The Issues | What We Know | Sep 2016

●●●●

● Summary

The Expanding Prosperity Impact Collaborative (EPIC), an initiative of the Aspen Institute’s Financial Security Program, will target a consequential consumer finance issue to explore in depth for a defined period of time. In its inaugural year, EPIC is focusing on income volatility. EPIC’s purpose is to synthesize insights to build a more accurate understanding of how income volatility impacts low- and moderate-income families and how best to combat the most destabilizing dimensions of the problem. The EPIC process includes identification and synthesis of data, convenings of crosssector experts, surveys of a broader group of experts and leaders, and dissemination of issue briefs. EPIC’s look at income volatility will conclude with a set of concrete recommendations for moving forward.

EPIC’s first issue brief, “Income Volatility: A Primer,” was a comprehensive literature review of what is known about the prevalence, causes, and impacts of income volatility. This second brief looks at managing income volatility at both the household and societal levels. It presents a framework for thinking through possible solutions. Though the conclusions reached are EPIC’s alone, this brief was informed by and should be considered part of the EPIC process Most notably, many of the policy ideas outlined below were unearthed through the expert surveys we administered earlier this year, and the framework itself was workshopped and refined during a two-day convening we hosted in June. Additional information on each claim and policy proposal in this brief, as well as sources, can be found in the Endnotes.

● Issue Brief

THE PROBLEM

As detailed in the first brief, volatility refers to household financial flows that are inconsistent and sometimes unpredictable. Fluctuations in Americans’ income appear to be larger, more frequent, and more widespread than in the past. Eight-seven percent of EPIC expert survey respondents consider income volatility to be a major or critical problem facing the country, and 83% expect income volatility to increase over the next ten years. Instability in labor market earnings, in non-labor transfers (such as public benefits and child support), and in household configurations lead to year-to-year as well as intra-year income shifts. Although some households at times welcome volatility – for example, choosing to work in industries that pay large bonuses or based on commission – most low- and moderate-income families would prefer stability. Those with unwanted volatility find it hard to cope with the fluctuations and plan for the future, suffering harms that include foregone savings and investment opportunities, instability around basic needs such as housing and food, and even negative child development outcomes.

"Eighty-seven percent of EPIC expert survey respondents consider income volatility to be a major or critical problem facing the country, and 83% expect income volatility to increase over the next ten years."

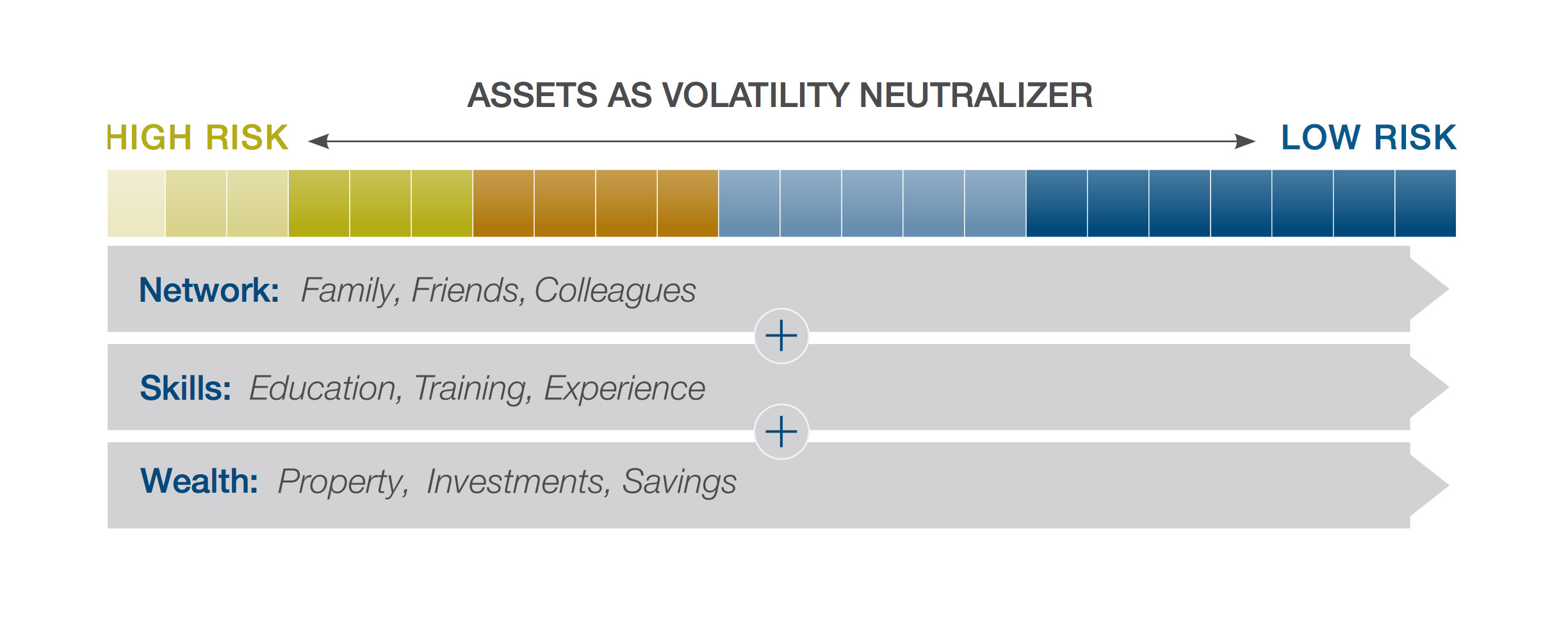

Volatility appears to be highest among the lowest-income households. The degree to which it is problematic depends in large part on the portfolio of assets available to the household. For those who can fall back on wealth or a robust support network or highly-marketable skills or experience, income volatility is more likely an inconvenience than a serious burden or obstacle. For those with less asset protection, volatility can present a significant challenge.

CURRENT MANAGEMENT STRATEGIES

Managing income volatility encompasses a spectrum of strategies to prevent it from happening and to mitigate its effects when it does occur. Workers can seek jobs with more consistent hours and pay. A secondary earner can move in and out of the labor force as needed. Unemployment compensation can cushion the blow of a layoff. Other insurance can protect against large, unpredictable expenses such as health care. Savings built up during good times can help with meeting expenses when times are tough. Borrowing can bridge a gap and takes many forms, from tapping credit cards, home equity, and retirement accounts, to putting off bill payments, incurring overdrafts, or leaning on family and friends.

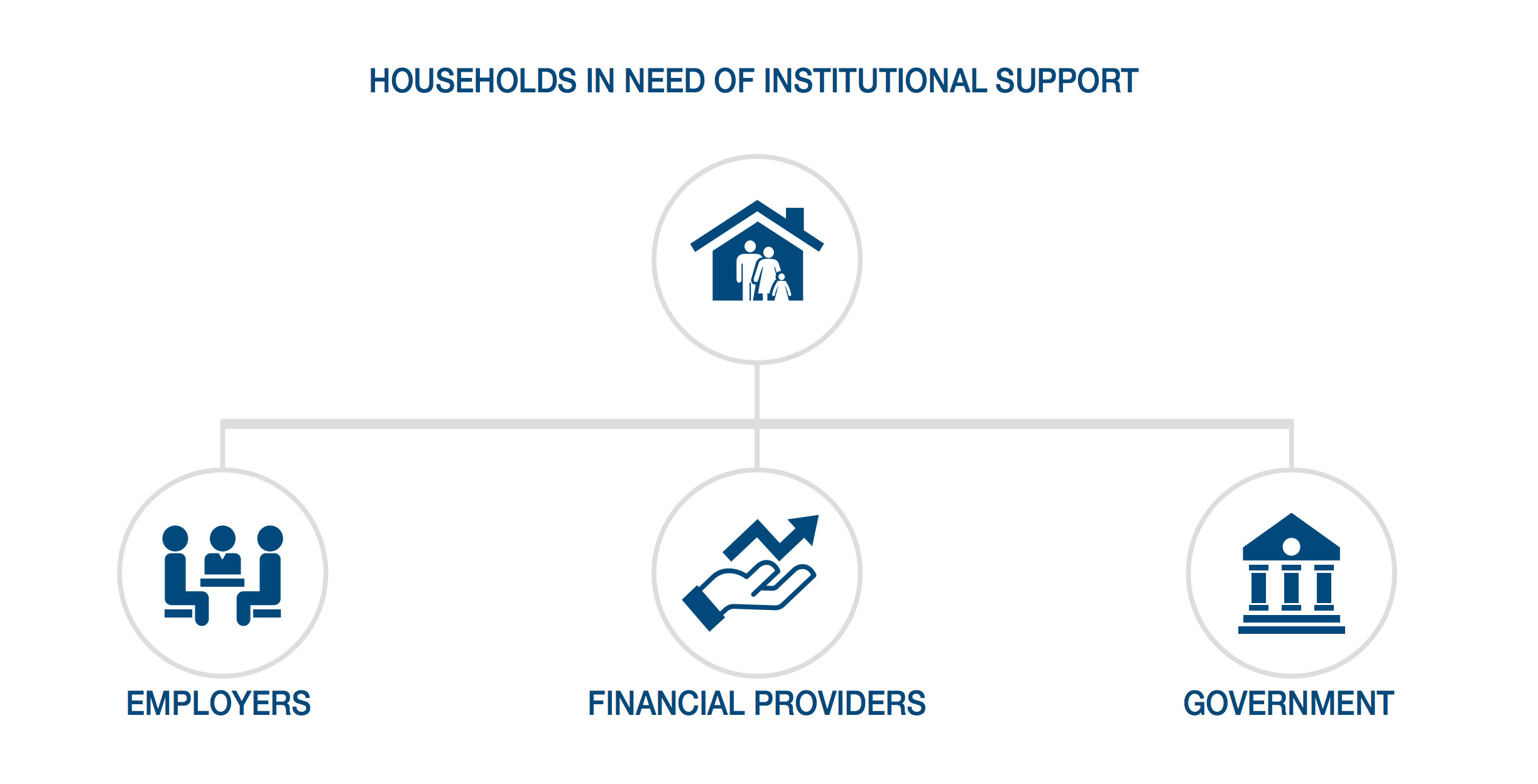

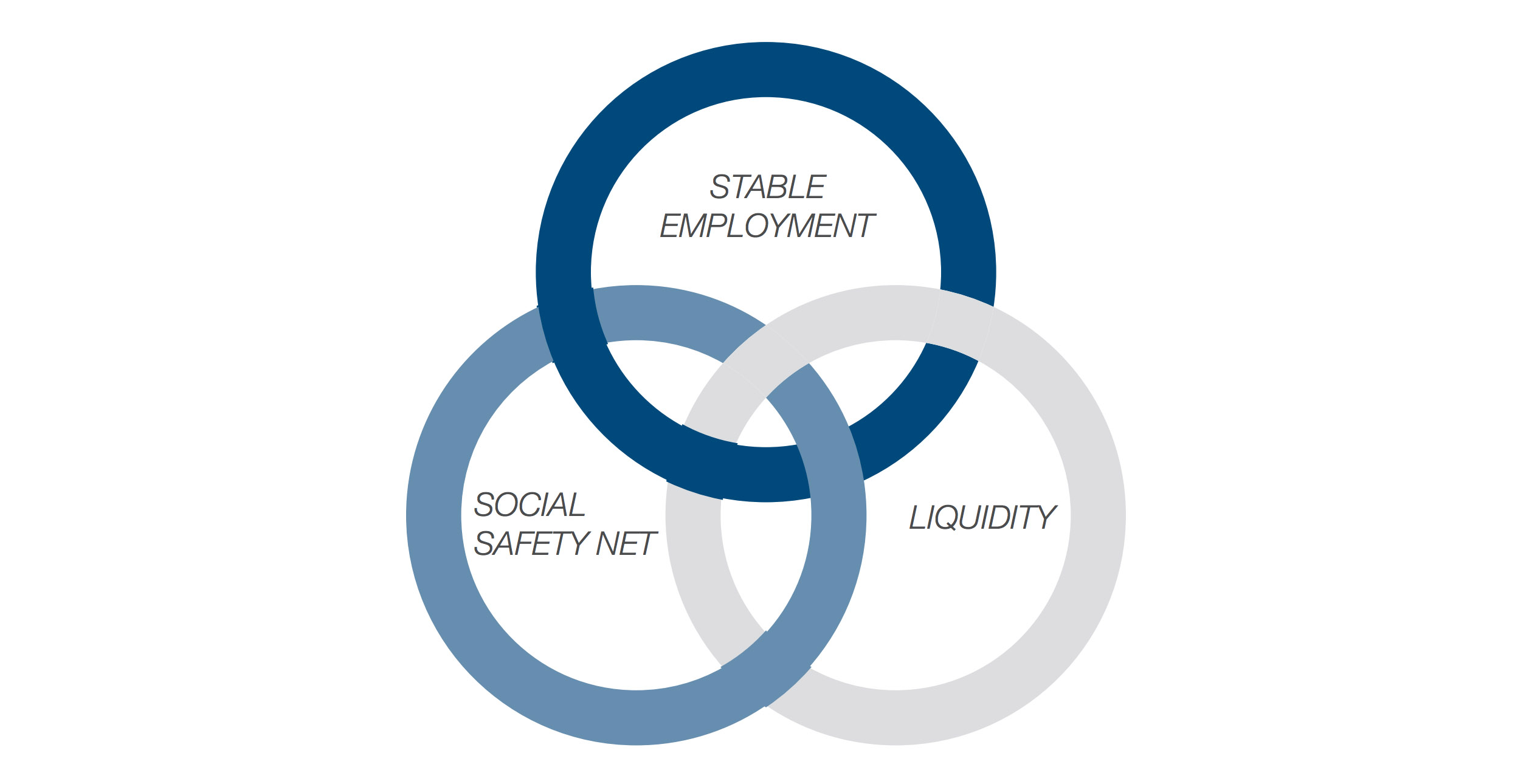

To better understand households’ options, we’ve divided these management strategies into three main categories, roughly positioned along the spectrum of prevention to mitigation: securing stable employment, accessing the social safety net, and relieving liquidity crunches.

"Having a steady job that provides a predictable flow of earnings offers the best protection against income volatility."

SECURING STABLE EMPLOYMENT

Having a steady job that provides a predictable flow of earnings offers the best protection against income volatility. Yet this can be difficult for workers to achieve. Employers increasingly seek efficiency – and competitive advantage – through independent contracting strategies and “just-in-time” scheduling that tends to make earnings highly variable and unpredictable, and stable employment scarce. As described in the first brief, around half of the low-wage workforce is subject to precarious scheduling (such as lack of input on the hours to be worked and little advance notice of shift changes or cancellations); and over 40% of Americans who Having a steady job that provides a predictable flow of earnings offers the best protection against income volatility. 5 report variable monthly income blame it on an irregular work schedule. Even jobs with steady hours can generate a volatile income stream due to performance-based pay, irregular pay periods, or lack of paid time off.

There is no sign that these trends will abate. In the current environment, low-wage workers have little workplace bargaining power to demand stability. And the traditional concerns of employment law – minimum wage, overtime pay, protection against discrimination – largely do not affect these practices.

ACCESSING THE SOCIAL SAFETY NET

Some public benefit and social insurance programs are explicitly designed to shield workers from the vagaries of the labor market and provide basic income during times of economic deprivation. But these programs have proved poorly suited for an era of increased income volatility, when beneficiaries are facing multiple, short-term financial shocks every month, as opposed to long-term spells of unemployment or chronic poverty.

• Unemployment insurance: Despite unemployment compensation’s role as the country’s main social insurance safeguard against employment-related volatility, it is not available to all workers in all industries. One study found it was a resource for only one in five households affected by unemployment – and it doesn’t help at all if, rather than being laid off, a worker’s hours are reduced. Those who are able to take advantage of it were usually working full-time when they lost their jobs; those who are part-time, temporary, or self-employed usually do not qualify for assistance.

• Work supports and other anti-poverty programs: Public poverty amelioration programs – in-kind benefits such as the Supplemental Nutritional Assistance Program (SNAP), Medicaid, the Low Income Heating and Energy Assistance Program (LIHEAP), and Housing Choice vouchers, as well as cash assistance – provide varying degrees of support for households trying to smooth income and expenses. However, as noted in the first brief, these benefits are not typically responsive to short-duration shifts in income and thus cannot fully mitigate that instability. They also carry heavy transaction costs to establish and maintain eligibility. The tax code (most notably, the Earned Income Tax Credit [or EITC], but also the Child Tax Credit) plays a prominent role in the income support safety net, but how the benefits are delivered – via a lump sum check once a year – actually exacerbates volatility. Furthermore, the credit amount itself can go down as wages or hours decrease, making dips in income even more pronounced.

RELIEVING LIQUIDITY CRUNCHES

Savings, credit, and insurance offer opportunities for households to mitigate the liquidity challenges resulting from income volatility, but most of the currently available financial tools are not well-designed for income volatility or, worse, are designed to predatorily exploit the vulnerability of those facing income shocks.

• Savings: For many, savings function primarily as a short-term emergency or precautionary “buffer stock” to finance consumption when income is low, lessening material hardship. However, only a fraction of households meets their emergency savings goals, and about half do not have any emergency savings. They may know they need more set aside, but they often underestimate how much and, regardless of goal, fall short of what is actually needed to cover unexpected shocks. In part, this is due to a dearth of attractive and accessible savings products. Automatic enrollment in workplace savings accounts is by far the most effective way to get workers saving, but employers rarely offer that benefit to low- and moderate-income employees, and, when they do, the savings account at issue is usually restricted to use in retirement, and not accessible for week-to-week consumption smoothing or emergencies.

"Most of the currently available financial tools are not well-designed for income volatility."

• Credit: Accessing credit can be an effective way for households to cope with financial shocks. Secured debt – using asset ownership as collateral to obtain cash, such as with a home equity loan or line of credit, a car title, or a retirement account – is an option for some, but more widespread is the use of unsecured debt – principally credit cards. Dubbed the “plastic safety net,” unsecured credit cards often charge exorbitant interest rates and late fees, quickly trapping borrowers in a cycle of debt. Furthermore, those with restricted access to mainstream secured or unsecured debt – the lowest-income households and others with poor credit ratings, but also more well-off borrowers whose fluctuating income does not fit standard underwriting models – may have to resort to “alternative financial services” or “small dollar credit” such as payday advance loans. These loans often come with even higher interest and fees than those charged by credit cards and tend to rollover and accumulate, creating long-term challenges for the borrower. Most of the currently available financial tools are not well-designed for income volatility.

• Insurance: For most, insurance (principally health, homeowners/renters, and automobile) is a hedge against expense volatility. Income protection may be available from life insurance (mitigating household volatility when there is loss of income due to death of a working family member) or employer-based or personal disability insurance, but these (as well as employer-based health insurance) are often inaccessible to lower-wage workers and those with part-time or variable hours.

• Real-time payments: Even as the digital revolution has dramatically accelerated the pace of economic interactions, key elements of the financial services infrastructure are mired in traditional processes that restrict liquidity. Essentially, the current “rails” that financial transactions move on could be faster. Workers with limited liquidity are waiting additional days to have their earnings or other payments credited to their account, reducing their liquidity and ability to meet obligations. It is noteworthy that the current system also results in money being debited out of a person’s account more slowly too – which may be a benefit when someone is liquidity-constrained.

A SOLUTIONS FRAMEWORK

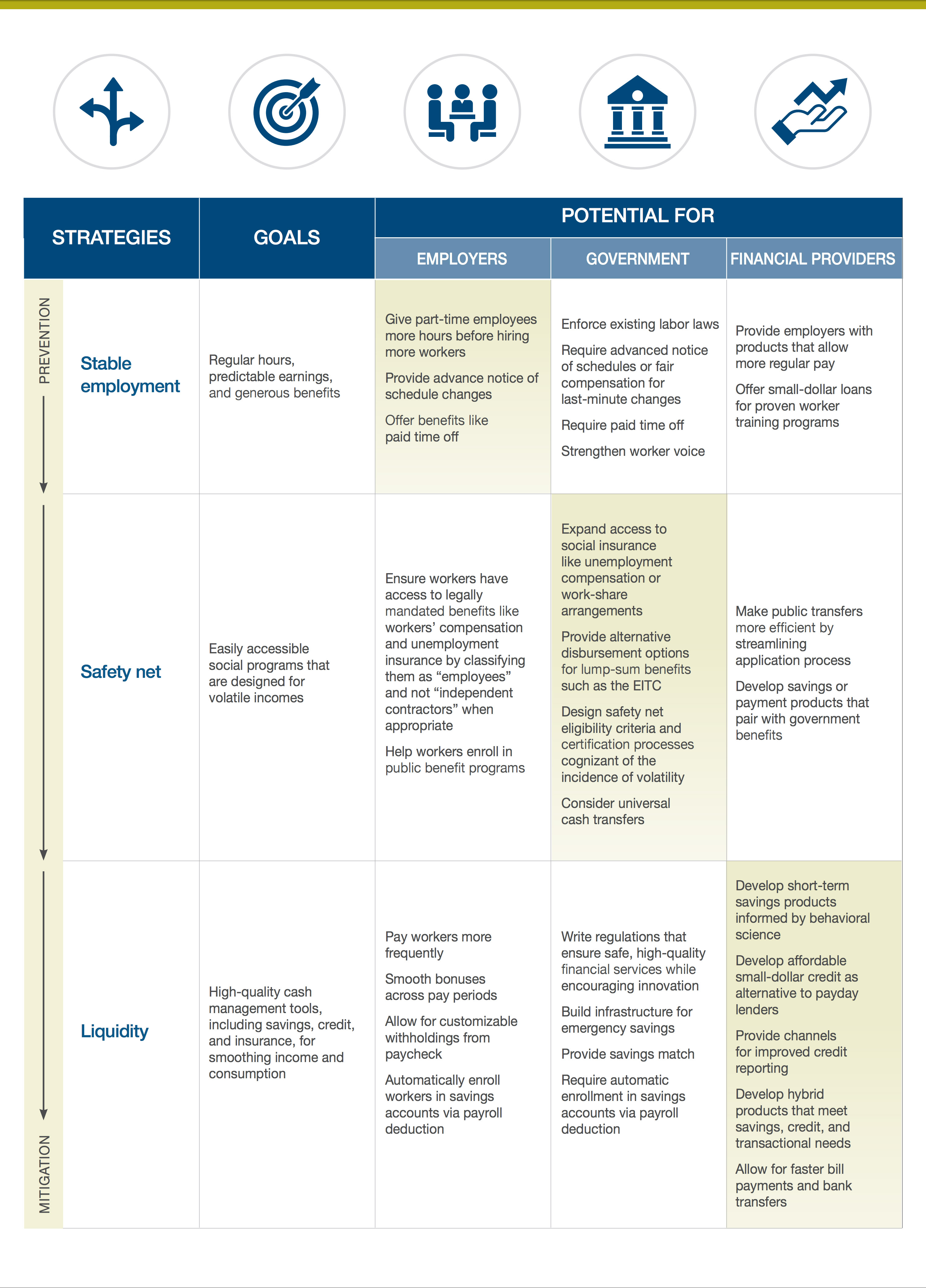

The current strategies for managing income volatility are proving unavailable or inadequate for those most negatively affected. Low- and moderate-income households need a better tool kit. EPIC believes building a set of effective prevention and mitigation solutions first requires creating a framework that clarifies objectives and identifies possible roles for key actors.

The table on page 9 presents such a framework. For each of the three main categories of identified strategies, there are goals and specific functions employers, government, and financial service providers could play. These proposals – which are not recommendations, but simply potential approaches to address the problem – are explored in greater detail in the following section.

Not explicitly present in the framework is the role households experiencing income volatility should assume. This reflects neither a denigration of their agency nor an abdication of personal responsibility. Households will inevitably be the ones making consequential decisions about managing volatility. But one of the most problematic elements of the current environment is that the actors with the fewest resources – the low- and moderate-income households directly affected – are bearing an increasing share (perhaps even most) of the risk and responsibility (what Jacob Hacker observes as the “great risk shift”). The institutional actors identified in the framework can, and must, do much more.

In considering the framework, it is also important to recognize that the three strategic categories sit along a spectrum of prevention to mitigation and sometimes address both. Furthermore, the strategies do not exist in isolation from each other but for any given household may be quite interdependent and connected. For example, in order for a worker to find a new, more stable job, he may need access to government benefits or personal liquidity to afford the requisite training or job search effort.

THE FRAMEWORK APPLIED

This section of the brief populates the solutions framework with specific, potential interventions, informed by a review of the income volatility literature, feedback from EPIC’s expert panels and June convening, and a survey of current innovations in the field. The institutional actors vary in the centrality of the role they play for each strategy, and the lead actor is listed first (or shaded, as in the table on page 9). Two key considerations underlying any application of the framework are: (1) scale (can an intervention be sufficiently large and/or pervasive to be effective in managing income volatility?), and (2) achievability (can an intervention be sufficiently practical to warrant allocation of potentially scarce resources to pursue it?).

SECURING STABLE EMPLOYMENT

• What employers can do: Workplace practices that make employment less secure (and earnings more volatile) belie an assumption that reducing investment in labor maximizes profits. However, there is evidence to the contrary, meaning there can be employer selfinterest in keeping workers happy by curtailing income volatility. Shareholders and even customers have a role to play in encouraging companies to become more worker-friendly while benefiting the bottom line. Predictable scheduling practices and responsive payroll processes are key (see sidebars on pgs. 11 and 15 respectively).

"Labor and employment law can better ensure a sharing of economic risk in the workplace."

• What government can do: Better enforcement of existing labor market regulations might reduce employment-related income volatility, but there is also a role for new public policy approaches. Labor and employment law can better ensure a sharing of economic risk in the workplace. Some existing labor protections interact with the current worker classification system to encourage employers to use independent contractors rather than full-fledged employees, which has led many to propose improvements. Government can also facilitate benefit systems for workers that help reduce volatility, such as paid sick or parental leave.

Of growing interest are regulations directly addressing the problems arising from “just-in-time” scheduling (see sidebar).

The government can also ensure stable employment is always available, either by hiring otherwise unemployed workers itself or partnering with private firms to deliver “subsidized jobs,” an approach that has proven effective in certain circumstances.

• What financial service providers can do: Financial firms will likely play a limited role in job quality improvement efforts, but there are channels through which they can affect positive change. For example, new financial products can help employers pay workers more frequently than the customary once every two weeks (see sidebar on pg. 15). And well-designed small dollar loans could help workers afford training programs that will make them more valuable employees.

• What financial service providers can do: Financial firms will likely play a limited role in job quality improvement efforts, but there are channels through which they can affect positive change. For example, new financial products can help employers pay workers more frequently than the customary once every two weeks (see sidebar on pg. 15). And well-designed small dollar loans could help workers afford training programs that will make them more valuable employees.

ACCESSING THE SOCIAL SAFETY NET

• What government can do:

o Unemployment insurance: Unemployment compensation is not achieving its potential as a frontline defense against income volatility, but policymakers have several options for fixing this (see sidebar on pg. 12).

o Broader earnings insurance: As the stability of the connection between employers and employees erodes, portability and universality become more critical. One approach for insuring financial stability regardless of the vagaries of a particular job is to establish publicly-backed, employee-funded savings accounts that could be drawn from in lieu of unemployment compensation. Facilitating development of stand-alone private-market wage insurance could also specifically target volatility by covering drops in wages or hours.

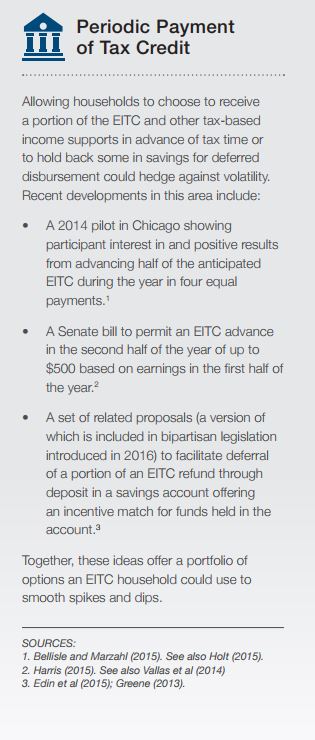

o Taxes: Alternatives to single, annual payments of safety net tax credits could hedge against volatility (see sidebar on pg. 13). Making more tax-based benefits refundable could smooth the effects of year-to-year volatility, as could viewing tax liability through a multi-year lens.

o Eligibility criteria for safety net programs: The mitigation value of traditional safety net programs could be bolstered by designing eligibility criteria and processes cognizant of the incidence of volatility. Depending on the resources and nimbleness of the government agency involved, this can involve making programs more responsive to changes in income, so that benefits flow to those truly in need, even if only for a few weeks, or less responsive, so that short-term swings don’t create unnecessary and administratively burdensome churn in and out of the program.

o Universal cash transfers: The worst consequences of income volatility for those affected – and for the larger society and economy – come to those who lack adequate income. Universal income supports – such as a basic guaranteed income or general child allowance – would provide a floor of stable monthly payments and may become increasingly important as technological change erodes demand for labor.

• What financial service providers can do: While the provision of public benefits and social insurance is necessarily a government function, private firms in both the finance and technology industries could help make public transfers more efficient, either by streamlining the application process for beneficiaries or developing low-cost savings or payment products that could pair with government benefits.

• What employers can do: Eligibility for many government benefits that can combat income volatility, including unemployment insurance and workers’ compensation, requires a bona fide employer-employee relationship. There is evidence, however, that many employers, either purposefully or unwittingly, misclassify their employees as independent contractors, thus denying their workers important protections. More accurate classification of worker type – in addition to simply hiring employees instead of independent contractors – could help improve access to the safety net.

RELIEVING LIQUIDITY CRUNCHES

• What financial service providers can do:

o Savings: The private market can enhance savings by incorporating insights gained from behavioral research into product design and execution. This includes creatively employing both personal goals and past experience as motivators, using frequent reminders, balancing easy access to saved funds with liquidity barriers, providing incentives, and incorporating both automatic and opportunistic elements. Emergency savings can be accumulated using motivations tied to gift-giving and prize-winning. Some product proposals focus explicitly on building savings habits rather than aiming for a specific savings target.

o  Credit: With respect to credit, the role of traditional financial services providers to supply volatility management tools remains uncertain. A FDIC pilot giving banks the opportunity to make low-cost small dollar loans saw some success, but the experiment ultimately did not provide a viable alternative to payday lenders. Credit unions have historically been more effective at offering this type of product but at very limited scale.

Credit: With respect to credit, the role of traditional financial services providers to supply volatility management tools remains uncertain. A FDIC pilot giving banks the opportunity to make low-cost small dollar loans saw some success, but the experiment ultimately did not provide a viable alternative to payday lenders. Credit unions have historically been more effective at offering this type of product but at very limited scale.

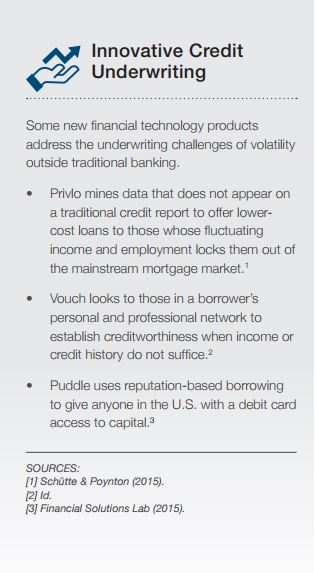

Credit scores are a key variable affecting access to credit products, but many prospective borrowers are “invisible” to the credit reporting organizations. Some alternative product innovations aim at credit score improvement by reporting financial behaviors – like paying rent – that have historically gone unreported (see sidebar).

o Insurance: There are many economic and regulatory barriers to entering the traditional insurance market, but technological advancements are lowering these hurdles, allowing for “friendsurance” and other unconventional pooling techniques to lower families’ risk of shouldering large expenses on their own. Auto insurance premiums can be better tied to risk and ability to pay using realtime tracking of miles driven. Microinsurance products (a fast-growing product in the developing world) could address the risks of small though consequential, unpredictable expenses such as car or appliance repairs.

o Multi-purpose products: Some products can simultaneously meet multiple consumer needs, such as facilitating spending, saving, and credit through a single account interface. Prepaid debit cards can be used to make purchases while also restraining spending and offering a “savings pocket” to build a reserve, as can secured credit cards. An app called Even helps workers manage income flow by holding money from above-average paychecks in a savings account that is drawn from automatically when pay is below average – or by providing an interest-free loan during below-average months if accumulated savings are insufficient.

• What government can do: The public sector’s regulatory oversight role can affect the private market products available to households. Improved public regulation of the private credit market – in particular, alternative financial services – could curtail the harm caused by products that exacerbate the negative consequences of experiencing volatility. However, regulatory approaches tend to have unintended consequences; it can be hard (though not impossible) to distinguish between “good” and “bad” products, and curtailing bad products can restrict access to needed liquidity.

Some policy initiatives provide an infrastructure supporting the kind of small savings that are useful as a hedge against volatility. The Treasury Department’s myRA program provides a no-fee, government-backed savings vehicle for workers without access to a retirement plan through their employer. An additional innovation would be permitting use of 401(k) accounts to build “rainy day” funds. The Department of Housing and Urban Development’s Family Self-Sufficiency Program puts public housing rent increases resulting from higher household earnings in a savings account available upon program graduation. This is one example of many possible tweaks in safety net programs to support accumulation of emergency savings and access to emergency credit.

Government can also provide incentives for households to save on their own, and there are a number of pending proposals to match contributions made to savings accounts.

• What employers can do: In addition to making earned pay available to workers on a more frequent basis (see sidebar on pg. 15), employers can look at paying bonuses over time rather than as a lump sum and using a “13th-month” payroll schedule that provides an extra paycheck in December when workers’ budgets are most stressed. Companies can also help facilitate savings by allowing – or automating – customizable withholdings from paychecks. Channeling a portion of a worker’s pay into an emergency savings account, for example, could help families build a financial cushion that will help relieve liquidity crunches and enhance their overall economic resiliency.

"Better managing income volatility will require a holistic approach that combines product innovation and policy reform; prevention and mitigation; and labor and financial services interventions."

THE ROAD AHEAD

Better managing income volatility will require a holistic approach that combines product innovation and policy reform; prevention and mitigation; and labor and financial services interventions. This brief identifies focal areas for this needed innovation, and it provides a solutions framework for analyzing who is best positioned to act and what promising practices those actors can pursue. That analysis is grounded in the emerging convergence EPIC has identified in its work to date: a thorough scan of the academic research and articles in the popular press; four expert surveys; and two expert convenings, one of which was spent intensively workshopping and refining this framework.

Yet even with this emerging convergence, significant uncertainty and disagreements remain. The path forward requires attention to three key questions: what works; at what scale; and at what cost. That analysis must look beyond a narrow view of effectiveness for the particular population studied to consider market viability broadly defined: the value proposition for attracting sufficient investment, the relative appeal among the competing priorities of public and private actors, and the anticipated reduction in the overall incidence of the negative consequences of income volatility. EPIC will tackle these questions as we prioritize two tracks of work in the coming months: (1) digging deeper into solutions to assess which are worthy of immediate action, real-world testing, or further research; and (2) building the committed leadership and networks needed to bring to market and policy the solutions that will most help Americans.

For Endnotes and Works Cited, please download the PDF version of this Issue Brief:

● Acknowledgments

EPIC would like to thank Steve Holt of HoltSolutions for synthesizing the research literature and writing this brief; David Mitchell for analyzing and categorizing the research base and solution options, and coordinating the research, writing, and editing processes; Judith Garber, Kiese Hansen, and Claire Garvin for research assistance; Ida Rademacher, Joanna Smith-Ramani, Tim Ogden, Michael Collins, Rachel Schneider, Kevin Jordan, Bradley Hardy, Charlotte Alexander, and Chuck Howard for reviewing drafts and making invaluable suggestions; the additional members of the EPIC Advisory Group – Marla Blow, Maureen Conway, Fiona Greig, Darrick Hamilton, Elisabeth Jacobs, Jonathan Morduch, and Caroline Ratcliffe – for providing feedback on an early outline; and Laura Starita at Sona Partners for designing and producing this brief. EPIC would also like to thank all those who completed the expert surveys or participated in either of the EPIC convenings. While this document draws on insights shared at these EPIC forums and by the aforementioned external reviewers, the findings, interpretations, and conclusions expressed in this report – as well as any errors – are EPIC’s alone and do not necessarily represent the view of EPIC’s funders or Advisory Group members. Finally, EPIC thanks the Ford Foundation and the W.K. Kellogg Foundation for their generous support.

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved