What's Trending | Solutions Framework | November 14, 2018

Lifting the Weight: Solving the Consumer Debt Crisis

●●●●

● Executive Summary

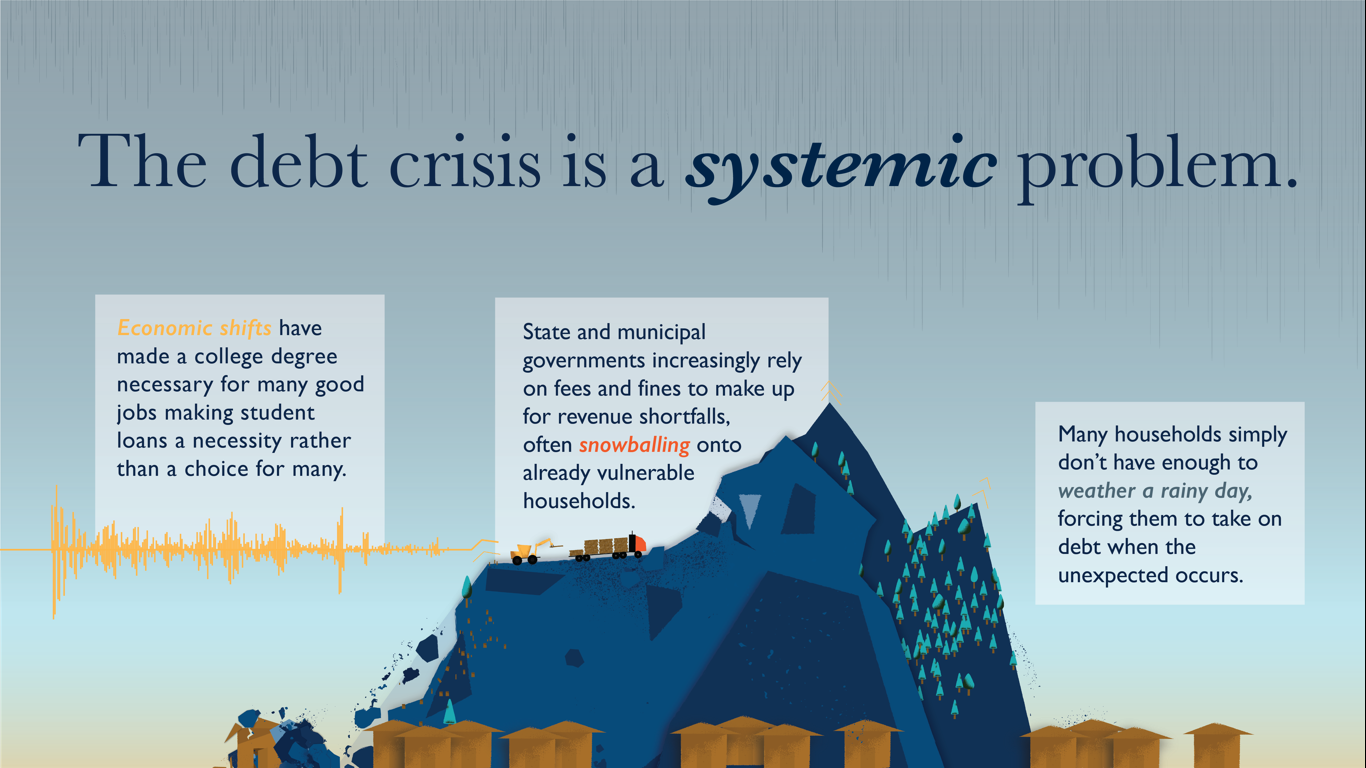

Consumer debt is ubiquitous. Although at any given time some Americans are debt-free, most of us carry debt some or even all of the time. We borrow for various reasons, and we are increasingly likely to incur debt also from non-loan sources (such as an out-of-pocket medical expense or being assessed a governmental fine or fee. Consumer debt is not inherently bad (taking on debt can often be a sound financial decision), but it is a concern today because it has reached record levels, and its effects reach deeply into financial security, physical and mental health, as well as the broader economy. Consumer debt is a systemic problem with significant consequences, but there are systemic solutions. With solutions ranging from product-level improvements to broader reforms, EPIC has identified options for stakeholders in every sector and for partnerships across sectors. Collectively, these solutions possess tremendous potential to address a critical dimension of household financial insecurity.

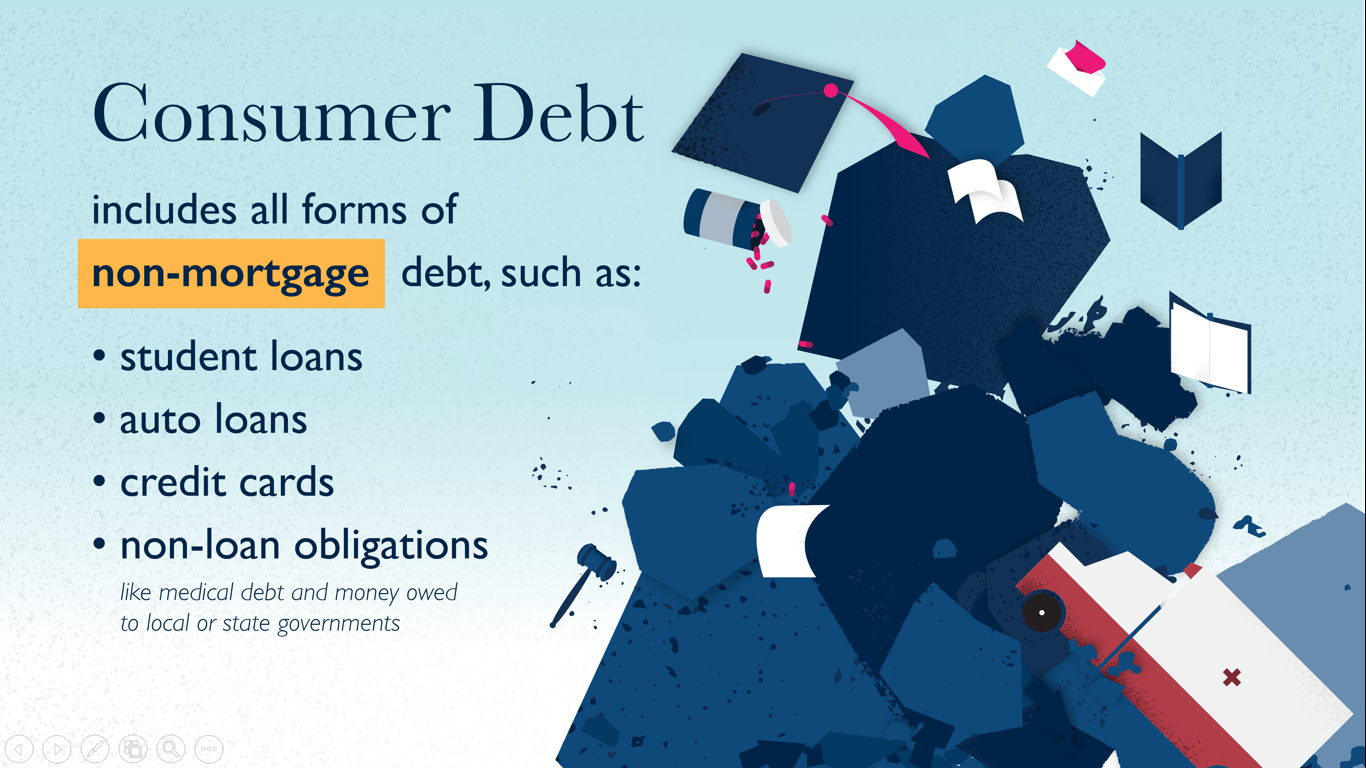

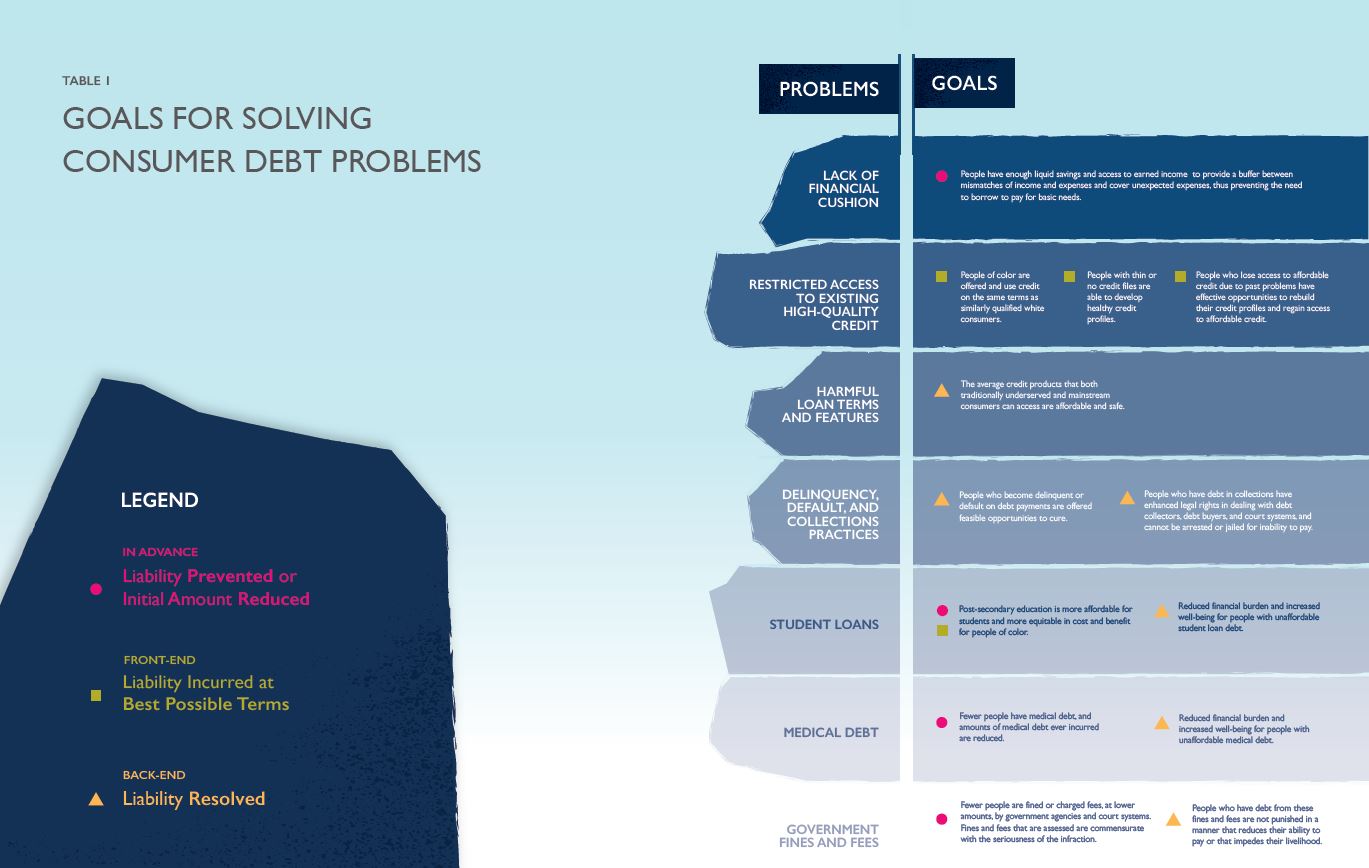

EPIC’s research has identified seven specific consumer debt problems – all amenable to solutions – that result in financial insecurity and damage well-being. Four of the identified problems are general to consumer debt: households’ lack of savings or financial cushion, restricted access to existing high-quality credit for specific groups of consumers, exposure to harmful loan terms and features, and detrimental delinquency, default, and collections practices. The other three problems relate to structural features of three specific types of debt: student loans, medical debt, and government fines and fees.

● SHARE

- New Solutions Framework from #AspenEPIC identifies the significant consequences of consumer debt, especially for low- and moderate-income households and other financially vulnerable Americans. https://buff.ly/2RWqHVP

- Consumer debt is a systemic problem with systemic solutions. New Solutions Framework from #AspenEPIC has identified solutions for stakeholders in every sector & for cross-sector partnerships. https://buff.ly/2RWqHVP

- #AspenEPIC’s research identified seven specific consumer debt problems that result in financial insecurity and damage well-being, and all are amendable to solutions. Read the full solutions framework: https://buff.ly/2RWqHVP

- Even a typical middle-income household has ready access to less than two-thirds of the liquid savings it needs to stabilize usual monthly fluctuations in income and spending. Read the full framework from #AspenEPIC https://buff.ly/2RWqHVP

- Fewer than half of all households have sufficient savings to cover an average-sized dip in income, and the typical low-income household has fewer liquid assets than it would take to cover the loss of just two weeks of pay. #AspenEPIC https://buff.ly/2RWqHVP

- Access to high-quality credit is a prerequisite for debt to be a positive force in a household’s financial life, yet access to affordable credit is racially inequitable and unnecessarily unavailable to many with limited credit histories or past problems. #AspenEPIC https://buff.ly/2RWqHVP

- Borrowers of different races with substantially similar income, assets, credit scores, and other financial characteristics are denied loans at different rates and, when approved, are charged different amounts of interest and fees. New Framework from #AspenEPIC identifies the dangers of consumer debt. https://buff.ly/2RWqHVP

- Exposure to harmful loan terms and features is a major risk factor for debt becoming a source of financial insecurity. Read the full Consumer Debt Solutions Framework from #AspenEPIC: https://buff.ly/2RWqHVP

- Only 14% of payday borrowers can afford to repay the average loan, and 41% report needing a cash infusion to pay off the advance. These loans are explicitly structured to encourage borrowers to roll over into new debt. #AspenEPIC https://buff.ly/2RWqHVP

- "About 5% of outstanding debt is 90 days or more delinquent, and an estimated 71 million adults in the US have debt in collections." Learn more from the new Consumer Debt Solutions Framework from #AspenEPIC: https://buff.ly/2RWqHVP

- Companies now routinely use courts to pursue consumers over small debts & about 1 in 7 of those contacted by debt collectors are sued. #AspenEPIC https://buff.ly/2RWqHVP

- The overwhelming majority of debt collection lawsuits result in default judgments even though consumers may have legitimate defenses. Now is the time to solve the consumer debt crisis: https://buff.ly/2RWqHVP #AspenEPIC

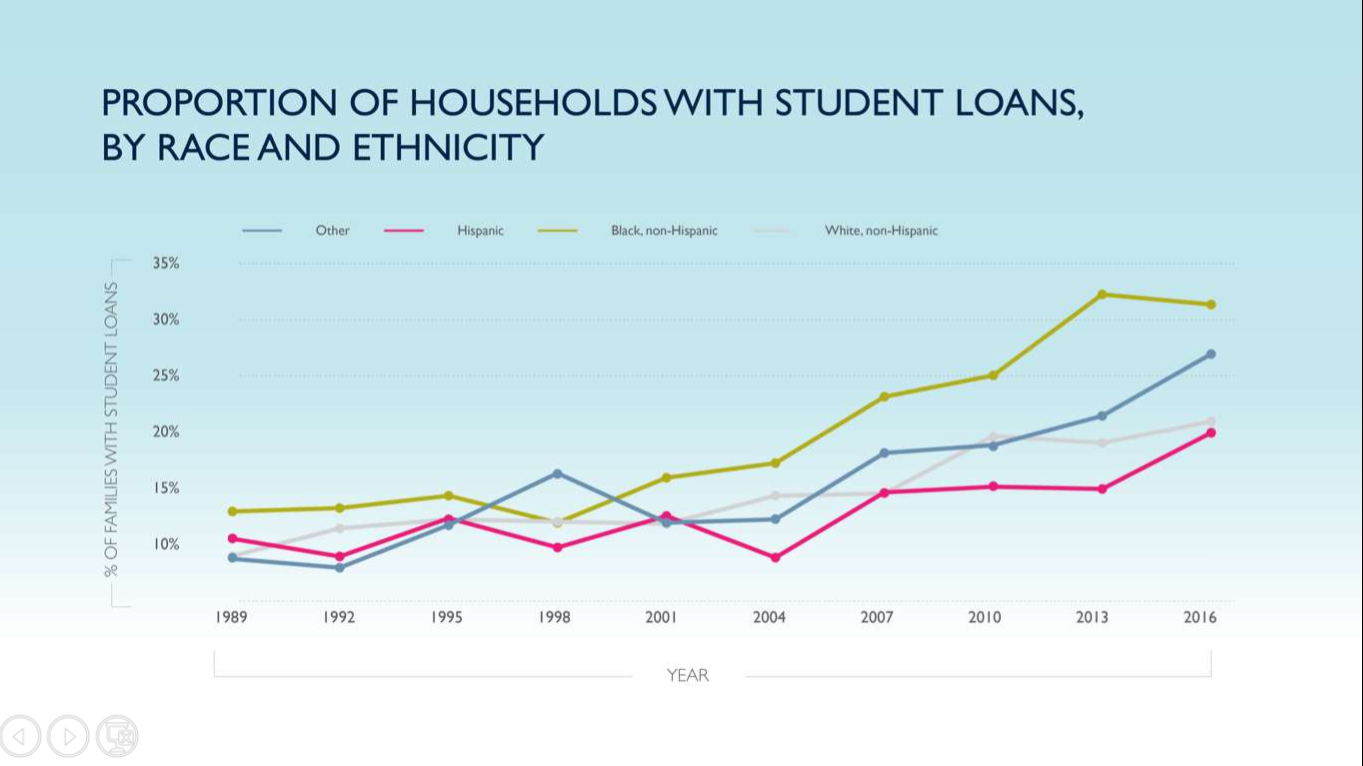

- The burden from record-level student loan debt reduces the ability of households to save and build wealth, and it has increased rather than narrowed the racial wealth gap. Learn more from #AspenEPIC's solutions framework: https://buff.ly/2Tes3wH

- #AspenEPIC's Consumer Debt Solutions Framework finds that since students of color disproportionately attend for-profit institutions, borrow more, and have lower graduation rates, they are at the greatest risk of financial hardship and experience disproportionate harm. https://buff.ly/2Tes3wH

- People often do not choose to incur debt for health care, being constrained both by medical necessity and a lack of pricing knowledge; moreover, there are racial disparities in the incidence of medical debt. #AspenEPIC https://buff.ly/2RWqHVP

- How can we reduce the burdens and increase financial well-being for people with unaffordable medical debt? Read #AspenEPIC's solutions framework today: https://buff.ly/2RWqHVP

- Unlike the other types of debt discussed in #AspenEPIC's framework, the harms of debt from government-issued fines and fees are created entirely through government policy. https://buff.ly/2RWqHVP

- Cities with large African-American populations are associated with levying large amounts of fines and fees. Now is the time to solve the consumer debt crisis: https://buff.ly/2RWqHVP #AspenEPIC

●●●●

●●●●

Your input and participation helps ensure that we have a level of dialogue and knowledge synthesis that is thorough and goes beyond usual sound bites.

We’re always looking to expand our network. Join our mailing list to stay in the loop with everything we’re working on.

EPIC is an initiative of the Aspen Institute's Financial Security Program.

CONTACT US:

The Aspen Institute

2300 N Street, NW Suite 700, Washington, DC 20037

Financial Security Program | The Aspen Institute | 2300 N Street, NW Suite 700 Washington, DC 20037 [cn-social-icon]

© The Aspen Institute 2017—All Rights Reserved