The Issues | What We Know | July 2017

●●●●

WAGE INSURANCE

● Summary

Research on income volatility reveals that job loss is one of the top two sources of negative income shocks. Yet, many efforts to understand and address income volatility do not adequately address the unique consequences of job loss. Newly unemployed workers face not only the short-term financial distress associated with dips in income, but also a long-term reduction in earnings, leaving them with fewer resources to manage income volatility in the future. In recent decades, laid-off workers do not reach their previous level of earnings for as long as six years. Even once reemployed, these workers face the type of ongoing, short-term volatility that impacts nearly half of all households—but future income spikes are likely to be smaller in magnitude. To explore these specific challenges, EPIC is focusing two briefs in our series on promising solutions to income volatility that is caused by job loss: this brief on wage insurance and a forthcoming brief on unemployment insurance. These briefs focus on public policies that can make these social insurance schemes work well for families, as well as explore private sector opportunities to complement and leverage public programs.

This brief focuses on wage insurance, a potentially high-impact opportunity to help families avoid the serious long-term consequences of job loss or reduced wages. Wage insurance is an insurance policy that provides partial replacement of lost wages to workers who are forced to accept pay cuts. The brief reviews the current research on how income shocks associated with job displacement impact families’ financial security in the short- and long-term. It reviews prior efforts to implement various forms of wage insurance, discusses the roles of key institutions – governments, employers, and financial services providers including insurers—and recommends principles for further action.

● Issue Brief

WHAT HAPPENS WHEN DIPS IN INCOME ARE NEVER OFFSET BY COMPENSATING SPIKES?

Income volatility destabilizes the finances of nearly half of American families each year. The problem has become both more common and more intense in recent decades. The share of households experiencing a negative income shock of $20,000 per year or more, for example, rose by 23% from 1991-2004. The Pew Charitable Trusts recently found that 43% of families experienced swings in income of more than 25% over a two-year period. Among those who experience income volatility, the second most common reason (following irregular work schedules) is unemployment.

The Pew Charitable Trusts define a “sudden income shock” as a year-over-year change of more than 25%, and find that 15% of households experience a negative shock each year. Families that experience these severe income shocks report lower financial wellbeing than others. What makes spells of unemployment so insidious is that workers rarely see countervailing spikes in income after a job loss. In fact, displaced workers often face wage reductions when they return to work. One recent study found that when a laid-off worker found a new position, he or she was paid, on average, about 33% less than in their previous job. The researchers followed a sample of workers for six years, and found that average earnings were still 7%-9% below baseline at the end of the study.

There are important differences in how different causes of volatility manifest and impact workers’ financial security. Volatility caused by irregular work schedules manifests as regularly occurring but difficult to predict, short-term fluctuations in income.

On the other hand, job loss causes large, sudden dips in income that are never fully offset by future spikes. Without a chance to catch up, money challenges during unemployment can turn into long-term financial distress.

This often leads to indefinite or semi-permanent drops in living standards.

Predictable scheduling and income-smoothing tools are not sufficient solutions for workers who have no income or whose earnings remain depressed and do not spike back up. For this population, solutions to income volatility must not only help smooth income but also provide ongoing support as workers climb back up the income ladder. Wage insurance programs and products can provide exactly that type of support.

INSURANCE CAN HELP, BUT EXISTING PROGRAMS ARE INSUFFICIENT TO ADDRESS THE PROBLEM:

Insurance is one of the most effective ways to hedge against financial risks. In the private sector, insurance is available to protect consumers against the risks of costly medical care, car accidents, theft, floods and fires, early death, and outliving one’s savings. In the public sector, social insurance programs protect certain groups of individuals, primarily workers (unemployment insurance, workers compensation), poor families (Medicaid) and the elderly (Medicare and Social Security). Innovative approaches to insurance—public and private—can be important tools to reduce volatility and mitigate the negative consequences of negative income shocks.

There are already two federal insurance programs that address and reduce income volatility associated with job displacement. The federal Unemployment Insurance (UI) program provides financial support to workers who have lost their jobs and are now searching for new positions—and is the subject of a future brief in this series. There is also an existing wage insurance program, Alternative Trade Adjustment Assistance (ATAA), which serves workers who have been displaced due to industrial decline and import competition—this is described in depth in the next section of this brief. Unfortunately, neither program is sufficient to address the prevalence or long-term consequences of income shocks due to job loss.

UI is designed to replace a substantial portion of lost income while encouraging workers to find new jobs quickly. For those reasons, benefits are generally limited to 26 weeks (or less in some states). The program also includes measures designed to exclude workers who were not strongly attached to the labor force, such as limiting eligibility to full-time, permanent workers and those who meet job tenure requirements (these vary by state and can be as long as one year). These restrictions help control costs but are poorly designed for today’s labor market.

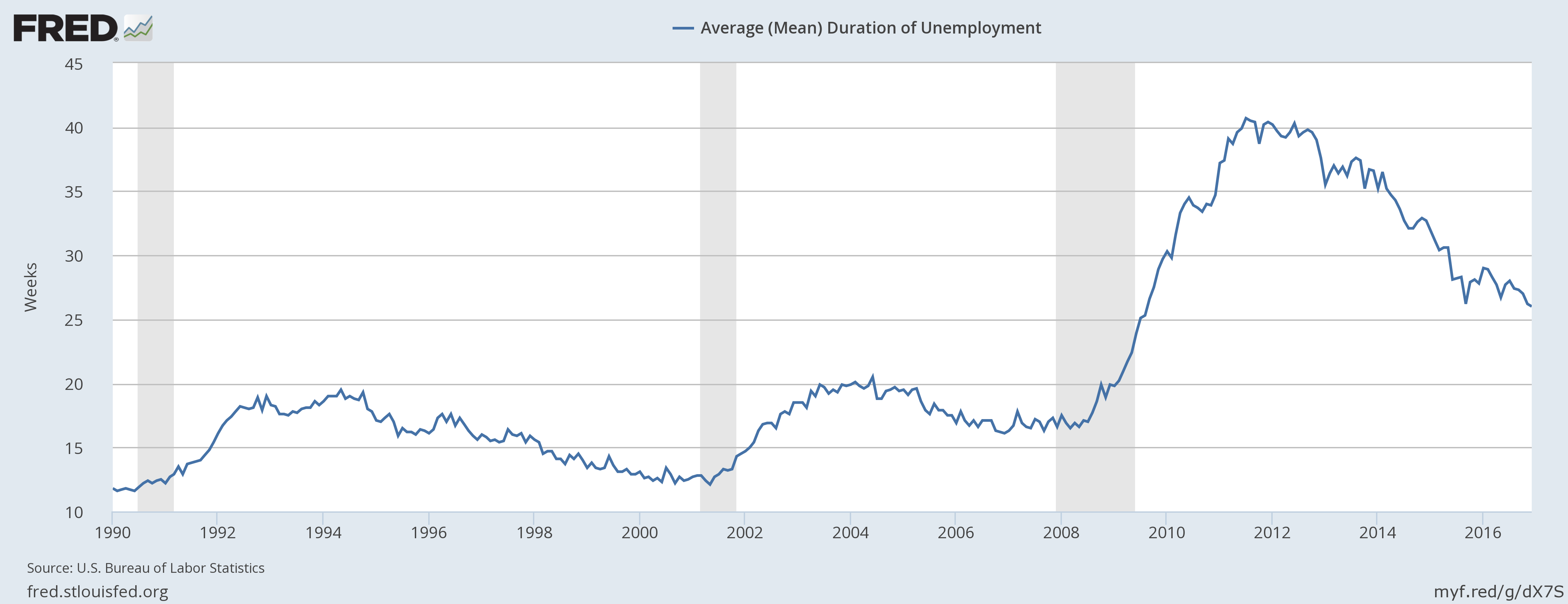

When the mean duration of unemployment was about 13 weeks—as it was throughout the 1990s—a 26-week UI allowance was generally sufficient. Since then, however, the average length of unemployment has increased, and has stayed persistently high since the Great Recession.

Mean duration of unemployment has more than doubled since 1990. Source: Data from Current Population Survey, U.S. Census and U.S. Bureau of Labor Statistics; retrieved via FRED, Federal Reserve Bank of St. Louis.

In 2015, the mean duration of unemployment was 28 weeks and, today, one in four jobless workers have been unemployed for longer than 26 weeks. Additionally, over the past 25 years, the proportion of workers covered by UI has fallen from 40% to just 27%. A major reason for the erosion of coverage is the rise of contract, temporary, freelance, contingent, and part-time work. One recent study estimated that 15.8% of all workers are now in such positions, and that nearly all new jobs created since 2000 fall into this category of “alternative work arrangement.”

HOW WAGE INSURANCE CAN HELP: LESSONS FROM PRIOR EFFORTS

Wage insurance could help workers cope with long-term reductions in earnings while incentivizing quick returns to work—creating benefits for workers, families, the economy, and government. Under a wage insurance program, when an unemployed worker starts a new job at lower pay, the insurance would kick in, bridging most of the gap between what they earned previously and their new wage. Without wage insurance, workers, many of whom do not expect and cannot afford to take pay cuts, pass on job opportunities that pay less. They remain unemployed longer—risking further damage to their future job prospects if they are jobless for extended periods. Wage insurance, in theory, should incentivize workers to take jobs sooner, even when they pay less. An important characteristic of wage insurance is that, once reemployed, the worker still has an incentive to hunt for higher paying jobs, because the benefit will always cover the gap between old and new earnings. Working more hours or accepting a promotion would not result in loss of benefits unless the worker’s new wages exceed what they earned before losing their job.

Currently, the United States operates one small wage insurance program, Alternative Trade Adjustment Assistance. ATAA is part of the Trade Adjustment Assistance Act (TAAA). TAAA’s narrow eligibility requirements limit the program to workers 50 and older, who have multi-year job tenure, and work in a TAAA-certified industry. Eligible workers must also choose between participating in ATAA and receiving any other TAAA benefits, including full-time job training and UI-like Trade Readjustment Allowances. They must make the choice before finding a new job and establishing a new income. Unsurprisingly, few people elect to take the risk of neither finding a new job nor receiving benefits that would otherwise be available. ATAA serves fewer than 4,000 workers per year, representing less than 6% of all TAAA workers who receive income supplements. It is worth noting that the wage insurance component of TAAA has not been evaluated since its launch in 2003.

ATAA is too restrictive but can serve as a framework for a more widely accessible program. When participants start a new job at lower wages (up to $50,000), the program subsidizes 50% of the difference, up to a maximum of $10,000 per year for two years. This is similar to the 2016 Obama administration proposal for a federal wage insurance program, which sought to expand the model to the broader labor market. The administration proposal, like ATAA, called for replacing half of lost wages, up to $10,000 per year for two years. The administration sought to control costs and limit eligibility to the highest-need workers through a three-year job tenure requirement.

CANADA'S EARNINGS SUPPLEMENT PROJECT

In the mid-1990s, the Canadian government, sharing the United States’ concern about growing job displacement due to trade, piloted and evaluated a wage insurance program. The Earnings Supplement Project (ESP) ran from 1995-1998 in Manitoba, Ontario, Quebec, and Saskatchewan. Its stated goal was to “provide direct compensation for wage reductions following job loss [and] provide temporary financial support that would promote—not impede—employment.”

To ensure that the pilot yielded meaningful data, it was implemented with a quasi-experimental design. When unemployed workers applied for benefits at one of the employment and workforce offices participating in the pilot, if they had a continuous work history prior to the recent job loss, they were randomly assigned either to a treatment group that could receive wage insurance or a control group that did not have access to the program. Treatment group participants were able to receive wage insurance if they accepted new jobs at lower wages within 26 weeks. The benefits bridged 75% of the gap between old wages and new, capped at $250 per week ($13,000 per year), for up to two years. Only 21% of treatment group participants met all requirements, accepted a lower-paying job within 26 weeks, and received supplements. On average, supplements were $195 per week, enabling recipients to replace 88% of their pre-unemployment income (compared to 50% for control group members). Fifteen months later, treatment group members had 5% less labor income than control group members, but greater total income (including unemployment and wage insurance benefits). Among the 21% of treatment group members who received payments, wage insurance had a large impact on their financial position. The average benefit amount was $5,663—nearly 20% of their total income. Administrative data indicate that 44% of recipients stayed in the program for the full two years, which required maintaining continuous employment at lower wages than they previously earned. These results and other program evaluation data indicate that ESP had a significant impact on workers’ willingness to accept lower-paying jobs, and impact on the length of unemployment. Wage insurance effectively cushioned the initial income shock and provided needed support as workers got back on their feet—achieving the government’s goal of reducing wage losses from unemployment while supporting rapid reemployment.

However, citing the fact that only 21% of treatment group members qualified for payments and concern about the cost of scaling up the program, the government declined to continue ESP.

Altogether, the U.S. and Canadian programs make clear that the success of a wage insurance program depends heavily on the goal. If policymakers are trying to reduce costs to the UI system, wage insurance is not a good solution. If the goal is decreasing the length of periods of unemployment, wage insurance is modestly effective. If, however, the goal is to prevent short-term negative income shocks due to job loss from causing and compounding long-term financial insecurity, wage insurance appears to fit the bill.

HOW INSTITUTIONS CAN HELP:

When EPIC surveyed a panel of experts about trends in income volatility, more than 70% expected income volatility to increase in the next decade. They identified social insurance policies as among the most likely to reduce income volatility.

Likewise, labor experts anticipate that employment security will continue to decline while “alternative work arrangements” will continue to grow. The convergence of these trends presents problems not just for workers and their families, but for the whole economy and society. In aggregate, the long-term reduction of incomes and increase in income volatility could be enormous.

While a full-fledged wage insurance program would require government backing, there is plenty of room—and great need—for innovation in the private sector. This section first explores those opportunities, then turns to the role of state and federal government.

FINANCIAL INSTITUTIONS AND INSURERS

Wage insurance products can and should be developed for the private market. There are many robust and competitive insurance markets other than those required by law (health, homeowners, and auto), such as renters insurance and life insurance. There are, however, significant barriers to overcome. The greatest legal barrier is the state-by-state nature of insurance regulation in the United States—products must be tailored to each state’s laws and approved by regulators in each state. The business challenge is also important: private insurers must invest significant resources to find and enroll large numbers of people who have great need for the product, a population that is often unaware that the insurance even exists. At the same time, most non-mandatory insurance products suffer from adverse selection, as the people most likely to pay for the product are those with the highest risk. To combat this, insurers must implement strategies to enroll large numbers of lower-risk customers. Despite those challenges, several financial institutions are already developing and scaling innovative insurance products. Pet insurance, for example, has in about a decade become a $775 million market. Similarly, several financial institutions have developed insurance products to cover other products they offer to consumers, like credit card insurance and identity theft insurance.

Financial institutions—including insurers and new entrants such as fintech firms—have an important role to play in helping develop wage insurance products that meet workers’ needs at low cost. One question in designing wage insurance programs is how high the benefit must be to be worth it for job seekers. Private firms are likely better positioned than government to answer this question, as they are already experts in tailoring coverage levels and costs for individual clients.

Wage insurance products can and should be developed for the private market. In fact, SafetyNet already offers an innovative wage insurance product that pays a lump sum in the event of job loss.

Premiums range from $5 to $30 per month on policies that pay lump sum payments of $1,500 to $9,000. This is relatively affordable coverage that could be accessible even to lower-income workers with higher risk of job loss. One of the most important features of SafetyNet—and one that is likely only possible in the private market—is its flexibility. While it is marketed as job loss insurance, it can also cover certain short-term disabilities and business closings. Sole proprietors are a major segment of the workforce that is not covered by UI, making this a potentially powerful product for millions of people. As a recent startup, SafetyNet is currently operating only in Wisconsin and Iowa, at least in part due to the high cost of adapting and gaining clearance to sell the product state by state.

EMPLOYERS

Throughout the EPIC cycle on income volatility, we have highlighted the many opportunities that employers have to help their workers, from implementing predictable scheduling, to partnering with the financial services industry to offer helpful products, to creating more full-time, permanent positions. Employers can also make a difference in helping their workers hedge against the risk of job loss.

In a labor market characterized by precarity and job insecurity, employers may think they have little incentive to help their workers insure against job loss. That said, many employers do offer severance pay, a benefit that is much like wage insurance in that it replaces lost earnings, but generally reserve it for higher-skill employees. It may not be feasible or affordable to offer severance packages to all employees, but employers can—and many do—partner with other firms to support their workers’ financial security through other methods. Most notably, employers have become an important conduit for innovative lenders, wage advance firms, and others to reach their target customers. The same could be possible when it comes to wage insurance. As others follow SafetyNet’s lead, employer partnerships could be an efficient strategy.

GOVERNMENTS

The most comprehensive, full-fledged wage insurance program would be public, like UI and Social Security.

California, Hawaii, New Jersey, New York, Rhode Island, and Puerto Rico have pioneered a new model for public social insurance—such as short-term disability and paid family leave—that could be adapted for wage insurance initiatives.

As such, governments have the greatest capacity to develop widely available wage insurance. Moreover, state governments have the opportunity to lead the way . President Obama recognized the important role of the states in his 2016 wage insurance proposal, which would have required states to create wage insurance programs. That model was similar to UI in that it proposed a federal-state partnership, giving states leeway to adjust many parameters of the program to fit their needs.

In fact, states already have a blueprint for developing new public insurance options. Five states (California, Hawaii, New Jersey, New York, Rhode Island) and Puerto Rico mandate that employers offer short-term disability benefits. Programs are funded with a combination of employer and employee contributions, depending on the state. California even has a supplemental program to insure employers and self-employed workers who are otherwise not covered by the mandate. Furthermore, three of those five states also mandate that employers offer paid family leave and provide those benefits through the existing short-term disability programs. In 2018, New York will join California, New Jersey, and Rhode Island in mandating and offering paid family leave policies. These first-movers have established a feasible model that can be adapted for wage insurance initiatives.

Given the many questions on how a public wage insurance program would work, perhaps the best role for the federal government at present is to support research and piloting efforts. This would not only equip the federal and state governments with more data, but the findings could also enable further innovation in the private market. One prominent researcher, in a recent assessment of the viability of wage insurance in the United States, identified key research questions that should be addressed before a large-scale wage insurance program is implemented. These questions could serve as the basis of a federal research agenda. He suggests developing pilot initiatives to test:

- Optimal qualification periods—do the findings from previous research still hold today?

- Optimal supplement amounts—how much is necessary to maximize take-up, and how small can a supplement be while remaining effective?

- Should wage supplements be paired with active labor market policies such as enhanced job search assistance and training?

- What are the long-term (5+ years) effects on recipients’ wages and total income?

- How much might a state-level or federal program cost? What are politically feasible and sustainable funding options?

In addition to exploring those questions, the federal government should conduct a long-overdue evaluation of ATAA, the existing wage insurance program. This would help policymakers understand whether it is effective, for which participants, and what would be required to boost take-up.

Finally, the federal government can take the models it has created for regulatory innovation initiatives, such as the Consumer Financial Protection Bureau’s Project Catalyst and the Office of the Comptroller of the Currency’s Office of Innovation, and expand to include insurance. The Department of the Treasury’s Federal Insurance Office, established under the Dodd-Frank Act, could be an appropriate home for such an initiative.

PRINCIPLES FOR FUTURE ACTION:

The goal of a public wage insurance program and private wage insurance products should be to prevent negative income shocks and incomplete recoveries from undermining workers’ long-term financial security. While implementing a public wage insurance program could generate savings in UI and new revenues through higher income taxes and more consumer spending, these should not be primary objectives. Research shows that policymakers should not expect more than breaking even on the administrative costs of a program. Providing supplements will require new money. In the private sector, of course, products must be profitable to be able to scale. Still, by focusing on their capacity to solve for the long-term consequences of job loss, private firms can make important contributions to our understanding of how to balance efficacy and efficiency in product design. Below, we identify principles to guide all actors in designing programs and products that are broadly accessible, have adequate duration of benefits and income replacement rates, are portable, and have some progressive features to target assistance at those with the greatest need and greatest risk.

Broad eligibility and accessibility: Workers who most need a wage insurance program or product include lower-income workers, those at high risk of becoming long-term unemployed, those with higher risk of long-term wage losses, and those who are not covered by UI. Job tenure requirements should be less than three years, since that excludes a large proportion of jobless workers. Private sector insurers and employers can work together to ensure not just broad eligibility but broad reach of private wage insurance products. In fact, the development of private products and dissemination through employers may be the best way to reach 1099 workers. Additionally, private products may be among the best solutions for the self-employed. They are excluded from UI because it is difficult to evaluate what counts as job loss and it is relatively easy for an unscrupulous few to game the system due to the role of cash and relaxed recordkeeping standards. SafetyNet’s standards for insuring the self-employed can be a model.

Adequacy: The supplements provided by a public program or private products must be sufficiently generous to both incentivize jobless workers to find and accept new work quickly, even at lower pay, and reduce the hardship associated with lost wages. ATAA has a 50% replacement rate and the Obama administration proposed a 50% replacement rate for its envisioned new program. On the other hand, Canada’s ESP had a 75% replacement rate. There is no precisely correct rate, but the 50%-75% interval seems like an appropriate choice. Greater experimentation is needed to further refine our understanding. In addition to the size of wage insurance supplements, it is important to consider the length of benefits. Given that it can take six years for a worker’s income to recover from a job loss, support needs to be available for significantly longer than UI benefits. Exactly how long is unknown—the two-year thresholds set in the U.S. and Canada seem to be arbitrary, seeking balance between long-term support and cost control. Here, too, governments and private firms should test a variety of options to better understand how long support is necessary to mitigate the long-term outcomes.

Portability: This is especially important for contingent and temporary workers and the self-employed. It is reasonable to set eligibility standards related to continuous work history, but it is important to recognize that in today’s economy, many hard workers will be continuously employed but by a variety of employers. At the public level, California’s short-term disability solution is a compelling model. They have a parallel program for the self-employed that is funded only with individual contributions, tying it only to the worker and enabling portability. Making this available through the public program spreads both cost and risk. At the same time, private wage insurance products likely have a critical role to play in developing and proving the model for portable benefits, and may find it a profitable niche. Several economists have already explored portable options. In fact, Jonathan Gruber, in a proposal to create “self-insured ‘security accounts,’” described those with more volatile incomes as primary beneficiaries. In a white paper for the Aspen Institute’s Future of Work Initiative, the Roosevelt Institute’s Susan Holmberg and Felicia Wong propose a similar idea, though their benefits would not be fully worker-funded.

Progressivity: Specifically, design programs to provide some additional support to those who already face financial insecurity, such as the working poor, and those who are most likely to experience profound, lasting wage losses, such as those served by the current trade adjustment assistance programs. Governments can create progressivity by lowering the cost of coverage via reduced tax contributions or by providing enhanced benefits for high needs groups. Private firms may not choose to directly create progressively structured products, but can still target additional assistance to those with the greatest need. Employer partnerships could be key here, as selling policies at scale can bring down costs and help mitigate adverse selection by making wage insurance easily accessible to a diverse range of workers with different risk profiles. Another advantage of employer partnerships is the possibility for employers to provide some subsidy to make wage insurance products affordable for their lower-wage workers.

Development of wage insurance policies and products is still nascent. Right now, the most important role for all actors is to support research and experimentation and share what they learn. Wage insurance is well-suited to the specific challenges faced by households that experience negative income shocks, but there are many questions about what works and how to best use scarce resources. Further research will lay the groundwork for fully fledged public programs and competitive private marketplaces, both of which have critical roles to play in helping workers overcome the insecurity and challenges they face in today’s labor markets.

For Endnotes and Works Cited, please download the PDF version of this Issue Brief:

● Acknowledgments

EPIC would like to thank Katherine Lucas McKay for writing this brief; Kiese Hansen, Gracie Lynne, David Mitchell, Ida Rademacher, and Joanna Smith-Ramani for reviewing drafts and making invaluable suggestions; Liz Ben-Ishai, Mark Greene, Adele Hunter, Tim Lucas, and Rachel West for the time and wisdom they shared on a topics ranging from labor markets conditions, unemployment and jobless workers, social insurance, and private market products; thanks also to Laura Starita at Sona Partners for designing the template. EPIC would also like to thank all those who completed the expert surveys or participated in either of the EPIC convenings. While this document draws on insights shared at these EPIC forums and by the aforementioned individuals, the findings, interpretations, and conclusions expressed in this report – as well as any errors – are EPIC’s alone and do not necessarily represent the view of EPIC’s funders or Advisory Group members. Finally, EPIC thanks the Ford Foundation and the W.K. Kellogg Foundation for their generous support.

●●●●

●●●●

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037© The Aspen Institute 2017—All Rights Reserved