workers seem comfortable receiving financial services through their job, they can be reticent about sharing details about their financial lives with their employers. There seems to be an opportunity, then, for third-party providers to leverage the employer delivery channel while building their own relationships with workers.

Payroll providers should join the party. A number of startup payroll providers, including Payable and Gusto, are thinking creatively about servicing a 21st century workforce. Larger providers, like ADP, Paychex, and Ceridian, have experimented around the edges, but have generally been slow to embrace innovations. For now, their place atop the industry hierarchy is not in question, but if they’d like to stay there long-term, they must be willing to adapt.

Humans aren’t always rational.Though it may seem paternalistic, there are drawbacks to simply giving workers access to all their earnings in cash as they accrue. Given what we know about mental accounting, hyperbolic discounting, and the importance of commitment devices, a more promising intervention would automatically send accrued earnings to where they are needed most – whether that is paying down credit card debt, funding a rainy-day savings account, or taking advantage of an employer match in the company’s retirement account – rather than just directly into the worker’s pocket, where, as the saying goes, it is liable to burn a hole.

The economic experience for American workers has transformed in recent decades, but the paycheck moment has not. As incomes have grown more volatile, the job market more unstable, and family’s finances more precarious, the paycheck has remained relatively infrequent and inflexible.A quicker and smarter paycheck is long overdue and, if realized, could help millions of hard-working Americans improve their financial security.

For Endnotes and Works Cited, please download the PDF version of this Issue Brief.

● Acknowledgements

EPIC would like to thank David Mitchell for writing this brief; Katherine Lucas McKay for coordinating the internal deliberative process resulting in this series of solution-focused issue briefs; Colleen Briggs, Kiese Hansen, Gracie Lynne, Katherine Lucas McKay, Anne Romatowski, Joanna Smith-Ramani, and Evelyn Stark for reviewing drafts and making invaluable suggestions; Cathy Beyda, Ace Callahan, Pamela Chan, Brian Cosgray, Arlyn Davich, Frank Dombroski, Doug Farry, Timothy Flacke, Fiona Greig, Pete Isberg, Callum King, Sherazade Langlade, Ram Palaniappan, Jason Perkins-Cohen, Dan Quan, Frank Santoni, Arjan Schütte, and Steve Utkus for the time and wisdom they shared on the topic; and Laura Starita at Sona Partners for designing the template used to layout this brief. EPIC would also like to thank all those who completed the expert surveys or participated in EPIC’s many income volatility-focused convenings. While this document draws on insights shared at these EPIC forums and by the aforementioned individuals, the findings, interpretations, and conclusions expressed in this report – as well as any errors – are EPIC’s alone and do not necessarily represent the view of EPIC’s funders or Advisory Group members. Finally, EPIC thanks the Ford Foundation, and the W.K. Kellogg Foundation for their generous support.

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved