The Issues | What We Know | May 2016

●●●●

● Summary

EPIC has identified hybrid financial products as an emerging opportunity to help families that experience income volatility manage it successfully. Hybrid products combine the functions of two or more consumer financial products that are generally offered separately, integrated for the purpose of improving peoples’ capacity to effectively manage their money. This brief reviews the current research on how families cope with income volatility, identifies existing hybrid products that have demonstrated capacity to help, discusses the roles of the institutions best positioned to act – financial institutions, employers, and government – and recommends principles for further action.

● Background

The Expanding Prosperity Impact Collaborative (EPIC), an initiative of the Aspen Institute’s Financial Security Program, is a first-of-its-kind, cross-sector effort to shine a light on economic forces that severely impact the financial security of millions of Americans. EPIC deeply investigates one consequential consumer finance issue at a time.

EPIC’s first issue is income volatility, which destabilizes the budgets of nearly half of American households. Over the last year, EPIC has synthesized data, polled consumers, surveyed experts, published reports, and convened leaders, all in an effort to build a more accurate understanding of how income volatility impacts low- and moderate-income families and how best to combat the most destabilizing dimensions of the problem.

This brief on hybrid financial products is second in a series that will explore highly promising solutions to income volatility. Hybrid financial products are exciting new tools that can optimize how families with volatile incomes and expenses manage cash flow. Our hope is that this brief will support public and private leaders as they attempt to innovate, implement, regulate, and scale multi-function products and services that are flexible enough to meet consumers’ changing needs in the moment

● Issue Brief

HOUSEHOLDS WITH VOLATILE EARNINGS FACE HIGH COSTS TO MAINTAIN LIQUIDITY

There is wide consensus that income volatility—particularly intra-year volatility—is a pervasive problem for American households. Estimates vary. For example, JP Morgan Chase Institute finds that 41% of consumers experience month-to-month fluctuations in earnings of more than 30%, while the Federal Reserve (SHED) finds 32% of households report experiencing occasional to frequent monthly variations.

"Hybrid products combine the functions of two or more consumer financial products that are generally offered separately, integrated for the purpose of improving peoples’ capacity to effectively manage their money."

The key challenge for families experiencing income volatility is how to maintain liquidity and avoid financial instability. Many households do so using a combination of savings and credit. In fact, research demonstrates that these are substitute goods: when people lack savings, they use more credit, and when people lack access to credit, they build and use more savings. Moreover, many consumers view these tools as interchangeable, using whichever resource is available or more abundant to meet expenses when income is low. The most recent Survey of Household Economics and Decisionmaking (SHED) data indicates that households that lacked the cash and savings to meet a $400 expense would turn to a wide variety of alternatives, including credit cards, informal borrowing from family and friends, and high-cost alternative financial services such as payday or auto title loans.

This approach is intuitive but has several drawbacks. For one, the structure of our financial system makes it difficult to understand precisely how much liquid cash one has at any given moment. It also makes it challenging to foresee the potential consequences of using the wrong product. Transaction ordering and the lack of real-time payments mean that, even when a consumer checks their balance just before making a payment, they may be acting on outdated information. Furthermore, when people are worried about how they can pull together enough cash to meet expenses, they may not be as sensitive to the cost of various options. One might knowingly make a purchase that will require over-drafting their bank account, but not anticipate incurring three separate fees because of pre-scheduled payments that are charged later that day. Similarly, even though credit card interest rates are considerably lower than payday loan rates, 37% of payday borrowers report that, if a payday loan were not available, they might use a credit card to cover expenses.

MANAGING THE SWINGS: HOW FAMILIES DEAL WITH INCOME VOLATILITY

As we detailed in an earlier report, families at all income levels experience income volatility and, in recent decades, volatility has become both more common and more severe, especially for low- and moderate-income families. Income volatility makes it difficult to save, can push households into unwanted debt, and prevents people from planning for the future. Reducing income volatility at its source would be ideal but it is unlikely to happen in the near future. In fact, 83% of EPIC experts surveyed expect income volatility to increase over the next ten years.

The costs of living with income volatility are especially high for families  with few resources. Researchers have found that families coping with income and expense volatility delay food purchases, pay bills late, forego medical care, and use high-cost credit such as payday loans. Bania and Leete find that low-income households struggling with income volatility tend to experience greater deprivation now than in the past, largely due to the erosion of benefits such as welfare and food stamps. The stress of managing income volatility with limited tools doesn’t help: research shows that stress reduces people’s capacity to make good financial decisions, among other negative effects. For those with chronic financial stress, such as low-income families, the impact on people’s cognitive capacity behavior becomes pervasive, deepening their financial distress.

with few resources. Researchers have found that families coping with income and expense volatility delay food purchases, pay bills late, forego medical care, and use high-cost credit such as payday loans. Bania and Leete find that low-income households struggling with income volatility tend to experience greater deprivation now than in the past, largely due to the erosion of benefits such as welfare and food stamps. The stress of managing income volatility with limited tools doesn’t help: research shows that stress reduces people’s capacity to make good financial decisions, among other negative effects. For those with chronic financial stress, such as low-income families, the impact on people’s cognitive capacity behavior becomes pervasive, deepening their financial distress.

Expenses also contribute significantly to financial volatility. Recent research from the JP Morgan Chase Institute finds that households experience surprisingly intense month-to-month fluctuations in expenses. Families earning the median income, on average, saw monthly swings of $1,297 (29% of total average expenses). The report also determined that each year nearly 40% of households make at least one “extraordinary” payment related to medical care, taxes, and auto purchases or repairs—expenses that are inherently difficult to predict and plan for. An added challenge for households that experience both income and expense volatility is that the spikes and dips do not align, making it extremely difficult to budget, plan for the future, and manage new financial challenges with existing resources.

Given these facts, families that experience income volatility need ways to manage it more successfully. Consumers need financial products and services that more effectively and less expensively help them to smooth income and expenses and make the best use of their resources in the moment. Hybrid financial products have the promise to do just that.

HOW CAN HYBRID FINANCIAL PRODUCTS HELP?

If the critical challenge for families experiencing income volatility is maintaining sufficient liquidity even when income is low, solutions must be designed around how and when consumers use savings and credit to cover expenses. The very concept of a hybrid product is relatively new and loosely defined. At present, the only definition offered by financial regulators comes from the Consumer Financial Protection Bureau’s (CFPB) regulation on prepaid cards. The CFPB “uses the term ‘hybrid prepaid-credit card’ to refer to a prepaid card that can access both an overdraft credit feature… and the asset portion of a prepaid account.”

The Center for Financial Services Innovation (CFSI) defines hybrid products as “those that combine two or more traditional product categories.” Commonwealth refers to “integrated solutions” that “[combine] multiple financial functions, particularly savings and credit. EPIC’s working definition of a hybrid financial product is one that combines the functions of two or more consumer financial products that are generally offered separately, integrated for the purpose of improving peoples’ capacity to effectively manage their money.

Hybrids are distinct from previous financial innovations because they are, to a greater extent, designed more elegantly around how consumers lead their financial lives and actual use cases for use the variety of products available to them rather than designed around a single specific function such as transacting. As Commonwealth puts it:

While these single-focus solutions have served many Americans well, they reflect the structures and competencies of financial service providers... Customers shouldn’t have to think like providers of financial services. They should be able to lead their lives, and turn to well-crafted solutions that address their needs as they arise. Ideally, people could reach for one solution when a need arises, and trust that the tool they grab will activate whatever financial functions are necessary to address their need.

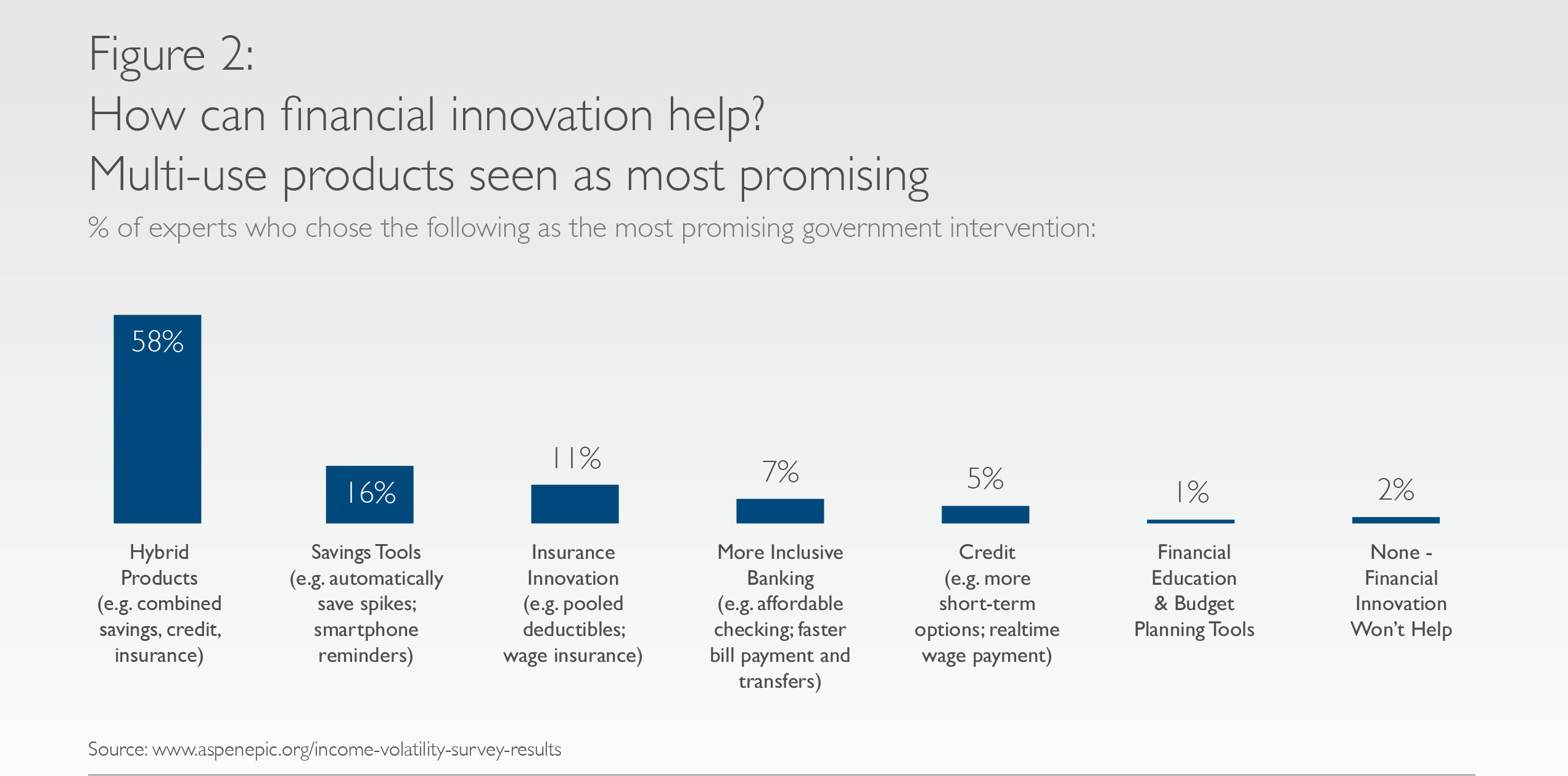

Hybrid products have increasingly gained attention from nonprofits, private firms, and governments that see them as promising innovations to boost vulnerable households’ financial security and develop potentially lucrative new markets in consumer finance. Among respondents to EPIC’s expert surveys, 56% selected hybrid products as the single most promising financial innovation to address income volatility (the next most common response was selected by just 16%). For several years, nonprofit organizations have pioneered hybrid “borrow and save” products, such as the Twin Account from Local Initiatives Support Coalition (LISC) and Justine Petersen Housing and Reinvestment Coalition. LISC offers a $300 loan product. As clients repay the loan, they build positive credit history and emergency savings funds. More recently, the private sector has begun investing heavily in hybrid products. CFSI reports that more than half of the nearly 300 applicants to its 2016 Financial Solutions Lab—an incubator focused on products for underserved consumers—offered multi-function products. Government’s interest is two-fold. On one hand, there are concerns about how to handle innovations that cross regulatory boundaries; on the other hand, some agencies have recognized the role that hybrids can play in advancing financial inclusion.

"Simplicity, flexibility, and complimentary functions can make a real difference in consumers’ ability to make ends meet despite the unpredictability and uncertainty facing those who struggle with income volatility."

For consumers, hybrid products offer the potential for greater access, affordability, simplicity, efficiency, and effective management of liquidity. For consumers who lack access to the full range of mainstream financial products, hybrids are an opportunity to use a product the consumer already has to provide access a complementary product that may be more appropriate in a given situation. These products could enable users to more easily understand which of their resources are most appropriate for certain situations, or even automatically select the most advantageous option. These products could also simplify financial management by reducing the number of products and accounts consumers must maintain. Simplicity, flexibility, and complimentary functions can make a real difference in consumers’ ability to make ends meet despite the unpredictability and uncertainty facing those who struggle with income volatility.

HYBRID FINANCIAL PRODUCTS CURRENTLY ON THE MARKET

Most of the hybrid products currently available to consumers address transactions, savings, credit, budgeting, and income payments. They fall into four basic categories, presented below with examples from for-profit and nonprofit providers.

SPEND AND SAVE

These products pair payment mechanisms with savings tools. They are usually bank accounts or general purpose reloadable prepaid cards, and are primarily intended to facilitate consumers’ transactions. Savings features are marketed as additional benefits to the account—sometimes referred to as “savings pockets” or “sidecars.” They are designed to enable consumers to easily—even automatically—build up a savings reserve while they carry out their day-to-day financial lives. Spend and save products are particularly promising tools to manage income volatility because they make savings the first available resource to cover cash shortfalls in the moment. Examples of these products include:

- Walmart’s MoneyCard – a general purpose, reloadable (GPR) prepaid card that offers a savings feature, the Vault. Drawing on research demonstrating that opportunities to win cash prizes boosts savings, MoneyCard users who move as little as $1 per month to their Vault are entered into a monthly prize drawing. Each month, Walmart awards 500 prizes, which are either $1,000 (1) or $25 (499).

- Digit – a fintech startup that automatically moves money into savings when it isn’t immediately needed. Unlike other apps that automatically move money to savings, consumers open an FDIC-insured bank account with Digit. The app makes decisions based on short-term liquidity constraints. As they put it, each day, “Digit checks your spending habits and moves money from your checking account if you can afford it.” Funds can be transferred back to the user’s checking account in one business day, and the company offers a guarantee against overdraft fees.

BORROW AND SAVE

These products combine credit and savings—and can therefore help households manage income volatility by expanding the resources available to them when they face shortfalls. Most are designed for and marketed to low- and moderate-income consumers who have limited access to credit and/or limited capacity to save. Many also enable consumers to build credit. Perhaps the best known type of borrow and save product is the secured credit card. Here, consumers are issued a low-balance card but must provide a security deposit equal to the card limit. Secured credit cards have been available for more than two decades, but have never fully gone mainstream. CFSI identifies several reasons, including low profitability due to high acquisition costs, and concludes that the product could be successful with substantial reforms to address those issues.

Recent borrow and save innovations are diverse. In a recent report, Commonwealth investigated the market for borrow and save products and identified several products across three categories: those that combine savings and credit to manage risk, those that offer credit products that also builds savings; and those that offer savings products that improve credit. Below are two examples of borrow and save products:

- Self Lender – a fintech startup whose slogan is “the most responsible way to build credit,” offers small loans (up to $2,200) that are not disbursed to borrowers but instead deposited into 12-month CDs. Borrowers pay off the loan in equal installments over 12 months. Upon repayment, borrowers gain access to both the CD’s principal and interest earned. Self Lender reports each payment to credit bureaus, so borrowers also build their credit histories and, often, their credit scores.

- Lending Circles – a nonprofit variant of credit builder loans. Lending Circles was developed by Mission Asset Fund, a Bay Area organization that supports low-income, primarily Latino residents. The program has since expanded to additional nonprofits nationwide. What makes Lending Circles unique is that the model is based on cultural practices familiar to consumers in the target market. Informal peer-to-peer lending is common in many countries, particularly those where large proportions of the population do not have access to formal financial services. In this model, a small group forms and commits to regularly contribute a set amount of money to a shared pool. Each month one member of the group receives the entire pool of money. Lending Circles formalizes that tradition by holding funds in bank accounts and reporting all participants’ payments to credit bureaus, helping them build credit histories and scores.

BUDGET AND SAVE

These products combine personal financial management tools and savings tools. Some customize users’ savings based on their budgets and available balances. Others enable users to identify budget and savings goals and work toward both simultaneously. These products can be helpful in managing income volatility because they analyze data on users’ income and expenses, reducing the burden on users and helping them anticipate and prepare for periods of volatility. Two examples of budget and save products are below:

- Even – smooths out users’ income for them. The app calculates average pay and ensures users receive that much money each payday. When earnings are higher than average, Even moves the excess funds to savings; when earnings are low, Even draws on the savings to make up the difference. When those savings are insufficient to cover the shortfall, Even provides a zero-interest loan to bridge the gap—which is automatically repaid the next time the consumers receives an aboveaverage paycheck. The app also identifies how much money users need to set aside for upcoming bill payments, and how much money remains available to spend.

- Earn and the Financial Clinic (FC) – both nonprofit organizations, have recently partnered to make expand the reach of their respective financial service offerings. Earn’s Starter Savings Program supports low- and moderate-income savers by contributing $10 in each month that users deposit at least $20 into their savings account. The Financial Clinic’s Change Machine platform offers curricula, coaching methods, and other resources to financial coaching organizations. Through this new partnership, financial coaching clients whose organizations use Change Machine can connect to Earn’s Starter Savings. Pairing these products may make it easier for clients to achieve their financial goals and save enough each month to receive the full match from Earn.

PAYROLL PLUS

These products to how people are paid and can help address income volatility by helping workers better align their income and expenses. Some do this directly, by enabling workers to access their pay before payday. Others layer additional services onto payroll systems, such as savings deductions and bill payments. These products are particularly promising for contract and contingent workers, who are usually unable to have taxes automatically deducted or contribute directly to savings from their paychecks. Innovative payroll products and services will be discussed in greater depth in a forthcoming EPIC brief. In the meantime, a few examples of these products include:

- DoubleNet Pay – enables workers to contribute directly to a goal-based savings account and pay bills automatically via payroll deduction. This addresses two challenges that arise from volatile incomes: automatically depositing part of a paycheck into savings increases workers’ ability to save successfully, and paying bills through payroll also leaves the worker with more certainty about how much money they have and how much is safe to spend. DoubleNet Pay partners with payroll processing firms and employers to make its services available to workers. When an employer decides to offer the service, DoubleNet Pay integrates into the rest of their payroll processes and procedures.

- WageGoal – designed in partnership by fintech startup FlexWage and the nonprofit Neighborhood Trust, aims to help financially insecure workers. FlexWage offers access to earned wages before payday, enabling workers to better match income with expenses and avoid liquidity crunches. Neighborhood Trust provides financial counseling, budgeting assistance, and high-quality financial wellness services to low- and moderate-income people, and is recognized as a leader in integrating nonprofit-developed services and private sector products to better meet consumers’ needs. WageGoal combines each organization’s offerings to help workers get more out of what they earn.

HOW INSTITUTIONS CAN HELP

Hybrid financial products are likely to continue growing rapidly over the next several years, due to changing consumer needs as well as deep interest from fintech startups and traditional financial institutions. There is a growing roster of fintech startups developing entirely new products with strong backing from investors, making it likely that consumers will soon have significantly more options. Additionally, there is growing interest from nonprofits with deep understanding of how financially insecure families manage volatility. This could be a winning combination: investors have the business savvy and funding to shape profitable mass-market products, while nonprofits have the expertise and consumer relationships to ensure that products offer effective solutions for target populations.

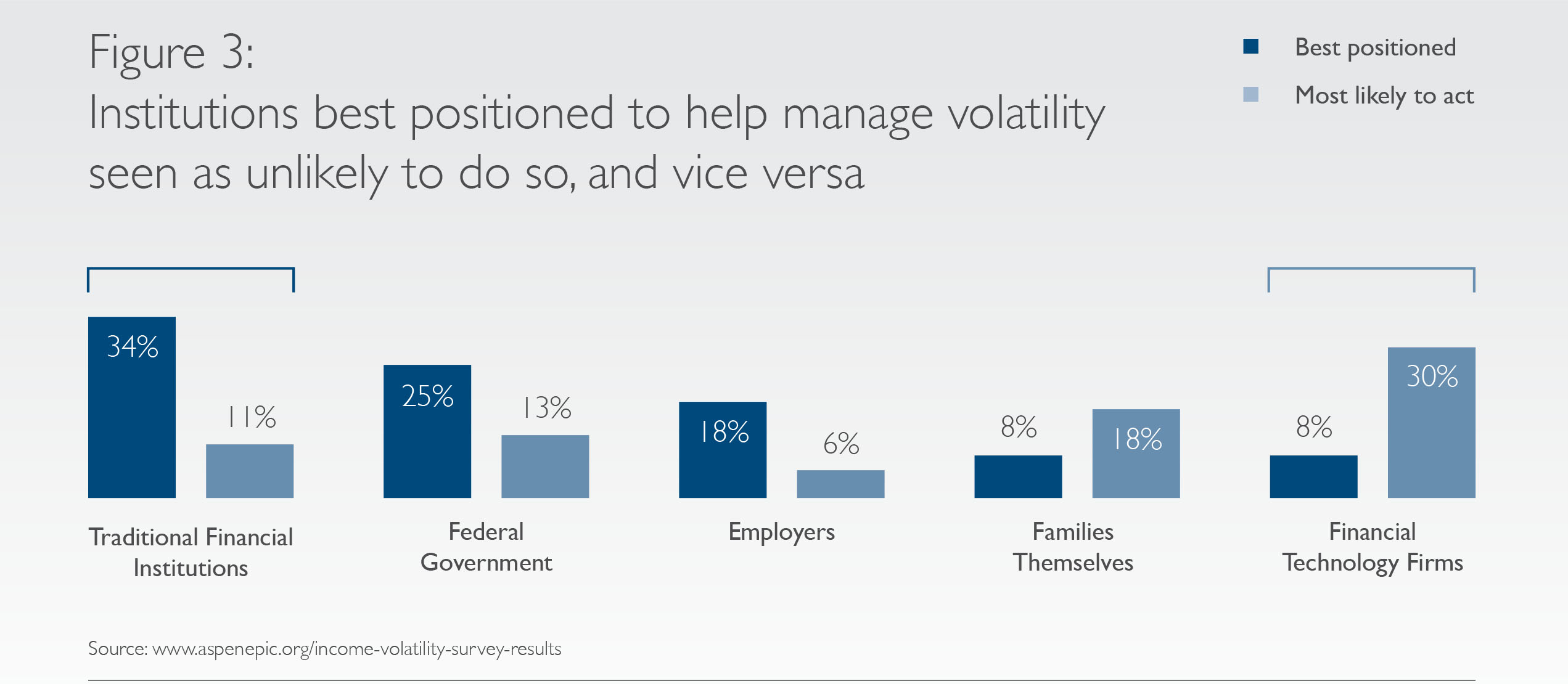

In our surveys, experts cited traditional financial institutions as the best-positioned to help families manage income volatility (43% of respondents), and fintech firms as the most likely to act (30%). They also identified employers and government as key institutions with the capacity to solve the problem. Each of those institutions can play an important role in supporting the development of high-quality, affordable hybrid products that help families manage income volatility.

FINANCIAL SERVICES INDUSTRY

Fintech startups and traditional institutions are pioneering the development of most hybrid products. As they move forward, they should continue to focus on solving consumers’ cash flow problems. Improving their ability to meet their expenses with available income is critical for reducing the negative impacts of volatility. Product designers should continue to apply behavioral insights about how consumers actually use products—and where actual use diverges from intended use—to ensure that hybrids truly are meeting consumer needs. Financial firms should also continue to forge cross-sector relationships with partners that have strong knowledge of how people experience and deal with income volatility. They should also work with regulators to build support and create space for innovation within the regulatory framework. These actions can ensure that hybrid products are well-designed to be affordable, safe, and effective.

EMPLOYERS

Employers have enormous power to help workers manage income volatility. They are able to see and understand how workers’ pay varies and can institute policies to directly reduce volatility. With regard to hybrid products, employers’ power lies in their ability to connect workers struggling with income volatility to products designed to help. Existing partnerships between employers and financial firms have incorporated hybrid products into business processes, such as payroll, and employee benefits programs. Continuing to form these partnerships and business relationships will support the refinement and scaling of hybrid products while doing more to meet their employees’ needs.

GOVERNMENT

The regulatory landscape is one of the most important considerations that will influence the growth and direction of these products, and it is both promising and challenging. Many of the products that hybrids combine are regulated quite differently. Savings and credit, for example, are subject to separate federal regulations. States take very different approaches to regulating financial firms, too. Bank- and credit union-issued products may face higher barriers to entry because they face different, scrutiny from regulators than fintech firms. One important opportunity is federal regulators’ emerging interest in supporting financial innovation. The CFPB’s Project Catalyst, for instance, is a dedicated office within the Bureau that is responsible for working with financial institutions developing innovative products. The office provides advice and feedback, can issue “no action” letters that may provide relief from other regulators’ concerns, and offers opportunities to pilot new products and services in partnership with the Bureau. Moreover, in 2016, the Office of the Comptroller of the Currency (OCC) announced that it has plans to consider applications from fintech firms to receive special purpose national charters. The agency also created an Office of Innovation with similar responsibilities to Project Catalyst.

Government agencies must continue to balance consumer protection and innovation. Efforts like Project Catalyst that strengthen relationships with innovators are key, as they help firms and regulators understand each other’s perspectives, needs, and concerns. Agencies should ask not only ask whether a hybrid product is safe for consumers, but also how effectively it can solve their problems. Perhaps the most important role of government is to develop a framework for supervising and regulating products whose multiple functions face particularly complex, overlapping, or contradictory regulations, such as savings and credit or insurance.

PRINCIPLES FOR FUTURE ACTION

The hybrid products described throughout this brief share a few common themes that enable them to help families manage income volatility. First, they leverage technology to carry out complex analysis in nearly real time, with a level of detail and accuracy that is difficult for humans to match. Second, they help users optimize the use of their existing financial resources. Third, they automate behaviors that are difficult (saving, keeping track of cash flow) and integrate them into products that are easy and/or necessary for consumers to use (debit and prepaid cards, payroll systems). These elements have the potential to powerfully improve families’ capacity to manage income volatility and thus strengthening their financial security.

We have identified several other design principles that could make hybrid products even more promising for addressing income volatility:

-

- Put user experience and consumer behavior at the center of the design process

- View credit and savings as complementary and help consumers access both based on what is most appropriate for their current financial position and needs 9

- Make customizable tools for budgeting and cash flow management core product functions

- Risk-management tools (potentially including insurance) to protect consumers against shocks larger than available credit and savings

As financial innovators, employers, and governments move forward, there is some risk that new products will have adverse, unintended consequences. As they continue to develop and support solutions that help households manage income volatility, these features can serve as a guide to ensure that products are safe, affordable, and effective.

For Endnotes and Works Cited, as well as more information on FSP and EPIC, please download the PDF version of this Issue Brief.

● Acknowledgments

EPIC would like to thank Katherine Lucas McKay for writing this brief; Kiese Hansen, Gracie Lynne, David Mitchell, Ida Rademacher, and Joanna Smith-Ramani for reviewing drafts and making invaluable suggestions; Pamela Chan, Brian Cosgray, Arlyn Davich, Frank Dombroski, Timothy Flacke, Fiona Greig, Dan Kaiser, Callum King, Tim Lucas, and Dan Quan for the time and wisdom they shared on the topic; Katie Bryan for laying out the brief; and Laura Starita at Sona Partners for designing the template. EPIC would also like to thank all those who completed the expert surveys or participated in either of the EPIC convenings. While this document draws on insights shared at these EPIC forums and by the aforementioned individuals, the findings, interpretations, and conclusions expressed in this report – as well as any errors – are EPIC’s alone and do not necessarily represent the view of EPIC’s funders or Advisory Group members. Finally, EPIC thanks the Citi Foundation, the Ford Foundation, JPMorgan Chase, and the W.K. Kellogg Foundation for their generous support.

● More Resources on the Connection Between Financial Solutions, FinTech, and Income Volatility

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved