The Issues | What We Know | July 2017

●●●●

● Summary

The Expanding Prosperity Impact Collaborative (EPIC), an initiative of the Aspen Institute’s Financial Security Program, is a first-of-its-kind, cross-sector effort to shine a light on economic forces that severely impact the financial security of millions of Americans, one issue at a time. Over the past 18 months, EPIC has synthesized data, polled consumers, surveyed experts, published reports, and convened leaders, all to build a more accurate understanding of how income volatility impacts low- and moderate-income families and how best to combat the most destabilizing dimensions of the problem. But many questions remain. If income volatility is growing, for whom? What is driving the trend? Who is most affected? What is the impact on families? Importantly, how is this persistent and destabilizing trend disrupting and paralyzing other efforts to improve the economic opportunity and wealth-building of families? And, naturally, what are the kinds of solutions that can match the size of this challenge?

This new EPIC research brief by Daniel Schneider (UC Berkeley) and Kristen Harknett (University of Pennsylvania) enhances our understanding of the connections between income swings and family outcomes for hourly retail workers. These workers are vulnerable to income shocks because they earn low wages, have changing, often unpredictable schedules, and are paid hourly. Many experience severe degrees of income volatility on a week-to-week basis, driven partly by unpredictable and unstable scheduling. The brief presents results from the Retail Work and Family Life survey, a national survey of service sector workers. The quantitative analysis is complemented with vignettes drawn from 25 in-depth interviews with San Francisco Bay-area parents working in retail or food service.

Some of the key findings:

- Income swings are common and sizeable among hourly workers: In a survey of 6,000 hourly non-managerial workers employed at 30 of the largest retail and fast-food companies, half report that their income varies from week to week. In the month prior to completing the survey, a typical respondent experienced a 34% difference between the lowest and highest earning weeks.

- Unpredictable schedules are a significant driver of income volatility: 54% of workers with variable schedules report week-to-week income volatility, compared to 40% of those with a regular day schedule.

- Volatility is connected to financial insecurity: Workers who report week-to-week volatility are 20% more likely to experience financial hardship; those with high levels of volatility were 12% more likely to have trouble paying bills. Additionally, workers who reported higher volatility were less likely to feel confident about their ability to cope with hypothetical shocks and more likely to turn to high-cost alternative financial services than those with steady earnings.

Solving for income volatility means reducing it where possible and helping families manage when they experience volatility. Governments at all levels, employers, the financial service industry, and, of course, the nonprofit sector have the capacity to advance a diverse range of potential solutions, and all their efforts are needed. The EPIC process has identified six solution areas that show promise to reducing the incidence of income volatility and the negative consequences described in this paper: predictable scheduling, short-fall savings, hybrid financial products, payroll innovations, unemployment insurance, and wage insurance. Each solution is described in more detail – including the role for the private and public sector – in a series of briefs available through the EPIC website.

● Issue Brief

INTRODUCTION

Tonya, a mother of three and employee at a big box store, is never sure how much she is going to earn from one week to the next. Although she is paid a fixed hourly wage, the number of hours she will work in any given week is unpredictable and outside of her control. As Tonya describes, “I get $10 per hour, you know, my hours vary. Sometimes I work 8 hours, sometimes I work part-time hours…next week I’m only working two days…but then the week right after that I’m working Monday through Friday, you know, [the hours] go up and down and so does the amount.”

Tonya’s story is documented in a new study, the Retail Work and Family Life Study, which includes a national survey of over 6,000 service sector workers and in-depth interviews with 25 working parents in the San Francisco Bay Area. This paper describes some of the key findings from this study on the pervasive experience of income volatility among those employed in the service sector as well as widespread consequences of this income volatility for household economic stability.

By nearly all accounts, income volatility is quite high and has been rising over the past several decades (Dynan et al. 2012; Gottschalk and Moffitt 2009). Income volatility is experienced across the income spectrum but is particularly common and impactful for low-income households. Workers in the service sector are particularly vulnerable to unstable income, because jobs in the service sector are usually paid by the hour and are often characterized by unpredictable and unstable work hours. Service sector workers are also particularly vulnerable to hardship when income fluctuates, because making ends meet on low wages makes it difficult to accrue savings and smooth income. The new data from the Retail Work and Family Life Study advances our understanding of the contours, causes, and consequences of income volatility for the large and growing number of workers employed in the service sector. We draw on this data to describe week-to-week volatility in earnings and in household income, to show how unstable and unpredictable scheduling practices drive income volatility, and to examine how income volatility matters for household economic security.

The portrait that emerges shows that work hour and income instability upset the delicate balance of income and expenses for low-income households and lead to a range of harmful consequences. There is a pressing need, then, for solutions that reduce work schedule instability and that help families to weather this instability when it does occur.

Recent research shows that volatility in labor market earnings is a large component of overall income volatility, and that a major driver of volatility in earnings is irregular work hours.

BACKGROUND

CONTOURS OF INCOME VOLATILITY

Recent research charts volatility in income and earnings between years and shows that income volatility from year to year is both prevalent and on the rise (Dynan et al. 2012; Gottschalk and Moffitt 2009). This important insight on annual income volatility has sparked further explorations into the extent of income fluctuations from month-to-month. In fact, month-to-month income volatility is also quite high: According to recent data from the Survey of Household Economics and Decisionmaking (SHED), one-third of all U.S. households report that their income varies from month-to-month (Federal Reserve 2016). High rates of month-to-month income volatility are also found in analyses of data from the financial diaries (Morduch and Schneider 2014; Hannagan and Morduch 2015) and in big data analyses of one million Chase banking customers (Farrell and Grieg 2016). These multiple data sources and studies reveal then that fluctuations in income from month-to-month are common and are sizeable.

The more granular data on monthly income variation is valuable because many large household expenses, such as rent or utilities, are paid on a monthly basis. However, these broad portraits of monthly income fluctuations are limited in two respects. First, these descriptions combine high income households with the resources to smooth their incomes over time with low-income households that lack those resources. There is a need for closer examination of income dynamics for low-income families in particular. Second, these descriptions still elide even more granular income fluctuations from week-to-week. This more fine-grained analysis of week to week volatility is usually not possible with existing data sources. Understanding week-to-week income volatility is important for low-income households because these week-to-week fluctuations can affect a household’s ability to afford basic daily necessities such as food as well as keep up with other regular household expenses.

CAUSES OF INCOME VOLATILITY

What causes volatility in income and earnings? Volatility is created both by dips and spikes. Workers who receive year-end bonuses, overtime pay, or raises will experience volatility in earnings between years and even between months. But, so will those who see their work hours reduced, who experience a period of unemployment, or take unpaid leave.

Recent research shows that volatility in labor market earnings is a large component of overall income volatility, and that a major driver of volatility in earnings is irregular work hours (Farrell and Grieg 2016; Federal Reserve 2016). Employment in the United States has become more “precarious” over the past fifty years. This precarity is manifest in low wages, few fringe benefits, and of key interest here, irregular and unpredictable work schedules. Particularly in the service sector, workers can no longer count on a regular day shift, or even a regular night or evening shift. Instead, work schedules are often set by employers on short-notice and the hours assigned to workers vary from day-to-day and the days worked vary from week-to-week (Lambert 2008). These practices, primarily affecting low-wage workers are likely to direct translate into earnings and income volatility – not just between years, or between months, but on a week-to-week basis.

The hourly pay and fluctuating hours in low-wage employment help explain why prior research has shown that income volatility is most pronounced among the households in the bottom income quintile. In the bottom quintile, 74 percent of households experienced income fluctuations of 30 percent or more from month-to-month (Farrell and Grieg 2016). Further, recent research from the SHED suggests that unpredictable and unstable work scheduling practices may play an important role in household income volatility dynamics. Of the one-third of respondents who reported that their household income varies from month-to-month, the single most common reason cited for this volatility was an “irregular work schedule.”

However, the SHED does not contain other detailed measures of work scheduling practices that would allow us to further examine this potentially important relationship and map these scheduling practices onto finer-grained measures of volatility. The new data we present extends and fleshes out this useful research by delving more deeply into work schedules, income volatility, and household financial security in the service sector.

CONSEQUENCES OF INCOME VOLATILITY

We saw that income volatility is particularly common for low-income households. The consequences of income volatility are also most pronounced for low-income households, which often have few economic resources to buffer income shocks (Hannagan and Morduch, 2015). Income fluctuations also pose the largest challenge when they are unpredictable and outside of an individual’s control. All of these conditions – few resources, unpredictable work schedules, and low autonomy – typify work in the service sector.

While a substantial amount of research describes levels and trends in volatility and begins to identify the causes of volatility, there is much less known about the consequences of income volatility for household wellbeing (Aspen Institute, 2016). Previous research finds that income volatility has consequences for household economic security, food insecurity, and economic hardship (Bania and Leete, 2007; Federal Reserve, 2016). Research also suggests that income volatility is linked to adverse schooling outcomes for children and worse emotional health among adults (Gennetian et al, 2015; Yeung et al, 2002; Hardy, 2014; Prause et al, 2009). However, in general the literature on the effects of income volatility remains quite thin.

THE DATA

The ongoing Retail Work and Family Life Study has collected national survey data from service sector workers and in-depth qualitative data from parents working retail jobs in the Bay Area.

The survey data were collected in 2016 from approximately 6,000 hourly non-managerial workers employed at 30 of the largest retail and fast-food companies by revenue. The survey is unique in combining detailed data on work scheduling practices, novel measures of income volatility, and a robust set of indicators of household economic security.

We harness these survey data to document the extent of week-to-week fluctuations in earnings and in household income, and to examine which demographic groups experience the most volatility. We then focus on unstable and unpredictable work scheduling practices as a likely significant determinant of earnings and income volatility. Finally, we use our survey data to trace the consequences of week-to-week income and earnings volatility for household economic security.

We complement this quantitative analysis with vignettes drawn from in-depth interviews conducted with parents working retail and food service jobs in the San Francisco Bay Area between June of 2015 and August of 2016. These interviews explored family dynamics related to schedule instability and unpredictability and income volatility. Interviews were taped, transcribed, and coded.

THE HIGH PREVALENCE OF WEEK-TO-WEEK EARNINGS AND INCOME VOLATILITY IN THE SERVICE SECTOR

When hourly, service sector workers experience a change in their hours worked from week to week, they also experience a proportionate change in their earned income. In our study, we capture this earnings volatility by comparing the week when the worker earned the least with the week they earned the most over the past month. Our measure of earnings volatility is the percent difference in highest and lowest weekly earnings in the past month.

Earnings in the service sector are highly volatile. The typical service sector worker experiences a 34% fluctuation in weekly earnings between the lowest and highest earning week in the month prior to completing our survey. More concretely, the typical worker earned as little as $214 and as much as $351 per week over the past month – a substantial amount of week-to-week volatility. These fluctuations can create severe hardships. Few service sector workers are making more than the bare minimum they need to make ends meet, even in the week they work the most hours. Therefore, a typical worker who is counting on making $351 each week can expect to face a shortfall of $137 once a month.

Compared with the typical service sector worker, some service sector workers have more stable earnings and some have even more volatile earnings. The workers who were in the top quartile in terms of earnings stability experienced less than a 20% swing in their earnings from week-to-week. In contrast, the workers who were in the quartile with the least earnings stability experienced at least a 54% swing in earnings from week-to-week. Across the board, though, earnings volatility is nearly universal in the service sector. Just 4% of workers reported less than a 5% change in earnings from week-to-week.

Because earned income is not the only income source for service sector workers, we also examine a second, broader measure of household income volatility, which captures fluctuations in income from all sources. To measure household income volatility, we asked workers to report whether “week-to-week your household income is” either “basically the same” or “goes up and down.” Because earned income is a major component of overall household income volatility, these two measures of volatility are closely related, and workers with highly volatile earnings are at high risk of a having a volatile household income as well. There is a striking degree of volatility in respondents’ household income: Half of all respondents report that week-to-week, their household income goes up and down.

Box 1: Earnings vs Income Volatility

Volatility for Whom?

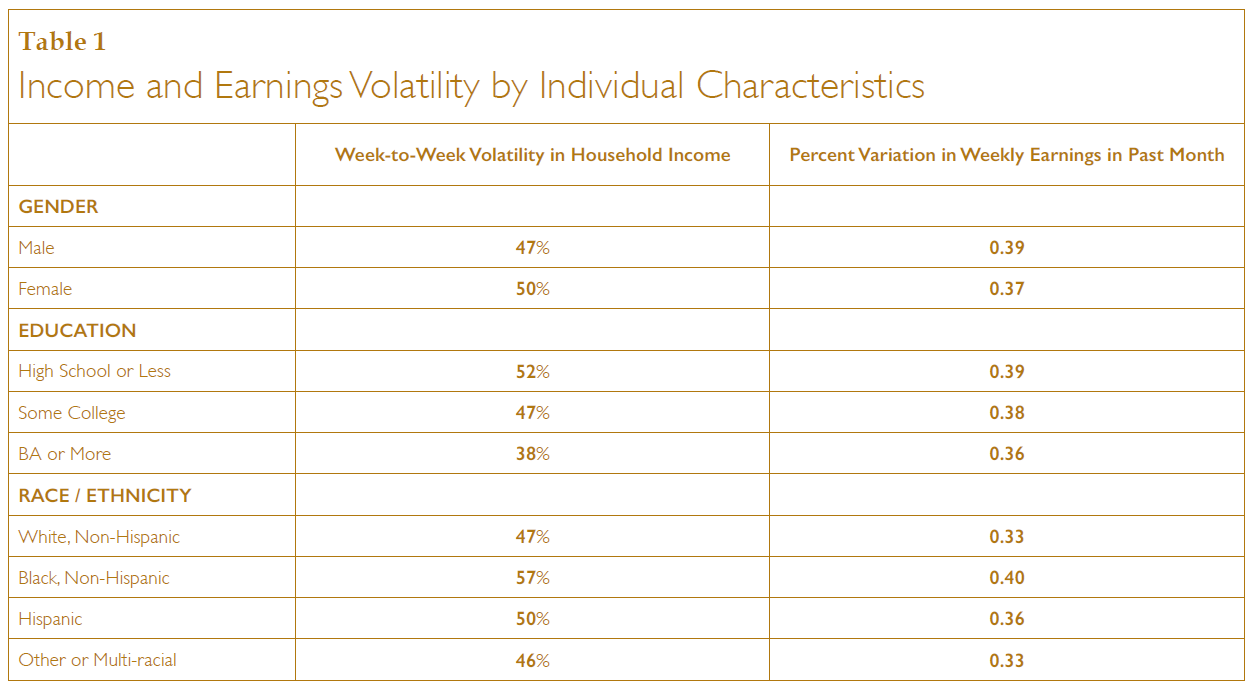

Some earnings and income volatility is experienced by nearly all service sector workers but this volatility is not evenly distributed across workers. There is a very clear difference in the degree of volatility depending on level of educational attainment, with higher levels of educational attainment having a stabilizing influence. Among our sample of service sector workers, 52% of workers with a high-school degree or less report week-to-week variation in household income compared with 38% of those with a college degree. Although not as large as these educational differences, we also observe racial disparities in the experience of income volatility: 57% of African American (non-Hispanic) respondents report week-to-week household income volatility compared with 50% of Hispanic respondents, and 47% of white, non-Hispanic workers. Women experienced slightly more volatility than men. Table 1 presents these statistics as well as similar patterns in week-to-week volatility in earnings by these demographic characteristics.

WORK SCHEDULES AS A DRIVING FORCE BEHIND INCOME VOLATILITY

Many factors can contribute to week-to-week variation in income and earnings, but work schedules are a key driving force. Workers certainly can experience dips and spikes in income for other reasons such as job churning, raises or bonuses, and overtime pay, but the income volatility that stems from work hours that change from week-to-week is distinctive in being a source of routine and chronic income volatility that workers contend with week in and week out, rather than just once in a while. In short, workers with unstable schedules are subject to a kind of “routine unpredictability” in their income and earnings, similar to that described previously for those employed in the health care industry (Clawson and Gerstel 2015).

In-depth interviews with retail workers in the Bay Area revealed a strong link between unstable work schedules and earnings volatility.

Patricia, a single mother who is employed at a big box store described the routine ups and downs in her scheduled work hours. As she says, “I could be anywhere from literally four to 20 hours a week.” In the lighter weeks, Patricia tries to supplement her income with odd jobs. For Patricia and most service sector workers, the volatility in work hours is largely outside of their control, and is determined for the most part by the needs and directives of employers.

Maria, a mother with four children who was employed at a grocery store, also experienced routine work hour instability. Maria described her weekly schedule from the past month week by week, then summed up: “you never know if you’re gonna work 40 hours or 24 hours…”

Maria expressed a willingness to work night or day and kept her schedule open and available to pick up extra shifts on short notice, because she was desperate for more hours and income. She continued, “it’s been hard because, like I said, they change my hours every week …. there is no guarantee that they have to give me my 32 hours. …there’s no guarantee. And they can give me like this week coming up they gave me 40 hours. But I don’t know what is gonna be like my next week so this 40 hours I’m oh okay, I have a little bit more extra money there but that’s for guarantee me for next week. It probably gonna go down to 24 hours so that money that I received the week before I have to save something, because I don’t know what’s gonna happen the next week.”

Given the low wages and scarce resources typical among service sector workers, the vast majority of working parents in our study were unable to save and had expenses that required full-time work hours every week, not just once in a while.

This uncertainty and fluctuation in the number of scheduled work hours was typical of the working parents we interviewed. Involuntary part-time work was a near universal complaint. The income smoothing that Maria describes – saving some money from a week she worked 40 hours to cover the week she could work only 24 hours – would be a good coping strategy. However, given the low wages and scarce resources typical among service sector workers, the vast majority of working parents in our study were unable to save and had expenses that required full-time work hours every week, not just once in a while.

From our national survey, we find corroborating evidence that week-to-week income and earnings volatility is often driven by scheduling instability and unpredictability. Schedule instability and unpredictability is multifaceted and requires multiple measures to get a complete picture. From our national survey, we characterize work schedules along four dimensions:

1) Schedule type: We asked our survey respondents to characterize their work schedules as either being regular day, regular night, regular evening or being a variable schedule or a rotating schedule.

2) Advance notice: Respondents report on the amount of advance notice that they have of their work schedules – that is how far in advance they generally know when and how much they will work (categorized as less than a week, 1-2 weeks, 2-3 weeks, or 3 weeks or more).

3) On-call shifts: Respondents report the frequency with which they were required to be “on-call” for work shifts in the prior month. “On Call” shifts mean that employees must be available for a work shift if called, but may also not be called-in.

4) Cancelled shifts: Finally, we asked respondents to report on whether one of their work shifts had ever been scheduled but cancelled in the prior month.

The conditions of low-wage work in the service sector vary such that some workers experience stability in their schedules, others experience a great deal of instability, and many fall in between the extremes. We count up the number of types of schedule instability that a worker experiences to create an “Instability Scale.” On this scale, 1 out of 10 service sector workers enjoy a regular and predictable schedule with 0 types of instability. The large majority of workers – 7 out of 10 - fall in the middle of the instability scale, encountering 1 or 2 types of instability. At the high end of the continuum, 2 out of 10 service sector workers experience 3 or 4 types of schedule instability.

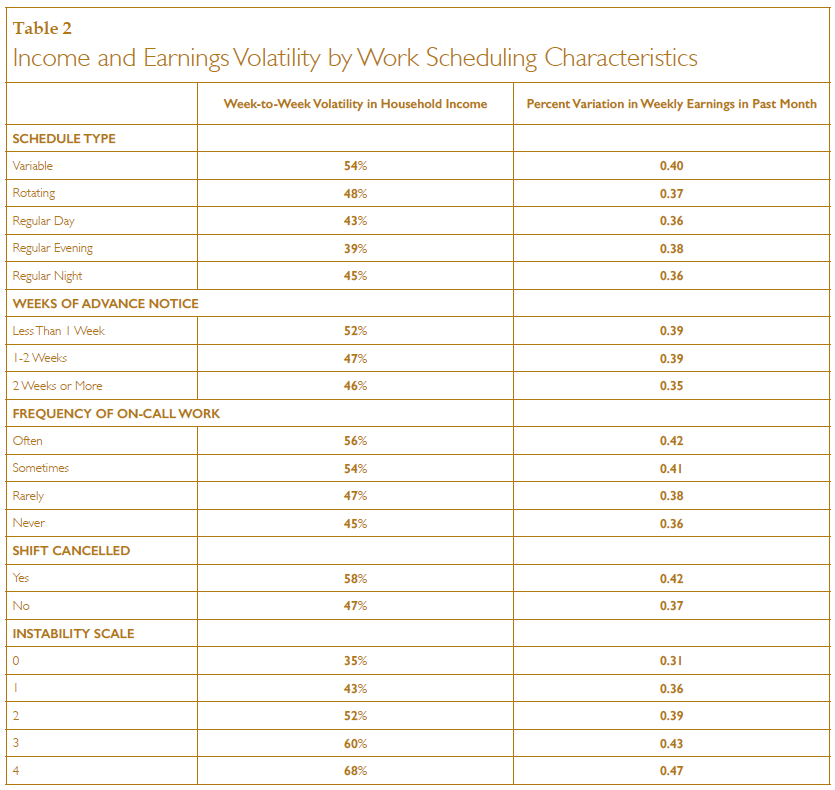

We examine the extent to which these four measures of exposure to unstable and unpredictable work scheduling practices are associated with week-to-week volatility in earnings and in household income. Table 2 isolates the relationship between these scheduling practices and earnings and income volatility by statistically controlling for a rich set of demographic and economic characteristics.

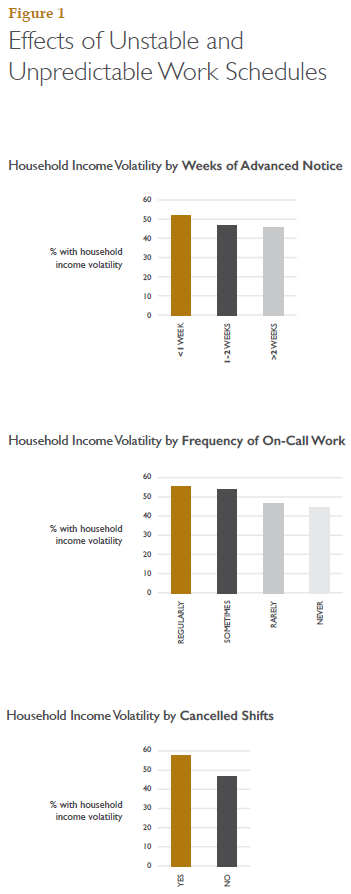

Our national data show that unstable and unpredictable work schedules are indeed associated with week-to-week volatility in household income. We estimate 54% of workers who have a variable schedule report that their household income changes from week-to-week, compared with just 43% of workers who have a regular day schedule. Those who work a regular night shift or evening shift also report lower levels of income volatility than those who work a variable schedule. Notably, while workers with a rotating shift experience variation in hours, in theory that variation is predictable and these workers experience less volatility than those with variable shifts. Workers who receive more advance notice of their work schedules also report lower levels of income volatility – 52% of those with less than one weeks’ notice versus 46% of those with at least two weeks’ notice. Workers exposed to on-call work and to cancelled shifts are also significantly more likely to report household income volatility. Consistent with these results on volatility in overall household income, we see a similar set of relationships between work schedules and volatility in earned income.

There is a very strong relationship between the extent of exposure to unpredictable and unstable scheduling and our two measures of volatility. Among workers with the most schedule instability, 68% experience income volatility. In contrast, among workers with the most stable schedules, just 35% report week-to-week variation in household income. Schedule instability has a powerful influence on the experience of income volatility.

It is important to note that, while these scheduling practices are significantly related to volatility in our data, we also see high levels of income and earnings volatility among service sector workers who have stable and predictable schedules. This volatility could come about because other earners contributing to household income experience volatility, because of volatility in income from second jobs or odd jobs, or because of ups and downs in the receipt of child support, public benefits, or informal support. Although work schedules are an important input influencing income volatility, there are clearly other factors at work.

6. Consequences of Volatility

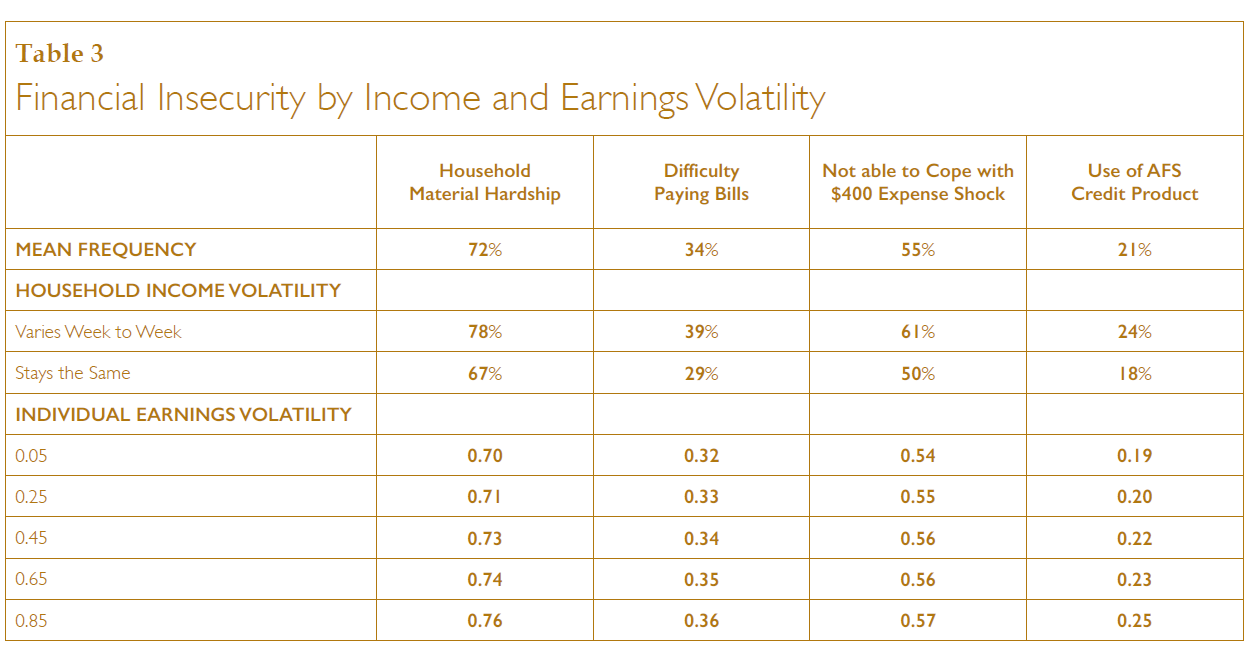

Week-to-week volatility of income and earnings is widespread among hourly service sector workers and is significantly shaped by work scheduling practices. What are the consequences of this income volatility for household economic security? To address this question, we analyze our national data, isolating the effect of income and earnings volatility on household economic security after statistically controlling for a large set of demographic and economic controls. The results are presented in Table 3.

Income volatility increases the experience of material hardship over the past year. Such experience of material hardship is widespread in this sample of the working poor. But, the experience differs significantly by volatility. Respondents who report that their household income varies from week-to-week are more likely to experience material hardship (78%) than those whose income is steady (67%). The chance of experiencing material hardship also rises in tandem with increases in weekly earnings volatility.

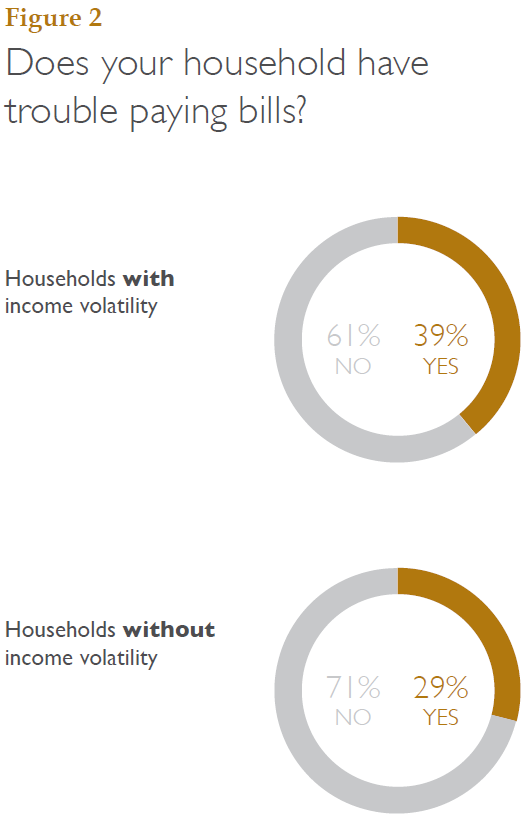

Respondents dealing with income and earnings volatility are also substantially more likely to report difficulty paying bills and making ends meet. 39% of workers who report week-to-week variation in household income had trouble versus 29% of those with more stable incomes. Earnings volatility was also a significant predictor of difficulty paying bills.

In our in-depth interviews, several respondents reported that fluctuating work hours led to trouble paying their rent and other monthly bills. One working father, employed at a fast food restaurant, described the hard choices that had to be made when his earnings dipped, “if I need to buy [something], I need to think like five times if we need it.”

Another respondent, a working mother, described the very real consequences of income volatility stemming from variable hours, explaining “It just depends on my schedule. Sometimes I wont get 35 I’ll get 32. You know and those 3 or 4 hours...matter. It's a big difference! That's $50 for food and I actually um... If I run out of food or something I can go to my church and get food box from them. I can only do it like once a month, but I can do that if I run low. And I have utilized that.” For this mother, there is a clear line connecting instability in work hours, to volatility in earnings, to household food insecurity.

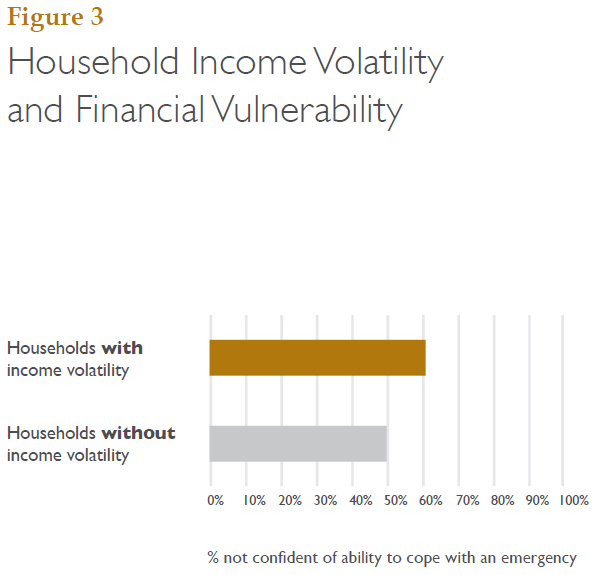

Volatility seems to also shape a more general financial vulnerability. Workers who report volatile household incomes also reported being less confident of their capacity to cope with a hypothetical $400 expense shock: 61% of those who experienced volatility reported being uncertain about their ability to cope against 50% of those who had stable household income. We did not though find significant variation in confidence in ability to cope with an expense shock by the degree of earnings volatility.

In the face of regular expenses, income and earnings volatility present households with the need to somehow smooth consumption. One way households may do so is through the use of alternative financial services (AFS) loan products such as payday loans or pawnshops. We find that 24% of respondents who report week-to-week volatility in income report using a payday loan or pawn shop in the past 12 months against 18% of those with stable incomes week-to-week. We also find a significant gradient in AFS loan product use by earnings volatility with just 19% of those with the most stable earnings reporting use a payday loan or pawnshop against 25% of those whose earnings were most variable.

CONCLUSIONS

We find widespread income and earnings volatility among service sector workers. This volatility plays out on a weekly basis and we find that exposure to unstable and unpredictable scheduling is a significant determinant of this volatility. Moreover, workers who experience week-to-week volatility in their incomes and earnings are more financially insecure. They are more likely to have experienced serious material hardships over the prior year, more likely to have difficulty paying bills, and less likely to feel confident in their ability to cope with a moderate expense shock. These workers are more likely to turn to alternative financial services like payday loans and pawning.

Our work suggests that recent policy and corporate action to reduce the use of unstable and unpredictable work scheduling practices could meaningfully reduce income and earnings volatility. Policy action on scheduling has been led by several west-coast cities, with San Francisco passing the first legislation to regulate unpredictable scheduling in 2014 and then with Emeryville, CA and Seattle, WA following suit in late 2016. All of these ordinances aim to reduce the unpredictability, and so perhaps also the variability, of work schedules by requiring large companies in the service sector to provide two weeks of advanced notice and to provide “predictability pay” when schedules change within two weeks of the shift. Because of the strong evidence linking schedule instability to income volatility, recent local ordinances that improve schedule instability can be expected to reduce income volatility at the same time. Alongside these legislative changes, some companies are also beginning to change their scheduling practices, with Walmart announcing that it will offer all Associates the opportunity to work a regular fixed schedule. These changes seem likely to be important, if partial, solutions to the problem of income and earnings volatility.

Our results also show that workers who experience income and earnings volatility are more likely to turn to alternative financial service providers like payday lenders and pawn brokers, presumably to smooth consumption in the face of volatile incomes. Solutions that could provide lower cost ways to satisfy this financial function could also be valuable. In this domain, FinTech innovations such as Even, Digit, and Active Hours that help workers smooth erratic incomes, may mitigate some of the harms of volatility.

When assessing the financial well-being of America’s working families, this paper adds to a growing chorus calling for attention not just to the level of annual income but also to the stability and volatility in income streams. The Retail Work and Family Life study shows that income volatility is prevalent and consequential for working families in the service sector, and that work schedules play an important role in driving this income volatility, and therefore represent an important avenue for crafting solutions.

For Endnotes and Works Cited, please download the PDF version of this Issue Brief:

● Acknowledgments

EPIC would like to thank Kristen Harknett and Daniel Schneider for writing this brief; Katherine Lucas McKay, David Mitchell, and Joanna Smith-Ramani for reviewing drafts and making suggestions. Schneider and Harknett gratefully acknowledge grant support from the Washington Center for Equitable Growth, UC Berkeley’s Institute for Research on Labor and Employment, the UC Berkeley School of Public Health, and the Hellman Fellows Fund. EPIC would also like to thank all those who completed the expert surveys or participated in EPIC’s many income volatility-focused convenings—that process deeply informed our series of briefs on promising solutions, as well as identifying important new research on the causes and consequences of income volatility, such as the Retail Work and Family Life survey.

Finally, EPIC thanks the Ford Foundation, Prudential, and the W.K. Kellogg Foundation for their generous support of our work. The findings, interpretations, and conclusions expressed in this report – as well as any errors – are EPIC’s and the authors’ alone and do not necessarily represent the view of EPIC’s funders or Advisory Group members.

● More Resources on Scheduling and Income Volatility

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved